Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqCM:NVEC

Should You Buy NVE Corporation (NASDAQ:NVEC) For Its Dividend?

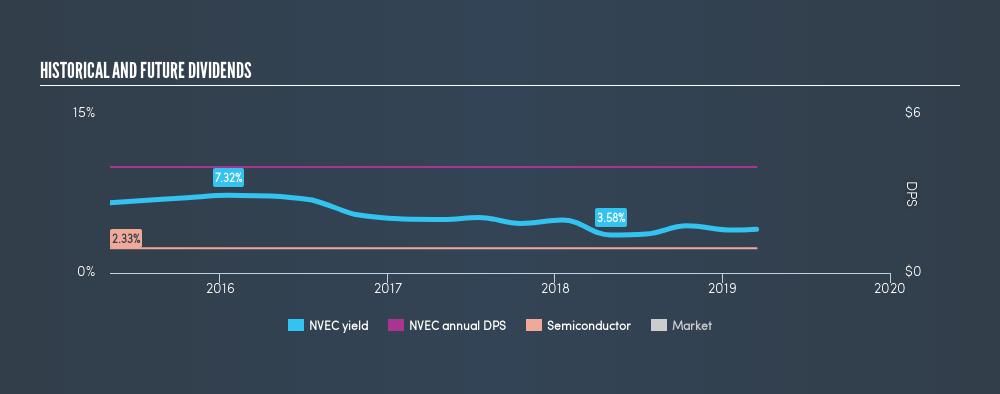

Dividends play an important role in compounding returns in the long run and end up forming a sizeable part of investment returns. In the last few years NVE Corporation (NASDAQ:NVEC) has paid a dividend to shareholders. Today it yields 4.1%. Let's dig deeper into whether NVE should have a place in your portfolio.

View our latest analysis for NVE

5 questions to ask before buying a dividend stock

When researching a dividend stock, I always follow the following screening criteria:

- Is it the top 25% annual dividend yield payer?

- Has it paid dividend every year without dramatically reducing payout in the past?

- Has it increased its dividend per share amount over the past?

- Can it afford to pay the current rate of dividends from its earnings?

- Will the company be able to keep paying dividend based on the future earnings growth?

Does NVE pass our checks?

The current trailing twelve-month payout ratio for NVEC is 125%, meaning the dividend is not sufficiently covered by its earnings. Furthermore, analysts have not forecasted a dividends per share for the future, which makes it hard to determine the yield shareholders should expect, and whether the current payout is sustainable, moving forward.

When assessing the forecast sustainability of a dividend it is also worth considering the cash flow of the business. Companies with strong cash flow can sustain a higher payout ratio, while companies with weaker cash flow generally cannot.

If there's one type of stock you want to be reliable, it's dividend stocks and their stable income-generating ability. Unfortunately, it is really too early to view NVE as a dividend investment. It has only been consistently paying dividends for 4 years, however, standard practice for reliable payers is to look for a 10-year minimum track record.

In terms of its peers, NVE generates a yield of 4.1%, which is high for Semiconductor stocks.

Next Steps:

After digging a little deeper into NVE's yield, it's easy to see why you should be cautious investing in the company just for the dividend. On the other hand, if you are not strictly just a dividend investor, the stock could still be offering some interesting investment opportunities. Given that this is purely a dividend analysis, I urge potential investors to try and get a good understanding of the underlying business and its fundamentals before deciding on an investment. There are three pertinent factors you should further examine:

- Future Outlook: What are well-informed industry analysts predicting for NVEC’s future growth? Take a look at our free research report of analyst consensus for NVEC’s outlook.

- Valuation: What is NVEC worth today? Even if the stock is a cash cow, it's not worth an infinite price. The intrinsic value infographic in our free research report helps visualize whether NVEC is currently mispriced by the market.

- Dividend Rockstars: Are there better dividend payers with stronger fundamentals out there? Check out our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqCM:NVEC

NVE

Develops and sells devices that use spintronics, a nanotechnology relying on electron spin to acquire, store, and transmit information, both in the United States and internationally.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|3.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6927.9% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8148.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.3% undervalued

131 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

81 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7921.6% undervalued

919 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative