Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:PLUS

Should ePlus' (PLUS) Upbeat Earnings and Dividend Hike Prompt Reassessment by Investors?

Simply Wall St

Reviewed by Sasha Jovanovic

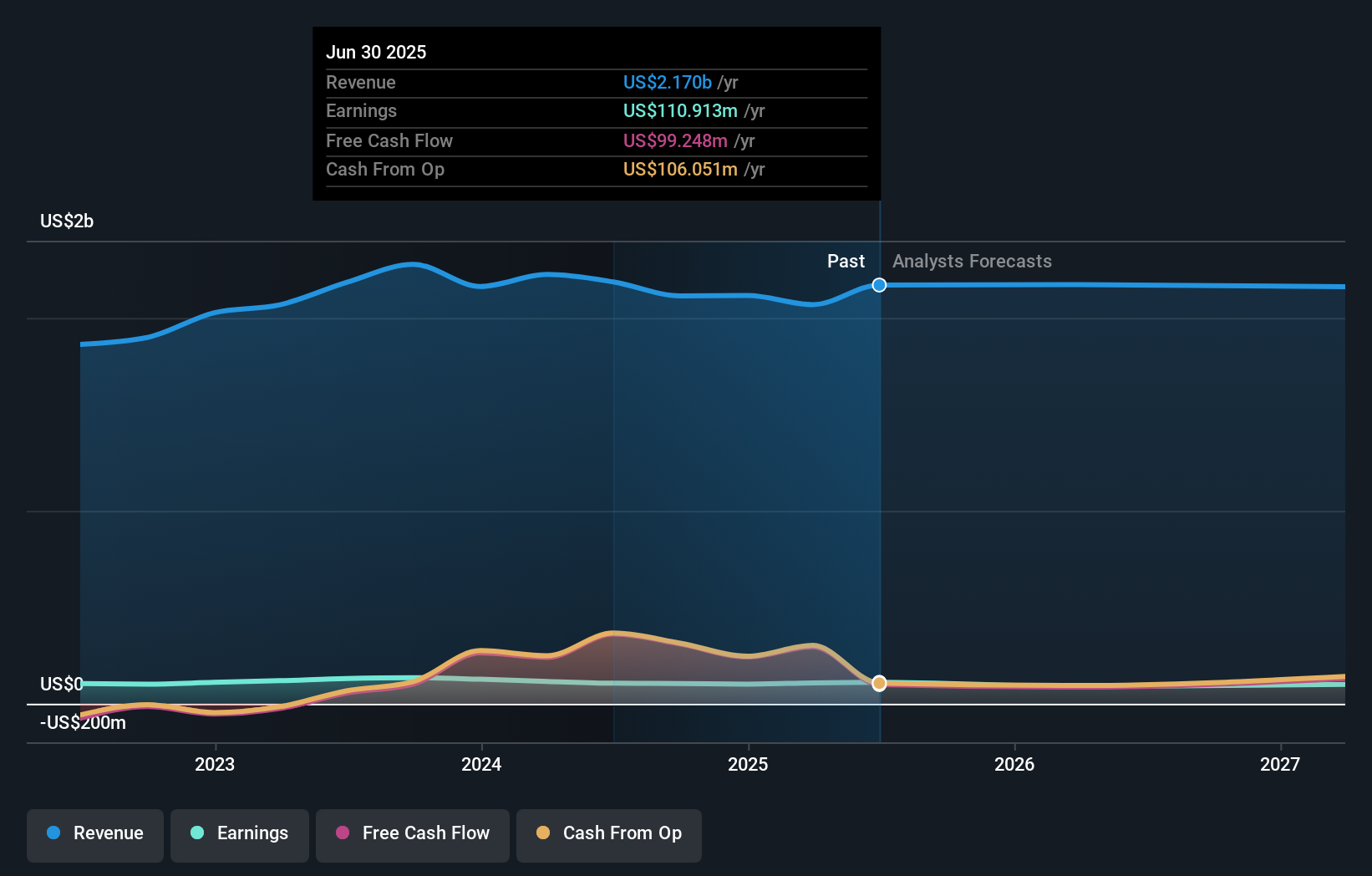

- On November 6, 2025, ePlus announced strong second quarter earnings results, raised its fiscal year 2026 earnings guidance, and declared a quarterly dividend of US$0.25 per share payable on December 17, 2025, to shareholders of record as of November 25.

- The improved outlook reflects management’s ongoing confidence following double-digit year-over-year growth in revenue, gross profit, and net earnings for the second quarter.

