Advertisement

- United States

- /

- IT

- /

- NYSE:NET

Cloudflare (NET) Valuation Checked After Record 2025 Quarter Beat And Strong 2026 Growth Guidance

Cloudflare (NET) just followed its strongest quarter of 2025 with fresh numbers and 2026 guidance, giving investors new reference points on growth, profitability progress, and how AI driven demand might shape the business.

See our latest analysis for Cloudflare.

The recent earnings beat and upbeat 2026 revenue guidance have helped lift sentiment, with a 5.77% 1 day share price return and 12.72% 7 day share price return. The 3 year total shareholder return above 200% indicates that longer term momentum has been strong overall.

If Cloudflare’s AI story has caught your attention, this could be a good moment to look across the sector and see what else stands out in our list of 34 AI infrastructure stocks.

With Cloudflare shares up strongly over the past week and trading below the average analyst price target, the key question now is whether recent AI optimism leaves further upside or if the market is already pricing in years of growth.

Most Popular Narrative: 15.9% Undervalued

With Cloudflare last closing at $195.85 and the most followed narrative pointing to a fair value of about $232.78, the story behind that gap focuses heavily on growth, margins and AI driven opportunities.

Cloudflare's early action building strategic positioning around the emerging Agentic Web and "Act 4" initiatives, leveraging its unique reach across 20% of the Internet and broad AI partnerships, offers significant optionality for new high-margin transaction-based business models that could unlock new revenue streams and expand the addressable market.

Curious how that potential relates to a higher fair value estimate? The narrative considers revenue trends, profitability dynamics and an earnings multiple that reflects expectations around Cloudflare’s ability to scale within AI and security themes.

Result: Fair Value of $232.78 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still real watchpoints here, including pressure on gross margins and intense competition from hyperscalers that could challenge the AI- and security-led upside story.

Find out about the key risks to this Cloudflare narrative.

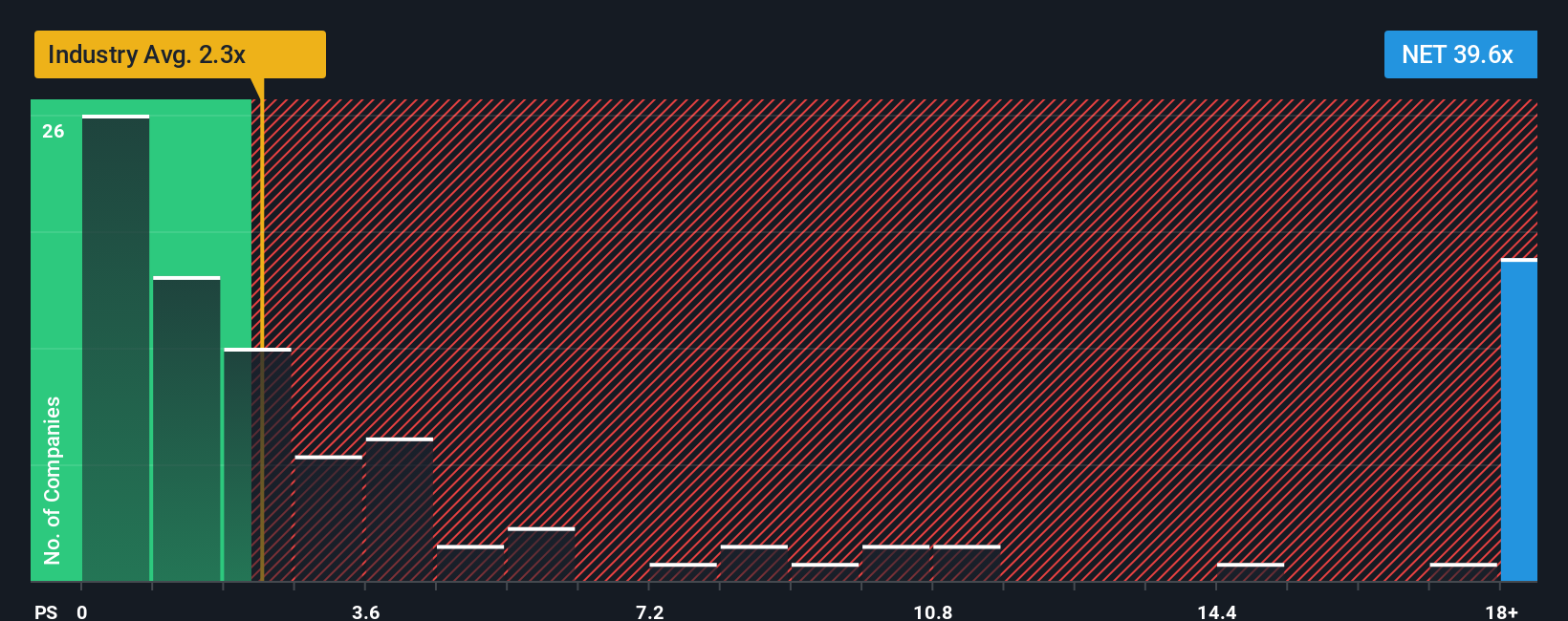

Another View: Multiples Paint A Very Different Picture

That 15.9% “undervalued” narrative leans heavily on future growth and margins, but the current P/S of 31.8x tells a very different story. It is far above the US IT industry at 2.2x, peers at 12.9x, and even the Simply Wall St fair ratio of 13.5x. This raises the question: is the real risk that expectations are already stretched?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Cloudflare Narrative

If you look at the numbers and come to a different conclusion, or just prefer to test your own assumptions, you can build a custom Cloudflare story from scratch in a few minutes: Do it your way.

A great starting point for your Cloudflare research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Cloudflare might be front of mind right now, but the real edge often comes from having a curated watchlist of other strong candidates ready to go.

- Spot potential mispricings early by checking out our list of 54 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect them.

- Strengthen your income stream by reviewing 13 dividend fortresses that offer higher yields with an emphasis on stability and consistency.

- Protect your downside by scanning 83 resilient stocks with low risk scores built around companies with more resilient financial and business risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NET

Cloudflare

Operates as a cloud services provider that delivers a range of services to businesses worldwide.

Exceptional growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.559.3% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$4811.0% overvalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

18 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8212.9% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on NIKE ·

Nike - A Fundamental and Historical Valuation

Fair Value:US$36.8311.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on AnaptysBio ·

ANAB has a scaling and rising royalty stream, one up and coming new royalty, a loan that dies in 2027 which will result in a doubling

Fair Value:US$9025.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GE

Germaine on MM Computer Systems Berhad ·

MM Computer Systems' Latest Contract Wins Reinforce Growth Momentum After Listing

Fair Value:RM 0.3313.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75031.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.9% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.2% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative