Advertisement

- United States

- /

- Media

- /

- NYSE:TSQ

Townsquare Media's (NYSE:TSQ) Shareholders Will Receive A Bigger Dividend Than Last Year

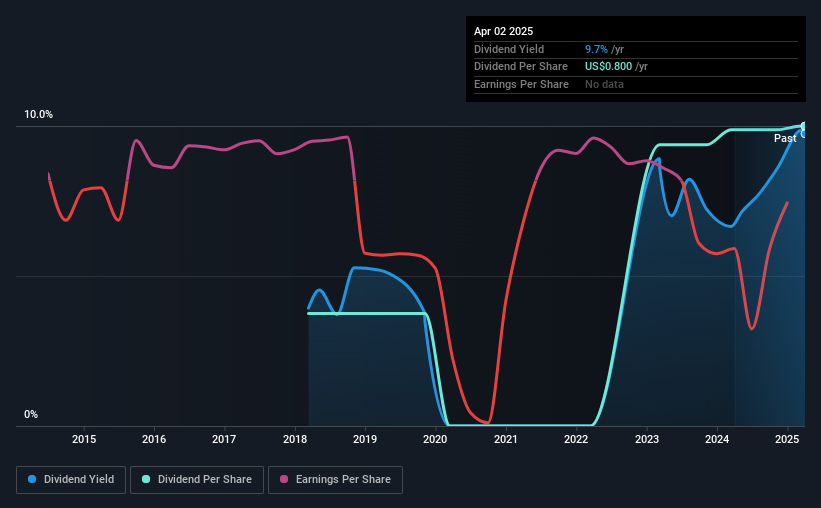

Townsquare Media, Inc. (NYSE:TSQ) will increase its dividend from last year's comparable payment on the 1st of May to $0.20. This will take the dividend yield to an attractive 9.7%, providing a nice boost to shareholder returns.

Townsquare Media Might Find It Hard To Continue The Dividend

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Townsquare Media is not generating a profit, but its free cash flows easily cover the dividend, leaving plenty for reinvestment in the business. We generally think that cash flow is more important than accounting measures of profit, so we are fairly comfortable with the dividend at this level.

Looking forward, earnings per share is forecast to expand by 70.5% over the next year. We like to see the company moving towards profitability, but this probably won't be enough for it to post positive net income this year. However, the positive cash flow ratio gives us some comfort about the sustainability of the dividend.

See our latest analysis for Townsquare Media

Townsquare Media's Dividend Has Lacked Consistency

It's comforting to see that Townsquare Media has been paying a dividend for a number of years now, however it has been cut at least once in that time. This suggests that the dividend might not be the most reliable. Since 2018, the dividend has gone from $0.30 total annually to $0.80. This works out to be a compound annual growth rate (CAGR) of approximately 15% a year over that time. It is great to see strong growth in the dividend payments, but cuts are concerning as it may indicate the payout policy is too ambitious.

The Company Could Face Some Challenges Growing The Dividend

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. We are encouraged to see that Townsquare Media has grown earnings per share at 25% per year over the past five years. While the company hasn't yet recorded a profit, the growth rates are healthy. If the company can turn a profit relatively soon, we can see this becoming a reliable income stock.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think Townsquare Media's payments are rock solid. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. To that end, Townsquare Media has 3 warning signs (and 1 which doesn't sit too well with us) we think you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Townsquare Media might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:TSQ

Townsquare Media

Operates as a digital and broadcast media, and digital marketing solutions company for small and medium-sized businesses in the United States.

Undervalued with moderate risk and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor