Advertisement

- United States

- /

- Retail Distributors

- /

- NasdaqGM:EDUC

What Educational Development Corporation's (NASDAQ:EDUC) 28% Share Price Gain Is Not Telling You

The Educational Development Corporation (NASDAQ:EDUC) share price has done very well over the last month, posting an excellent gain of 28%. The last 30 days bring the annual gain to a very sharp 43%.

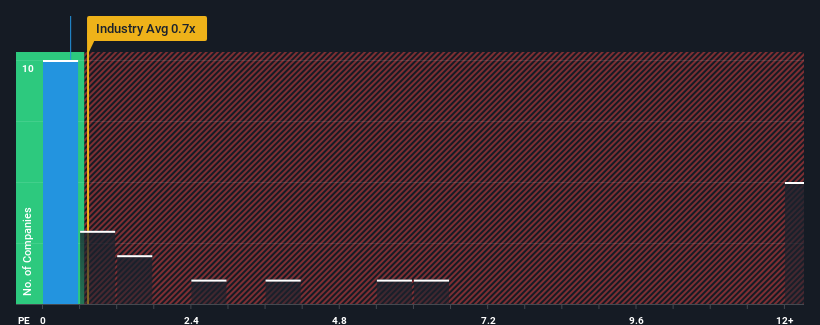

In spite of the firm bounce in price, there still wouldn't be many who think Educational Development's price-to-sales (or "P/S") ratio of 0.4x is worth a mention when the median P/S in the United States' Retail Distributors industry is similar at about 0.5x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Educational Development

What Does Educational Development's Recent Performance Look Like?

For instance, Educational Development's receding revenue in recent times would have to be some food for thought. One possibility is that the P/S is moderate because investors think the company might still do enough to be in line with the broader industry in the near future. If you like the company, you'd at least be hoping this is the case so that you could potentially pick up some stock while it's not quite in favour.

Although there are no analyst estimates available for Educational Development, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is Educational Development's Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Educational Development's is when the company's growth is tracking the industry closely.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 41%. The last three years don't look nice either as the company has shrunk revenue by 78% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Comparing that to the industry, which is predicted to deliver 3.2% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

With this information, we find it concerning that Educational Development is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company are way less bearish than recent times would indicate and aren't willing to let go of their stock right now. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh on the share price eventually.

The Final Word

Educational Development's stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look at Educational Development revealed its shrinking revenues over the medium-term haven't impacted the P/S as much as we anticipated, given the industry is set to grow. Even though it matches the industry, we're uncomfortable with the current P/S ratio, as this dismal revenue performance is unlikely to support a more positive sentiment for long. Unless the the circumstances surrounding the recent medium-term improve, it wouldn't be wrong to expect a a difficult period ahead for the company's shareholders.

Before you take the next step, you should know about the 5 warning signs for Educational Development (1 shouldn't be ignored!) that we have uncovered.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Educational Development might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:EDUC

Educational Development

Distributes children's books, educational toys and games, and related products in the United States.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.563.5% undervalued

49 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.826.3% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23055.3% overvalued

54 followersusers have followed this narrative

1 commentusers have commented on this narrative

14 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.6% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30155.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BI

bip59 on Apple ·

Perfect Hardware, Dated Software: Why I See Apple at $100 in 3 Years

Fair Value:US$100215.3% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LI

Lijo on Accenture ·

A value stock that's undervalued.

Fair Value:US$18326.1% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.8% undervalued

87 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5448.2% undervalued

60 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7107.2% undervalued

53 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative