Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:NTAP

These 4 Measures Indicate That NetApp (NASDAQ:NTAP) Is Using Debt Safely

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, NetApp, Inc. (NASDAQ:NTAP) does carry debt. But is this debt a concern to shareholders?

We check all companies for important risks. See what we found for NetApp in our free report.When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is NetApp's Debt?

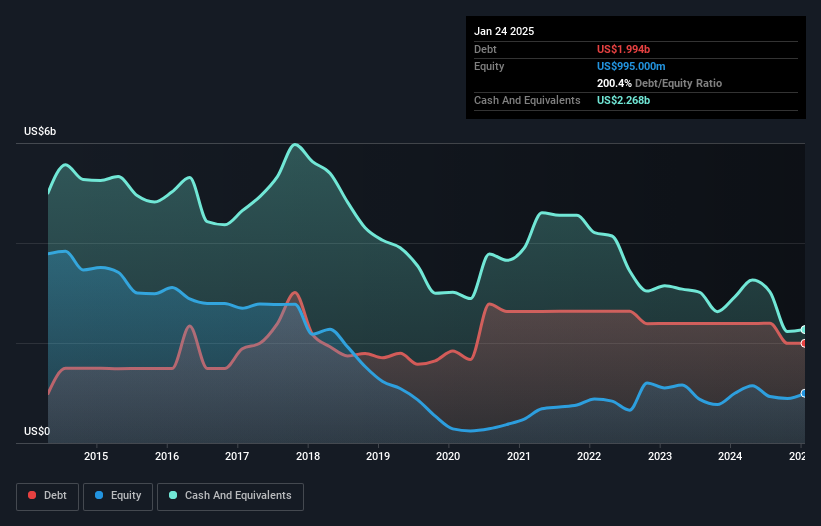

The image below, which you can click on for greater detail, shows that NetApp had debt of US$1.99b at the end of January 2025, a reduction from US$2.39b over a year. However, it does have US$2.27b in cash offsetting this, leading to net cash of US$274.0m.

How Healthy Is NetApp's Balance Sheet?

We can see from the most recent balance sheet that NetApp had liabilities of US$4.20b falling due within a year, and liabilities of US$3.80b due beyond that. On the other hand, it had cash of US$2.27b and US$898.0m worth of receivables due within a year. So it has liabilities totalling US$4.83b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since NetApp has a huge market capitalization of US$16.8b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt. Despite its noteworthy liabilities, NetApp boasts net cash, so it's fair to say it does not have a heavy debt load!

Check out our latest analysis for NetApp

Also good is that NetApp grew its EBIT at 14% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine NetApp's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. NetApp may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, NetApp generated free cash flow amounting to a very robust 91% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Summing Up

Although NetApp's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$274.0m. And it impressed us with free cash flow of US$1.3b, being 91% of its EBIT. So we don't think NetApp's use of debt is risky. Another factor that would give us confidence in NetApp would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if NetApp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:NTAP

NetApp

Provides a range of enterprise software, systems, and services that customers use to transform their data infrastructures in the United States, Canada, Latin America, Europe, the Middle East, Africa, and the Asia Pacific.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

289 followersusers have followed this narrative

1 commentusers have commented on this narrative

43 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

102 followersusers have followed this narrative

2 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

9 followersusers have followed this narrative

3 commentsusers have commented on this narrative

4 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2803.2% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

KA

kapirey on OceanaGold ·

OceanaGold: Potential Upside with High Costs and Mid-Tier Status

Fair Value:CA$65.3336.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18057.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HE

HedgeY on Newron Pharmaceuticals ·

Still A Binary Phase III Bet on Evenamide

Fair Value:CHF 1824.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

102 followersusers have followed this narrative

2 commentsusers have commented on this narrative

29 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.229.5% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.1% undervalued

1399 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative