Stock Analysis

- United States

- /

- Specialty Stores

- /

- NYSE:BOOT

What Is Boot Barn Holdings's (NYSE:BOOT) P/E Ratio After Its Share Price Tanked?

To the annoyance of some shareholders, Boot Barn Holdings (NYSE:BOOT) shares are down a considerable 68% in the last month. And that drop will have no doubt have some shareholders concerned that the 62% share price decline, over the last year, has turned them into bagholders. For those wondering, a bagholder is someone who keeps holding a losing stock indefinitely, without taking the time to consider its prospects carefully, going forward.

Assuming nothing else has changed, a lower share price makes a stock more attractive to potential buyers. While the market sentiment towards a stock is very changeable, in the long run, the share price will tend to move in the same direction as earnings per share. So, on certain occasions, long term focussed investors try to take advantage of pessimistic expectations to buy shares at a better price. One way to gauge market expectations of a stock is to look at its Price to Earnings Ratio (PE Ratio). A high P/E implies that investors have high expectations of what a company can achieve compared to a company with a low P/E ratio.

See our latest analysis for Boot Barn Holdings

Does Boot Barn Holdings Have A Relatively High Or Low P/E For Its Industry?

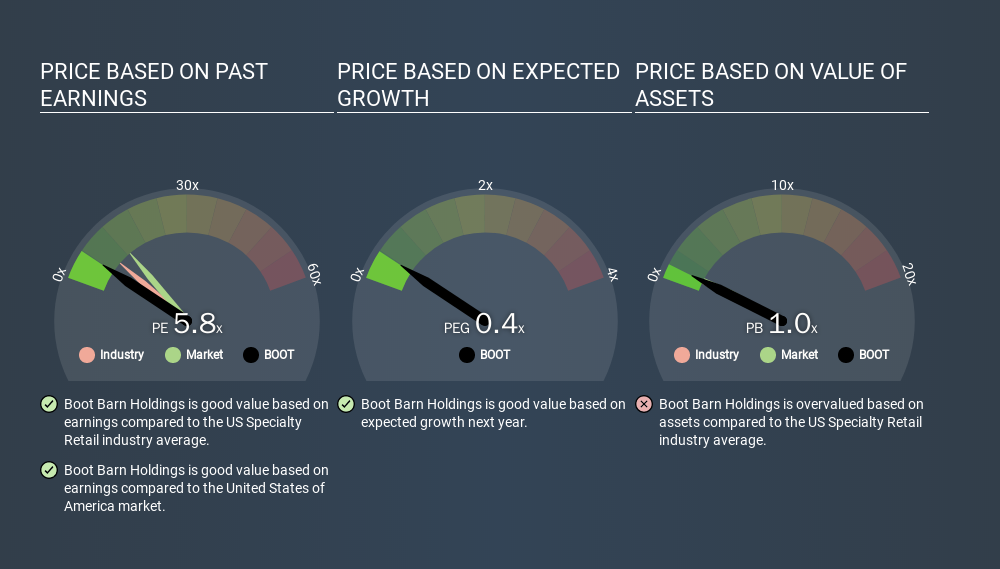

Boot Barn Holdings's P/E of 5.85 indicates relatively low sentiment towards the stock. The image below shows that Boot Barn Holdings has a lower P/E than the average (7.4) P/E for companies in the specialty retail industry.

Boot Barn Holdings's P/E tells us that market participants think it will not fare as well as its peers in the same industry. Many investors like to buy stocks when the market is pessimistic about their prospects. It is arguably worth checking if insiders are buying shares, because that might imply they believe the stock is undervalued.

How Growth Rates Impact P/E Ratios

Generally speaking the rate of earnings growth has a profound impact on a company's P/E multiple. That's because companies that grow earnings per share quickly will rapidly increase the 'E' in the equation. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. Then, a lower P/E should attract more buyers, pushing the share price up.

Notably, Boot Barn Holdings grew EPS by a whopping 34% in the last year. And its annual EPS growth rate over 5 years is 26%. I'd therefore be a little surprised if its P/E ratio was not relatively high.

Remember: P/E Ratios Don't Consider The Balance Sheet

The 'Price' in P/E reflects the market capitalization of the company. In other words, it does not consider any debt or cash that the company may have on the balance sheet. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Such expenditure might be good or bad, in the long term, but the point here is that the balance sheet is not reflected by this ratio.

So What Does Boot Barn Holdings's Balance Sheet Tell Us?

Boot Barn Holdings's net debt equates to 36% of its market capitalization. You'd want to be aware of this fact, but it doesn't bother us.

The Bottom Line On Boot Barn Holdings's P/E Ratio

Boot Barn Holdings has a P/E of 5.8. That's below the average in the US market, which is 11.8. The company does have a little debt, and EPS growth was good last year. If it continues to grow, then the current low P/E may prove to be unjustified. Since analysts are predicting growth will continue, one might expect to see a higher P/E so it may be worth looking closer. What can be absolutely certain is that the market has become more pessimistic about Boot Barn Holdings over the last month, with the P/E ratio falling from 18.4 back then to 5.8 today. For those who prefer invest in growth, this stock apparently offers limited promise, but the deep value investors may find the pessimism around this stock enticing.

Investors should be looking to buy stocks that the market is wrong about. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine. So this free visual report on analyst forecasts could hold the key to an excellent investment decision.

Of course you might be able to find a better stock than Boot Barn Holdings. So you may wish to see this free collection of other companies that have grown earnings strongly.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:BOOT

Boot Barn Holdings

Operates specialty retail stores in the United States and internationally.

Flawless balance sheet with limited growth.