Advertisement

- United States

- /

- Biotech

- /

- NYSE:EBS

Emergent BioSolutions (EBS): Evaluating Valuation After Raised 2025 Guidance and Strong Q3 Results

Emergent BioSolutions (EBS) captured investors' attention after reporting third-quarter results that topped revenue and profitability expectations. Management responded by raising full-year 2025 revenue and adjusted EBITDA guidance following these strong results.

See our latest analysis for Emergent BioSolutions.

Emergent BioSolutions has staged a remarkable turnaround lately, with a 36% jump in its 1-month share price return and an eye-catching 110% surge over the last 90 days. This rapid momentum comes after recently upgraded guidance, new government contracts, and a completed buyback program, suggesting that renewed confidence is taking hold among investors. While the stock's 1-year total shareholder return is a solid 37%, its longer-term returns remain deeply negative, indicating the recovery is still taking shape.

If you're interested in uncovering what else is capturing attention in healthcare, consider expanding your search and explore See the full list for free.

With shares surging in recent months and management raising guidance for 2025, the big question for investors now is whether Emergent BioSolutions still has upside potential or if future growth has already been fully priced in.

Most Popular Narrative: 7.6% Undervalued

After closing at $12.48, Emergent BioSolutions looks mispriced compared to the narrative's fair value estimate of $13.5. Stakeholders appear divided on whether this gap can close, setting up a pivotal moment for the stock.

Expansion of international revenues, now accounting for 40 to 48% of medical countermeasure sales year-to-date, demonstrates successful penetration into new markets and positions Emergent to benefit from rising global health threats and prioritization of pandemic preparedness. This drives both revenue growth and diversification.

Curious how bold international moves and shifting global health priorities are factored into Emergent's valuation? Rumor has it, the secret sauce in this narrative is built on future profitability targets and a valuation multiple that defies current market sentiment. Want to see what projections the analysts are really betting on? The surprising narrative calculations are just a click away.

Result: Fair Value of $13.5 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, risks remain. Heavy reliance on government contracts or a slowdown in new contract wins could threaten the recovery narrative for Emergent BioSolutions.

Find out about the key risks to this Emergent BioSolutions narrative.

Another View: Is the Market Too Optimistic?

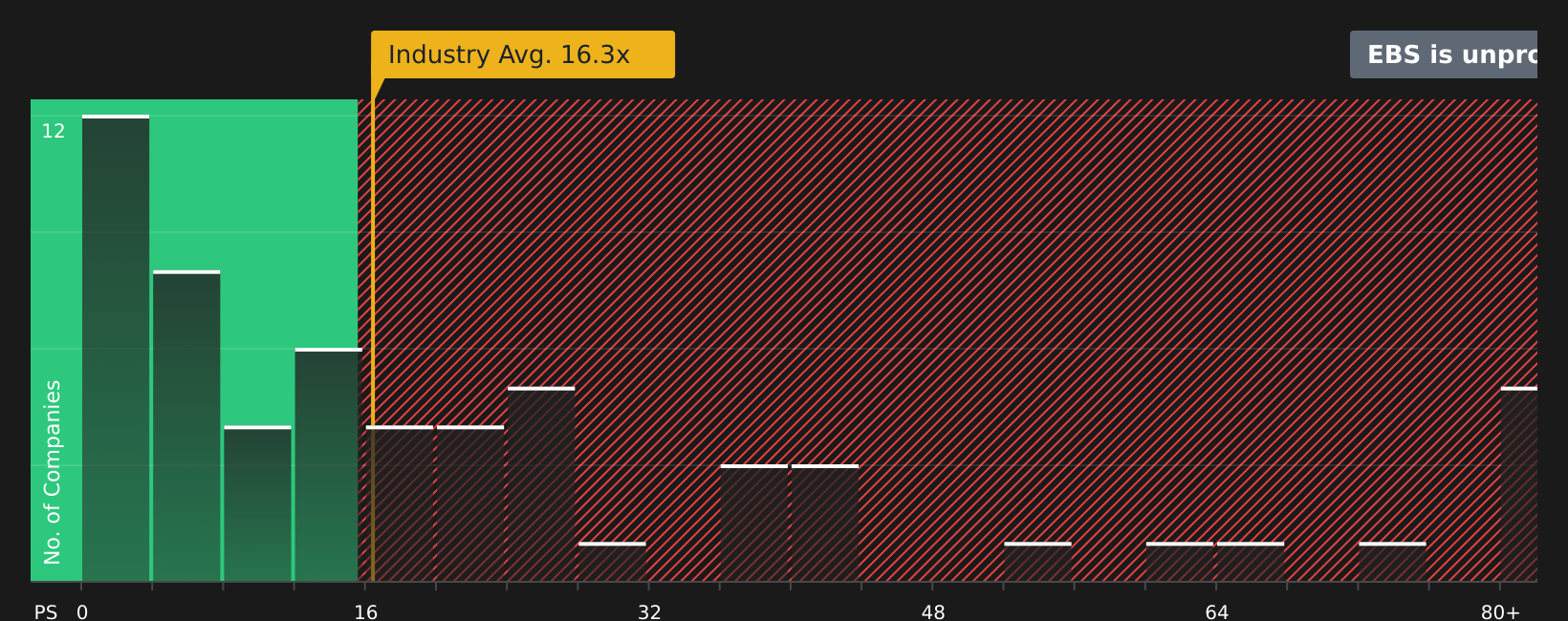

Taking a step back and looking at the company's price-to-earnings ratio paints a different picture. Emergent BioSolutions is valued at 8.6x earnings, which is well below similar US biotech companies, averaging 17.7x. However, compared to its estimated fair ratio of 5.4x, this signals the stock might actually be expensive. Is the market overlooking some risks, or is there hidden upside?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Emergent BioSolutions Narrative

If you want to challenge this perspective or dig deeper into the numbers, you can craft your own Emergent narrative in just a few minutes. Do it your way

A great starting point for your Emergent BioSolutions research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors never stop searching for their next edge. Don’t let opportunity pass you by. Uncover stocks shaking up their spaces and unlocking hidden value below.

- Tap into income potential with these 22 dividend stocks with yields > 3% that reward shareholders with high yields above 3% and solid financials backing every payout.

- Spot tomorrow’s industry leaders with these 26 AI penny stocks riding the AI revolution and powering breakthroughs across every sector.

- Find value where others overlook by targeting these 840 undervalued stocks based on cash flows poised for growth based on robust cash flows and healthy fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Emergent BioSolutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EBS

Emergent BioSolutions

A life sciences company, provides preparedness and response solutions for accidental, deliberate, and naturally occurring public health threats in the United States, Canada, and internationally.

Undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4351.3% undervalued

77 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8166.9% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

BR

Bradders3 on CT Global Managed Portfolio Trust ·

Neat way of diversifying

Fair Value:UK£1.290% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BR

BrandonM84 on Lightwave Logic ·

Pre Commercialization optimism

Fair Value:US$74.182.7% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on DIGITAL HEARTS HOLDINGS ·

Strategic pivot in maximizing corporate value

Fair Value:JP¥928.1618.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.4% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6119.9% undervalued

1195 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative