Advertisement

- United States

- /

- Software

- /

- NasdaqGS:VRNS

A Look At Varonis Systems (VRNS) Valuation After Analyst Upgrades And AllTrue.ai Acquisition

Varonis Systems (VRNS) is back in focus after a cluster of analyst upgrades, the announced purchase of AllTrue.ai for US$125 million, and fresh earnings that topped market expectations despite ongoing securities class action lawsuits.

See our latest analysis for Varonis Systems.

Despite the recent analyst upgrades and the AllTrue.ai deal, Varonis' 30 day share price return of 24.34% and year to date share price return decline of 20.85%, alongside a 1 year total shareholder return decline of 42.49%, point to momentum that is still rebuilding after last year's sharp reset and ongoing class action headlines.

If this mix of AI driven security news and legal risk has your attention, it could be a good moment to see what else is out there with our screener of 58 profitable AI stocks that aren't just burning cash and compare how other names in the space are holding up.

With Varonis trading at a discount of roughly 35% to the average analyst price target and an estimated intrinsic value gap of about 47%, you have to ask: is this a reset opportunity, or is growth already fully priced in?

Most Popular Narrative: 25.8% Undervalued

Varonis last closed at $25.36, compared with a widely followed fair value narrative of $34.20, which rests heavily on its long term AI driven data security role.

Continued SaaS transition and high NRR (notably for SaaS customers), combined with robust upsell momentum across cloud and multi-cloud environments, enhance ARR visibility and predictability, driving durable earnings and margin expansion as the SaaS mix climbs and operational leverage improves post-transition.

Want to see what is really backing that fair value gap? The narrative refers to compound revenue growth, rising margins, and a future profit multiple that assumes meaningful execution. Curious which numbers anchor that view and how they fit together over the next few years?

Result: Fair Value of $34.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that gap could close quickly if the SaaS transition continues to pressure margins or if competition in data security forces heavier investment and weaker pricing power.

Find out about the key risks to this Varonis Systems narrative.

Another View: Multiples Paint A Tighter Picture

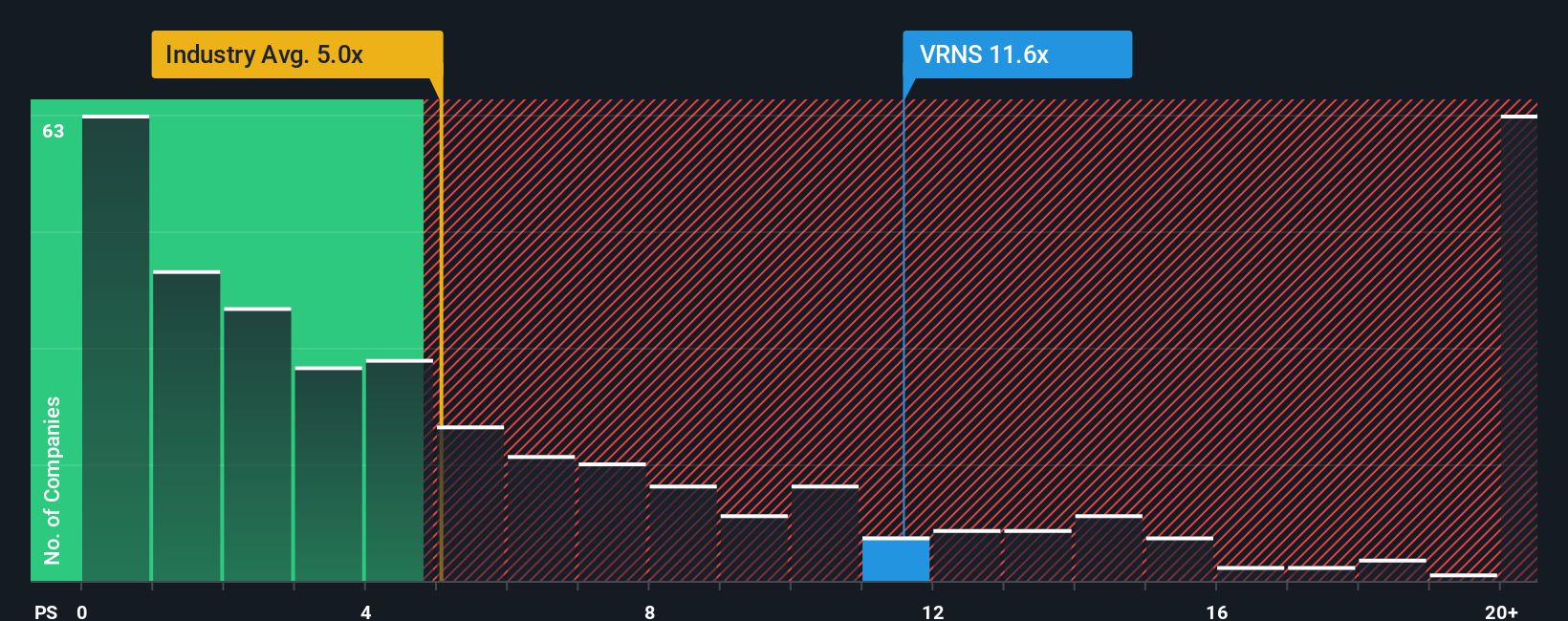

While the narrative and fair value work suggest Varonis is 46.9% below an estimated intrinsic value of $47.80, its current P/S ratio of 4.8x looks richer than both peers at 3.4x and the US Software average at 3.6x, and only slightly below a fair ratio of 5.1x. That mix hints at less obvious upside and more balance between potential opportunity and valuation risk. Which signal do you trust more?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Varonis Systems Narrative

If you think this story misses something or you simply prefer to work from the raw numbers yourself, you can build a custom thesis in minutes: Do it your way

A great starting point for your Varonis Systems research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Varonis has sharpened your thinking, do not stop there. Use the Simply Wall St Screener to uncover other opportunities that could fit your goals better.

- Target stability first by checking companies in our 83 resilient stocks with low risk scores that score well on risk while still offering room for growth.

- Hunt for potential bargains by reviewing the screener containing 24 high quality undiscovered gems, where strong fundamentals meet limited current attention.

- Prioritize resilience by focusing on companies in the solid balance sheet and fundamentals stocks screener (44 results) that pair financial strength with consistent business profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRNS

Varonis Systems

Provides software products and services that continuously discover and classify critical data, remediate exposures, and detect advanced threats with AI-powered technology in North America, Europe, APAC, and rest of worlds.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4351.3% undervalued

77 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8166.9% undervalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

VA

ValueInvestingSubstack on IJM Corporation Berhad ·

What's the Fair Value of IJM?

Fair Value:RM 1.7716.9% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VA

ValueInvestingSubstack on Intel ·

Is Intel Still Investable At $60?

Fair Value:US$1307.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VA

ValueInvestingSubstack on PayPal Holdings ·

$PYPL Options Are Cheap

Fair Value:US$6026.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.4% undervalued

113 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6119.8% undervalued

1194 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative