Advertisement

- United States

- /

- Retail Distributors

- /

- NYSEAM:DIT

AMCON Distributing (NYSEMKT:DIT) Takes On Some Risk With Its Use Of Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that AMCON Distributing Company (NYSEMKT:DIT) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for AMCON Distributing

How Much Debt Does AMCON Distributing Carry?

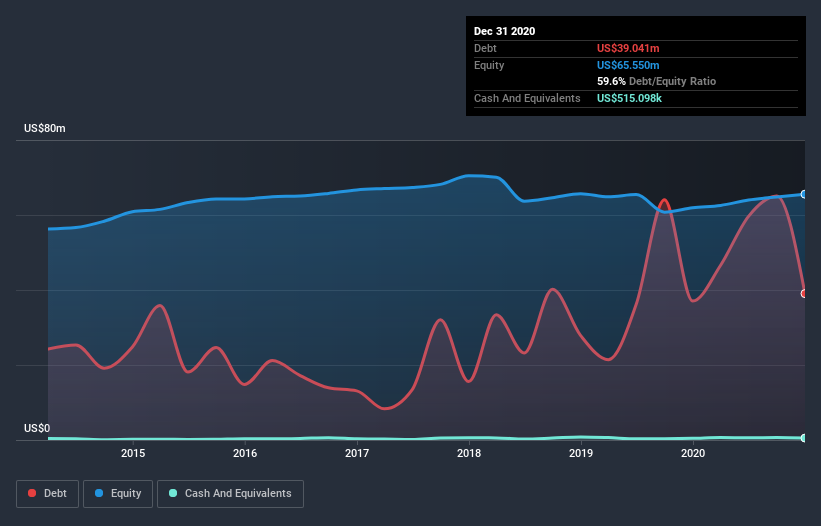

You can click the graphic below for the historical numbers, but it shows that as of December 2020 AMCON Distributing had US$39.0m of debt, an increase on US$37.1m, over one year. Net debt is about the same, since the it doesn't have much cash.

How Healthy Is AMCON Distributing's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that AMCON Distributing had liabilities of US$37.4m due within 12 months and liabilities of US$54.8m due beyond that. On the other hand, it had cash of US$515.1k and US$29.7m worth of receivables due within a year. So it has liabilities totalling US$62.0m more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of US$62.8m, so it does suggest shareholders should keep an eye on AMCON Distributing's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With a debt to EBITDA ratio of 2.5, AMCON Distributing uses debt artfully but responsibly. And the fact that its trailing twelve months of EBIT was 7.8 times its interest expenses harmonizes with that theme. Importantly, AMCON Distributing grew its EBIT by 50% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since AMCON Distributing will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Looking at the most recent three years, AMCON Distributing recorded free cash flow of 28% of its EBIT, which is weaker than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

AMCON Distributing's level of total liabilities and conversion of EBIT to free cash flow definitely weigh on it, in our esteem. But the good news is it seems to be able to grow its EBIT with ease. We think that AMCON Distributing's debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 3 warning signs for AMCON Distributing (of which 1 is concerning!) you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you decide to trade AMCON Distributing, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSEAM:DIT

AMCON Distributing

Engages in the wholesale distribution of consumer products in the Central, Rocky Mountain, and Mid-South regions of the United States.

Moderate risk second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor