Advertisement

- United States

- /

- IT

- /

- NasdaqGS:VRSN

Is VeriSign’s (VRSN) Domain Growth Enough to Sustain Its Competitive Edge?

Simply Wall St

Reviewed by Sasha Jovanovic

- VeriSign reported strong third-quarter results, with revenue reaching US$419.1 million and net income at US$212.8 million, both ahead of the prior year’s figures.

- The company’s ongoing marketing efforts and enhanced registrar engagement contributed to higher new domain registrations and improved renewal rates, driving earnings growth beyond expectations.

- We will explore how this earnings outperformance, led by growth in domain registrations, impacts VeriSign’s broader investment narrative.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

VeriSign Investment Narrative Recap

For investors considering VeriSign, the core belief centers on the resilience of its domain registry business and the potential for steady revenue from new registrations and renewals. The latest quarterly results, which topped expectations on both sales and earnings, signal positive momentum but do not fundamentally alter the main catalyst: sustainable growth in domain name registrations. However, the main risk, slowing industry-wide demand for new domains, remains unaddressed by this news and deserves continued monitoring.

Of all the recent announcements, the company’s ongoing quarterly dividend of US$0.77 per share stands out. This regular payout underscores management’s focus on delivering stable returns to shareholders and aligns with the earnings outperformance that has fueled positive sentiment around the stock’s short-term prospects. But while these cash distributions speak to stability, investors should stay attentive to ...

Read the full narrative on VeriSign (it's free!)

VeriSign's narrative projects $1.9 billion in revenue and $1.0 billion in earnings by 2028. This requires 6.4% yearly revenue growth and an earnings increase of about $200 million from current earnings of $799.5 million.

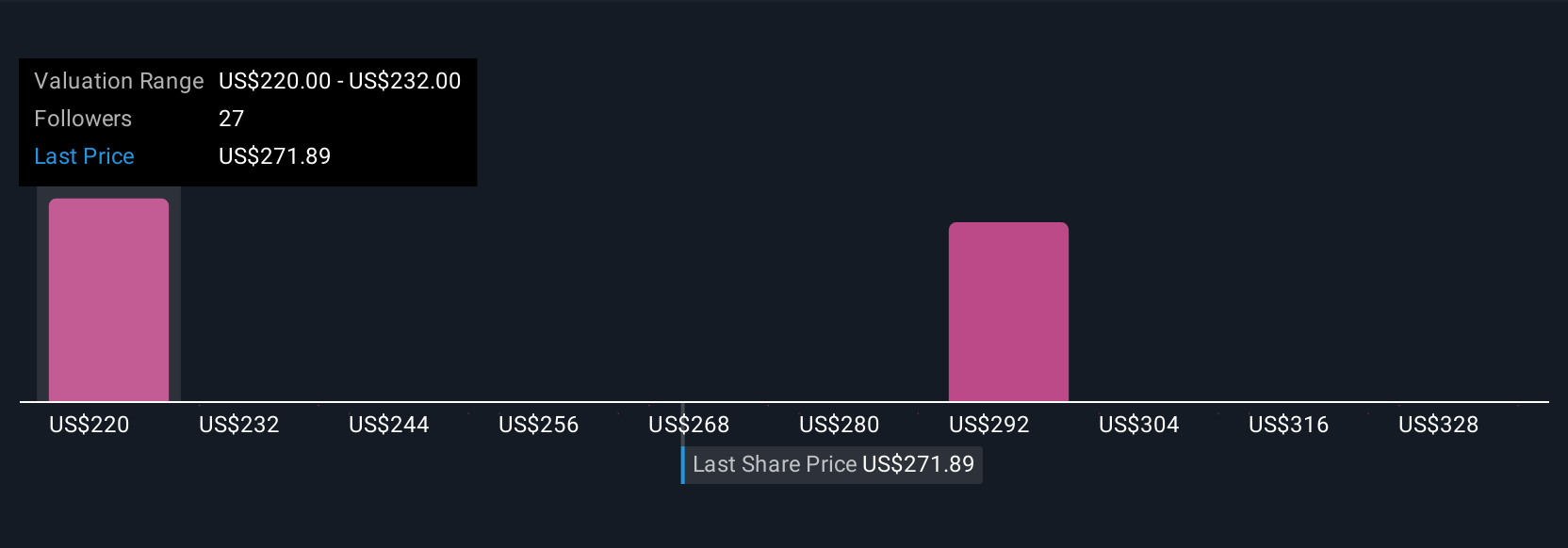

Uncover how VeriSign's forecasts yield a $304.00 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Seven Simply Wall St Community fair value estimates for VeriSign span from US$211.66 to US$340 per share. While analysts remain focused on the trend in domain registration growth, you should keep in mind that investor opinions are often wide ranging and worth comparing.

Explore 7 other fair value estimates on VeriSign - why the stock might be worth as much as 44% more than the current price!

Build Your Own VeriSign Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your VeriSign research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free VeriSign research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate VeriSign's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've found 24 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Rare earth metals are the new gold rush. Find out which 35 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRSN

VeriSign

Provides internet infrastructure and domain name registry services that enables internet navigation for various recognized domain names worldwide.

Good value with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor