Advertisement

- United States

- /

- Biotech

- /

- OTCPK:MTEM.Q

Earnings Release: Here's Why Analysts Cut Their Molecular Templates, Inc. (NASDAQ:MTEM) Price Target To US$18.00

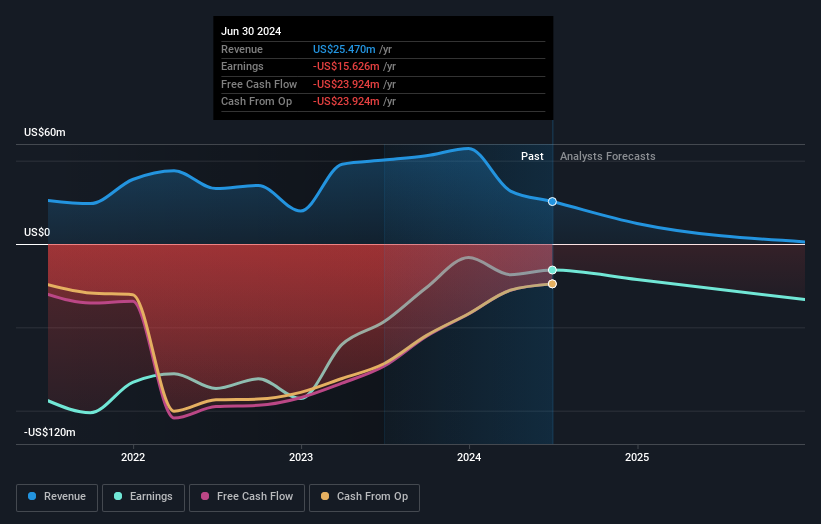

Molecular Templates, Inc. (NASDAQ:MTEM) just released its latest second-quarter report and things are not looking great. Statutory earnings fell substantially short of expectations, with revenues of US$572k missing forecasts by 91%. Losses exploded, with a per-share loss of US$1.23 some 162% below prior forecasts. The analyst typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analyst latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for Molecular Templates

Taking into account the latest results, the current consensus, from the solitary analyst covering Molecular Templates, is for revenues of US$12.3m in 2024. This implies a disturbing 52% reduction in Molecular Templates' revenue over the past 12 months. Per-share losses are expected to explode, reaching US$2.90 per share. Before this earnings announcement, the analyst had been modelling revenues of US$12.7m and losses of US$3.25 per share in 2024. While the revenue estimates fell, sentiment seems to have improved, with the analyst making a favorable reduction in losses per share in particular.

The analyst has cut their price target 52% to US$18.00per share, suggesting that the declining revenue was a more crucial indicator than the forecast reduction in losses.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 77% by the end of 2024. This indicates a significant reduction from annual growth of 17% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 23% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Molecular Templates is expected to lag the wider industry.

The Bottom Line

The most obvious conclusion is that the analyst made no changes to their forecasts for a loss next year. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. Even so, earnings per share are more important to the intrinsic value of the business. The consensus price target fell measurably, with the analyst seemingly not reassured by the latest results, leading to a lower estimate of Molecular Templates' future valuation.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Molecular Templates going out as far as 2025, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 6 warning signs for Molecular Templates (3 can't be ignored!) that you should be aware of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:MTEM.Q

Molecular Templates

A clinical stage biopharmaceutical company, focuses on the discovery and development of biologic therapeutics for the treatment of cancer and other serious diseases in the United States.

Adequate balance sheet low.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.1% undervalued

TI

Community Contributor