- We'll explore how ePlus's raised full-year guidance, after robust Q2 results, could shift the company's previously cautious investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

ePlus Investment Narrative Recap

To be a shareholder in ePlus, you have to believe in the company’s ability to drive consistent revenue and profit growth from accelerating demand for IT infrastructure, security, and digital transformation. The latest quarterly earnings beat, dividend announcement, and improved fiscal year guidance bring momentum to this outlook but do not eliminate the short-term risk of revenue volatility tied to large, project-based customer deals, this risk remains a key factor to monitor.

Among the recent announcements, ePlus’s raised full-year guidance stands out as particularly relevant. By projecting mid-teens growth in both net sales and gross profit, along with increased adjusted EBITDA, the company is signaling a strong expectation of continued operating leverage and profitability, reinforcing the positive catalyst of expanding demand for managed and recurring services.

Yet in contrast, investors should also be aware that customer concentration in key verticals still leaves ePlus exposed if spending patterns unexpectedly shift...

Read the full narrative on ePlus (it's free!)

ePlus' narrative projects $2.2 billion revenue and $78.4 million earnings by 2028. This requires a -0.2% yearly revenue decline and a $32.5 million decrease in earnings from $110.9 million today.

Uncover how ePlus' forecasts yield a $92.00 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Community estimates for ePlus’s fair value range widely, from US$34.92 to US$92, with just 2 individual perspectives submitted to Simply Wall St Community. Despite positive momentum from improved guidance, recurring revenue expansion will remain crucial as opinion on the company’s future varies greatly.

Explore 2 other fair value estimates on ePlus - why the stock might be worth as much as 25% more than the current price!

Build Your Own ePlus Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ePlus research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ePlus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ePlus' overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PLUS

ePlus

Provides information technology (IT) solutions that enable organizations to optimize IT environment and supply chain processes in the United States and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

TA

Talos on Tesla ·

The "Physical AI" Monopoly – A New Industrial Revolution

Fair Value:US$665.3637.3% undervalued

30 followersusers have followed this narrative

14 commentsusers have commented on this narrative

17 likesusers have liked this narrative

MA

Marek_Trnka on CSG ·

Czechoslovak Group - is it really so hot?

Fair Value:€5548.6% undervalued

36 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

AL

alex30free on Swedencare ·

The Compound Effect: From Acquisition to Integration

Fair Value:SEK 46.2846.8% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Rio Silver ·

Rare Pure High Grade Silver with 35% Insider (Near Producer)

Fair Value:CA$2297.1% undervalued

1 followerusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AL

alex30free on Vitec Software Group ·

Swedens Constellation Software

Fair Value:SEK 316.8923.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on Inotiv ·

Inotiv NAMs Test Center

Fair Value:US$1.276.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.886.3% undervalued

57 followersusers have followed this narrative

5 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3319.7% undervalued

79 followersusers have followed this narrative

0 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.8% undervalued

1068 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative

Trending Discussion

US

User on Tesla ·

When was the last time that Tesla delivered on its promises? Lets go through the list! The last successful would be the Tesla Model 3 which was 2019 with first deliveries 2017. Roadster not shipped. Tesla Cybertruck global roll out failed. They might have a bunch of prototypes (that are being controlled remotely) And you think they'll be able to ship something as complicated as a robot? It's a pure speculation buy.

3

|1

US

User on Tesla ·

This article completely disregards (ignores, forgets) how far China is in this field. If Tesla continues on this path, they will be fighting for their lives trying to sell $40000 dollar robots that can do less than a $10000 dollar one from China will do. Fair value of Tesla? It has always been a hype stock with a valuation completely unbased in reality. Your guess is as good as mine, but especially after the carbon credit scheme got canned, it is downwards of $150.

2

|0

TI

TickerTickle on Figma ·

Figma is still deeply embedded as the default design system in big companies, and the ecosystem (Buzz, Slides, Sites, Make) is clearly the strategic play rather than a one‑off product bet. None of those qualitative assumptions have really broken yet, the bigger change has been sentiment toward growth/AI software in general, not Figma’s product reality. Assuming ~30% annual growth, margins stepping up to 25%, and a 40x PE in 2030 with an 8.4% discount rate is too optimistic now considering how the broader market is now pricing similar SaaS names, which means you can believe in the long term thesis and still accept that the stock might chop sideways or even drift lower while expectations and multiples reset. I will be sharing an update soon.

1

|0