Advertisement

- United States

- /

- Software

- /

- NasdaqGS:TEAM

Is Atlassian (NASDAQ:TEAM) Using Debt Sensibly?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Atlassian Corporation (NASDAQ:TEAM) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Atlassian

What Is Atlassian's Debt?

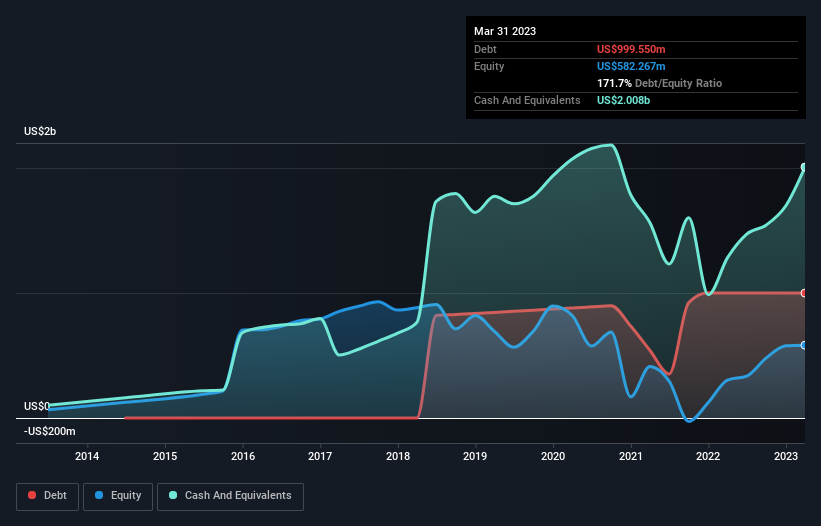

As you can see below, Atlassian had US$999.6m of debt, at March 2023, which is about the same as the year before. You can click the chart for greater detail. However, its balance sheet shows it holds US$2.01b in cash, so it actually has US$1.01b net cash.

A Look At Atlassian's Liabilities

The latest balance sheet data shows that Atlassian had liabilities of US$1.87b due within a year, and liabilities of US$1.38b falling due after that. Offsetting this, it had US$2.01b in cash and US$346.3m in receivables that were due within 12 months. So its liabilities total US$902.8m more than the combination of its cash and short-term receivables.

Of course, Atlassian has a titanic market capitalization of US$44.4b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Despite its noteworthy liabilities, Atlassian boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Atlassian's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Atlassian reported revenue of US$3.4b, which is a gain of 29%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Atlassian?

Although Atlassian had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of US$825m. So although it is loss-making, it doesn't seem to have too much near-term balance sheet risk, keeping in mind the net cash. The good news for Atlassian shareholders is that its revenue growth is strong, making it easier to raise capital if need be. But that doesn't change our opinion that the stock is risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 1 warning sign we've spotted with Atlassian .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:TEAM

Atlassian

Provides a collaboration software that enables organizations to connect all teams through a system of work that unlocks productivity at scale worldwide.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7061.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17036.6% undervalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.3% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.8% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

AY

Ayomiposi_X on CWG ·

63% Profit Growth, 6.8× Forward P/E: Inside CWG Plc's FY 2025 Numbers and What They Signal

Fair Value:₦3132.9% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WE

Westimnster on EPAM Systems ·

Expect EPAM's fair value to reach 59.38

Fair Value:US$113.3814.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28023.3% undervalued

89 followersusers have followed this narrative

9 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.7% undervalued

124 followersusers have followed this narrative

2 commentsusers have commented on this narrative

36 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.1% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1930.3% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative