Stock Analysis

- United States

- /

- Hotel and Resort REITs

- /

- NYSE:AHT

Time To Worry? Analysts Are Downgrading Their Ashford Hospitality Trust, Inc. (NYSE:AHT) Outlook

Market forces rained on the parade of Ashford Hospitality Trust, Inc. (NYSE:AHT) shareholders today, when the analysts downgraded their forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analysts seeing grey clouds on the horizon.

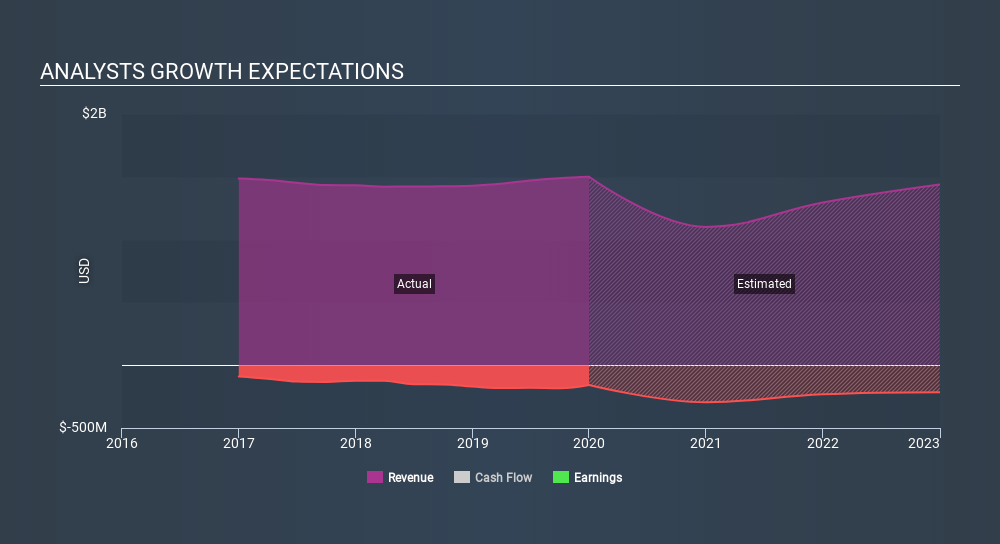

Following the latest downgrade, the five analysts covering Ashford Hospitality Trust provided consensus estimates of US$1.1b revenue in 2020, which would reflect a sizeable 27% decline on its sales over the past 12 months. Losses are supposed to balloon 143% to US$3.84 per share. However, before this estimates update, the consensus had been expecting revenues of US$1.4b and US$0.62 per share in losses. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a serious cut to their revenue forecasts while also expecting losses per share to increase.

View our latest analysis for Ashford Hospitality Trust

The consensus price target fell 40% to US$1.51, with the analysts clearly concerned about the company following the weaker revenue and earnings outlook. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Ashford Hospitality Trust at US$2.00 per share, while the most bearish prices it at US$0.75. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. These estimates imply that sales are expected to slow, with a forecast revenue decline of 27%, a significant reduction from annual growth of 7.0% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 4.3% annually for the foreseeable future. It's pretty clear that Ashford Hospitality Trust's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to note from this downgrade is that the consensus increased its forecast losses this year, suggesting all may not be well at Ashford Hospitality Trust. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Ashford Hospitality Trust's revenues are expected to grow slower than the wider market. With a serious cut to this year's expectations and a falling price target, we wouldn't be surprised if investors were becoming wary of Ashford Hospitality Trust.

So things certainly aren't looking great, and you should also know that we've spotted some potential warning signs with Ashford Hospitality Trust, including dilutive stock issuance over the past year. Learn more, and discover the 4 other risks we've identified, for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:AHT

Ashford Hospitality Trust

Ashford Hospitality Trust is a real estate investment trust (REIT) focused on investing predominantly in upper upscale, full-service hotels.

Undervalued with imperfect balance sheet.