Advertisement

- United States

- /

- Office REITs

- /

- NYSE:KRC

Does Kilroy Realty’s Q3 Earnings Surge Signal a Lasting Portfolio Transformation for KRC?

Simply Wall St

Reviewed by Sasha Jovanovic

- Kilroy Realty Corporation recently reported its third quarter 2025 earnings, highlighting US$279.74 million in revenue and a significant jump in net income to US$156.22 million, mainly due to gains on property sales and active leasing efforts.

- In addition to improved earnings, the company updated its full-year guidance for funds from operations and continued to execute on acquisitions and dispositions, emphasizing an ongoing transformation of its portfolio.

- We'll explore how Kilroy Realty's strong leasing momentum and property sales impact the company's investment narrative amid shifting office demand trends.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Kilroy Realty Investment Narrative Recap

To own shares of Kilroy Realty, you need to believe in the company's ability to maintain leasing momentum and optimize its West Coast portfolio, even as long-term office demand remains uncertain due to remote and hybrid work trends. The recent earnings report, driven by gains on property sales and strong leasing, supports the most important short term catalyst, improved portfolio quality, while the biggest risk remains persistent pressure on occupancy rates; this news does not appear to shift that risk-reward balance in a material way.

Among recent announcements, the acquisition of Maple Plaza stands out, reinforcing Kilroy’s focus on trophy assets in high-demand submarkets. This aligns with the company’s ongoing shift toward innovation clusters and underscores leasing and development as the key catalysts, especially with the goal of enhancing long-term cash flows.

In contrast, investors should also be aware of the financial pressures that can build as office demand shifts...

Read the full narrative on Kilroy Realty (it's free!)

Kilroy Realty is projected to have $1.1 billion in revenue and $64.0 million in earnings by 2028. This outlook assumes a 0.2% annual revenue decline and a $154.5 million decrease in earnings from the current $218.5 million level.

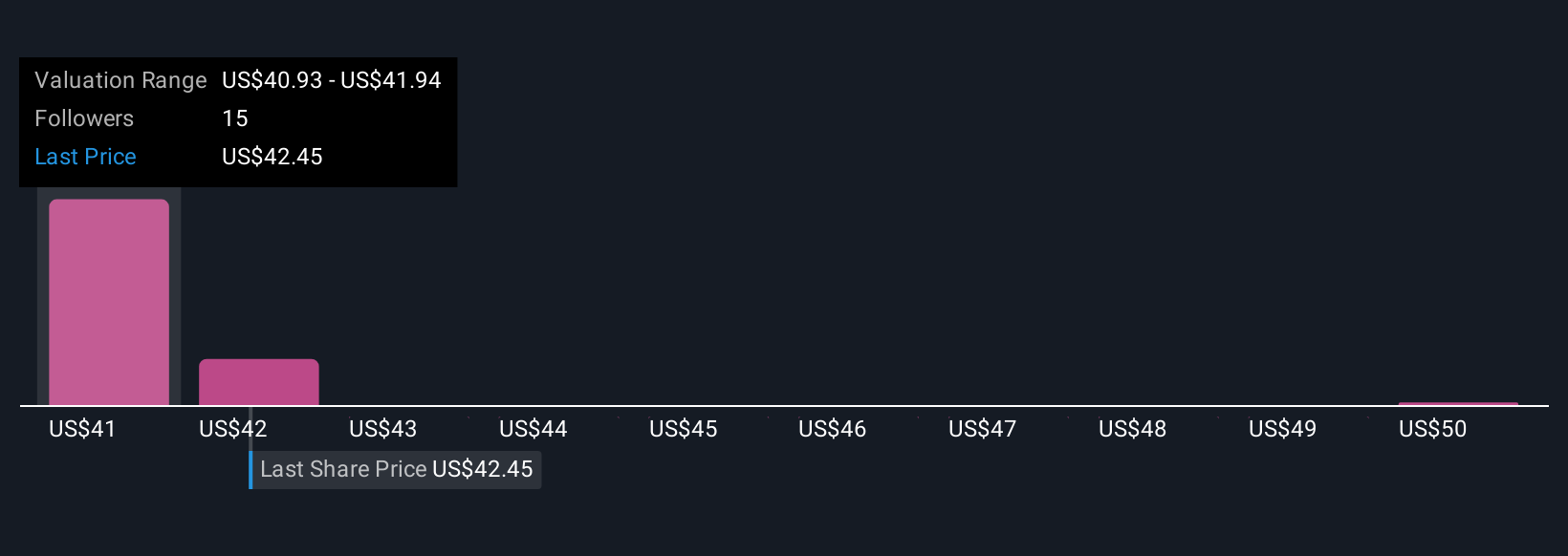

Uncover how Kilroy Realty's forecasts yield a $42.00 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members set fair value estimates for Kilroy Realty shares ranging from US$42.00 to US$51.04, highlighting three individual views. Given ongoing office demand uncertainty, these differences reflect broad debates about future occupancy and growth, explore the full spread of opinions for more insights.

Explore 3 other fair value estimates on Kilroy Realty - why the stock might be worth just $42.00!

Build Your Own Kilroy Realty Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kilroy Realty research is our analysis highlighting 4 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Kilroy Realty research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kilroy Realty's overall financial health at a glance.

Looking For Alternative Opportunities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Rare earth metals are the new gold rush. Find out which 35 stocks are leading the charge.

- We've found 24 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kilroy Realty might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KRC

Kilroy Realty

Kilroy is a leading U.S. landlord and developer, with operations in San Diego, Los Angeles, the San Francisco Bay Area, Seattle, and Austin.

6 star dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor