Advertisement

- United States

- /

- IT

- /

- NasdaqGS:VNET

Is VNET Group (NASDAQ:VNET) Using Debt In A Risky Way?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that VNET Group, Inc. (NASDAQ:VNET) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for VNET Group

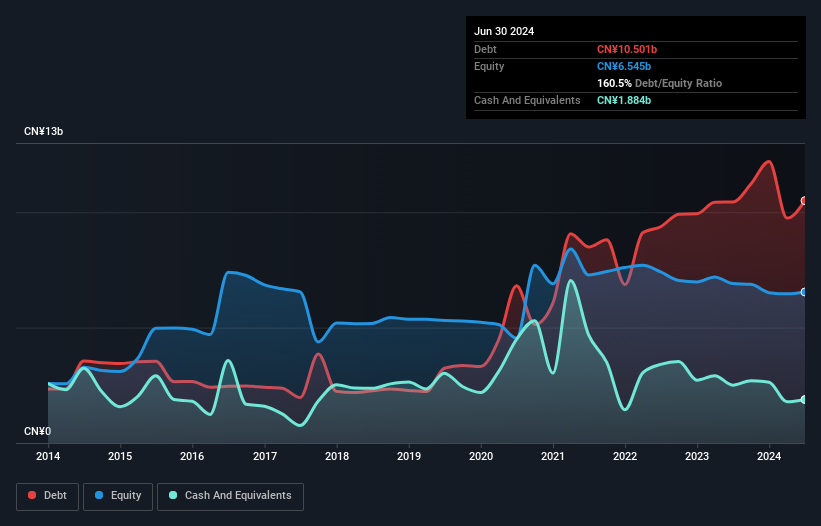

How Much Debt Does VNET Group Carry?

As you can see below, VNET Group had CN¥10.5b of debt, at June 2024, which is about the same as the year before. You can click the chart for greater detail. However, it also had CN¥1.88b in cash, and so its net debt is CN¥8.62b.

A Look At VNET Group's Liabilities

Zooming in on the latest balance sheet data, we can see that VNET Group had liabilities of CN¥8.14b due within 12 months and liabilities of CN¥14.4b due beyond that. Offsetting these obligations, it had cash of CN¥1.88b as well as receivables valued at CN¥2.15b due within 12 months. So it has liabilities totalling CN¥18.5b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the CN¥7.15b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. At the end of the day, VNET Group would probably need a major re-capitalization if its creditors were to demand repayment. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine VNET Group's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, VNET Group reported revenue of CN¥7.7b, which is a gain of 4.8%, although it did not report any earnings before interest and tax. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, VNET Group had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost CN¥67m at the EBIT level. Combining this information with the significant liabilities we already touched on makes us very hesitant about this stock, to say the least. That said, it is possible that the company will turn its fortunes around. But we think that is unlikely, given it is low on liquid assets, and burned through CN¥2.2b in the last year. So we consider this a high risk stock and we wouldn't be at all surprised if the company asks shareholders for money before long. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for VNET Group (1 can't be ignored!) that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:VNET

VNET Group

An investment holding company, provides data center hosting and related services in China.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3448.6% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7100.7% overvalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.650.7% undervalued

25 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.0% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on UUE Holdings Berhad ·

UUE Holdings Trading at Deep Value Despite Strong Growth Prospects

Fair Value:RM 0.743.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PU

Pure_Research on Micron Technology ·

Strategic and Financial Blueprint of Micron Technology: Resolving the Memory Wall in the Gen-AI Era

Fair Value:US$2.02k48.3% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NI

niteco on Palantir Technologies ·

Palantir: Operating System for Government and Regulated Industry AI

Fair Value:US$361.5863.9% undervalued

12 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7443.3% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9638.7% undervalued

57 followersusers have followed this narrative

8 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.6% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

AC

ACV on Alignment Healthcare ·

high medical loss ratios, and negative free cash flow signal that scaling profitably remains elusive...

0

|0