Advertisement

- United States

- /

- Diversified Financial

- /

- NasdaqGS:PYPL

PayPal Holdings, Inc’s (NASDAQ:PYPL) Growth May Accelerate as Strategic Acquisitions Drive Network Effects

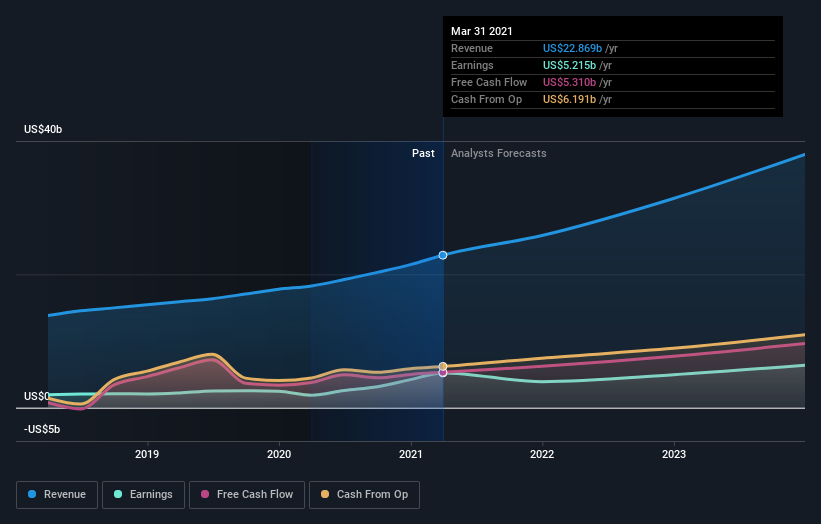

Tomorrow PayPal Holdings, Inc. ( NASDAQ:PYPL ) will release its financial results for the second quarter. Analysts are expecting revenue to be 19% higher than a year ago and EPS to be about 4.7% higher than a year ago. These growth rates may seem quite modest, but they are being measured against a very strong quarter last year.

We think PayPal is a company to keep an eye on, as there is potential for the company’s growth to accelerate in the future. PayPal is already over 20 years old, but it has only really gained momentum in the last five years. Case in point, PayPal’s market capitalization is now more than 2.5 times that of Goldman Sachs, while they were the same size just three years ago. The only bank that is’ worth more is JP Morgan Chase ( NYSE: JPM ).

There are several reasons that PayPal’s growth might accelerate in the future. Firstly, the company is making strategic acquisitions to build an ecosystem of fintech applications. Amongst these acquisitions have been Venmo, one of the most successful P2P payment apps and Xoom, a money transfer service. Each of these new services offers cross selling opportunities within the ecosystem. They also expand the value proposition for the platform as a whole.

Secondly, consumers are becoming increasingly comfortable using digital wallets and other fintech apps. PayPal and Square, Inc (NYSE: SQ) are the market leaders outside of China, and have strong brand recognition. This means consumers and merchants may be more likely to turn to one of these platforms.

PayPal recently announced that it will allow consumers to make payments using Bitcoin. The company has some way to go before it catches up with Square’s CashApp, but PayPal has more than ten times as many account holders to offer crypto services to. In time PayPal may become an important bridge between the conventional and crypto economies. PayPal may not be a leader in the crypto space, but it has more reach than any crypto company.

See our latest analysis for PayPal Holdings

What is PayPal Holdings worth?

The stock is currently trading at US$309 on the share market, which means it is overvalued by 31% compared to our intrinsic value estimate of $235.58. This means that the opportunity to buy PayPal Holdings at a good price has disappeared, unless future growth turns out to be higher than forecast.

Analysts are expecting revenue growth to be between 19 and 21% over the next three years. However, as indicated PayPal may be able to grow faster if its customer base grows and revenue per customer grows. This is by no means certain, but it is a reason to keep an eye on developments at PayPal.

Alternatively, a decline in the share price would give investors an opportunity to buy closer to the intrinsic value estimate. Given that PayPal Holdings’s share is fairly volatile (i.e. its price movements are magnified relative to the rest of the market) this could mean the price can sink lower, giving us another chance to buy in the future. This is based on its high beta, which is a good indicator for share price volatility.

What does the future of PayPal Holdings look like?

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Although value investors would argue that it’s the intrinsic value relative to the price that matters the most, a more compelling investment thesis would be high growth potential at a cheap price. PayPal Holdings' earnings over the next few years are expected to increase by 26%, indicating a highly optimistic future ahead. This should lead to more robust cash flows, feeding into a higher share value.

The Bottom Line

Based on current growth forecasts, PayPal does appear to be trading at a premium. However, growth has accelerated in the past, and may continue to accelerate the future. This may happen as PayPal adds new services which attract new customers while simultaneously increasing the revenue earned from each customer. The next step is to look for evidence that this strategy is working.

To get a sense of how the company is performing you can track the TPV, or Total Payments Volume, and the total number of accounts. These figures are included in PayPal’s financial results which are published each quarter.

If you want to dive deeper into PayPal Holdings, you'd also look into what risks it is currently facing. Every company has risks, and we've spotted 2 warning signs for PayPal Holdings you should know about.

If you are no longer interested in PayPal Holdings, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

Interactive Brokers Promoted

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

* Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:PYPL

PayPal Holdings

Operates a technology platform that enables digital payments for merchants and consumers worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.3% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

HA

Haha94 on Perdana Petroleum Berhad ·

Perdana Petroleum Berhad is a Zombie Business with a 27.34% Profit Margin and inflation adjusted revenue Business

Fair Value:RM 0.2128.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AB

Abc on Global X Etfs Icav - Global X Silver Miners Ucits ETF ·

Many trends acting at the same time

Fair Value:€10068.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$314.4446.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

109 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

941 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative