Advertisement

- United States

- /

- Office REITs

- /

- NYSE:BXP

Should BXP’s (BXP) Pivot to Acquisitions Amid Losses Signal a New Long-Term Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- BXP, Inc. reported third quarter 2025 results showing a net loss of US$121.71 million on revenues of US$871.51 million, and provided earnings guidance for full-year 2025 with expected EPS between US$0.99 and US$1.02, both below prior periods.

- Despite launching nearly US$2.5 billion in new office developments and exploring acquisitions, BXP’s recent results highlight ongoing profitability challenges in the current market environment.

- We'll explore how BXP's shift toward acquisitions and cautious 2025 outlook may reshape the company's long-term investment narrative.

This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

BXP Investment Narrative Recap

To be a shareholder in BXP, investors need to believe in a recovery of office market fundamentals and the company’s ability to turn new developments and selective acquisitions into sustainable earnings growth. The recent quarterly loss and cautious earnings outlook reinforce near-term pressure on profitability, but do not materially alter the biggest short-term catalyst, leasing momentum in core assets, or the main risk, which remains persistent weakness in occupancy and rent growth.

Among recent announcements, BXP’s move to seek acquisitions, while maintaining an emphasis on higher yields and disciplined capital allocation, stands out. This measured approach aims to balance development with acquisition opportunities and keep the focus on returns, yet the willingness to deploy new capital could heighten sensitivity to ongoing leasing risks if portfolio occupancy lags expectations.

However, investors should also be aware that despite BXP’s strong asset base, the risk from ongoing tenant churn and sluggish rent growth could...

Read the full narrative on BXP (it's free!)

BXP's narrative projects $3.7 billion in revenue and $368.8 million in earnings by 2028. This requires a 2.5% yearly revenue growth rate and an earnings increase of about $364 million from current earnings of $4.9 million.

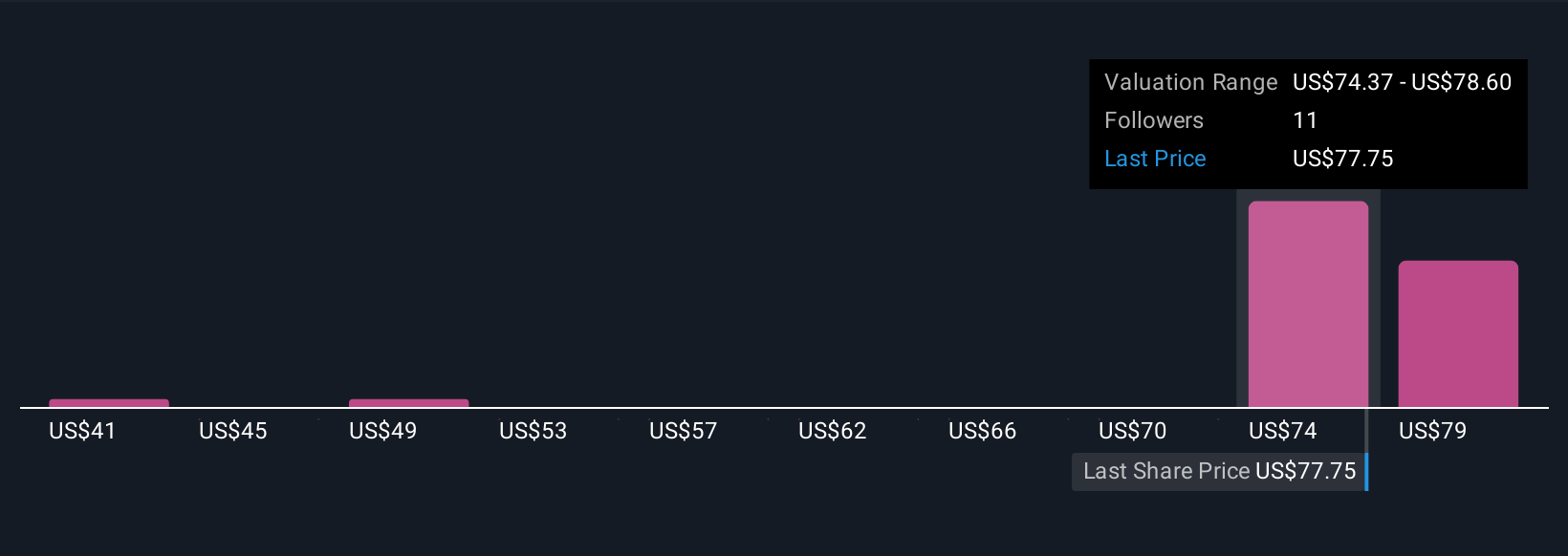

Uncover how BXP's forecasts yield a $79.50 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community estimated BXP's fair value from as low as US$40.50 to just above US$81.93. With market opinions this wide, especially given ongoing pressure on occupancy and rents, you can compare alternate views of BXP’s outlook before making your own judgment.

Explore 4 other fair value estimates on BXP - why the stock might be worth 43% less than the current price!

Build Your Own BXP Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your BXP research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free BXP research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate BXP's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BXP might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BXP

BXP

BXP, Inc. (NYSE: BXP) is the largest publicly traded developer, owner, and manager of premier workplaces in the United States, concentrated in six dynamic gateway markets - Boston, Los Angeles, New York, San Francisco, Seattle, and Washington, DC.

Established dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor