Stock Analysis

- United States

- /

- Media

- /

- NYSE:CCO

Exploring Three Undervalued Small Caps With Insider Action In The Region

Reviewed by Simply Wall St

In a week marked by modest gains across major U.S. stock indexes and a notable performance uplift in small-cap companies, the investment landscape appears cautiously optimistic as investors await more definitive cues from upcoming quarterly earnings reports. Amid these conditions, exploring undervalued small caps with recent insider action might reveal potential opportunities for those looking to diversify their portfolios in this segment of the market.

Top 10 Undervalued Small Caps With Insider Buying

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Columbus McKinnon | 20.9x | 1.0x | 46.09% | ★★★★★☆ |

| Semen Indonesia (Persero) | 12.8x | 0.7x | 23.01% | ★★★★★☆ |

| East West Banking | 3.4x | 0.7x | 49.23% | ★★★★★☆ |

| RAM Essential Services Property Fund | NA | 5.6x | 41.98% | ★★★★★☆ |

| Healius | NA | 0.6x | 43.72% | ★★★★★☆ |

| Dicker Data | 20.7x | 0.8x | 4.00% | ★★★★☆☆ |

| China Leon Inspection Holding | 10.1x | 0.7x | 25.37% | ★★★★☆☆ |

| Giordano International | 8.7x | 0.8x | 36.02% | ★★★☆☆☆ |

| Tai Sin Electric | 15.0x | 0.5x | 5.20% | ★★★☆☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

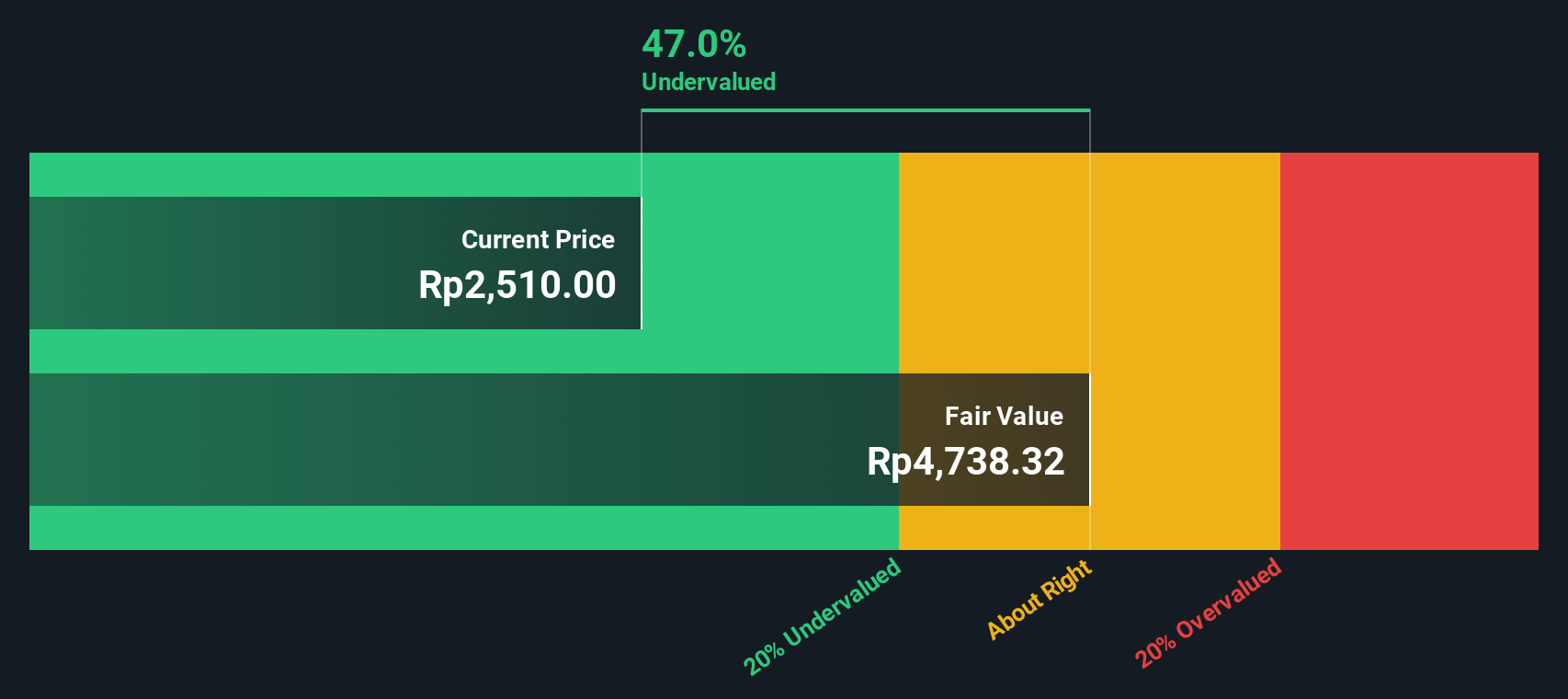

Semen Indonesia (Persero) (IDX:SMGR)

Simply Wall St Value Rating: ★★★★★☆

Overview: Semen Indonesia is a company engaged in the production of cement and non-cement products, with a market capitalization of approximately IDR 34.11 billion.

Operations: Cement Production and Non-Cement Production are the primary revenue contributors for the company, generating IDR 34.11 billion and IDR 13.13 billion respectively. Over recent periods, the Gross Profit Margin has shown variability, with a notable figure of 0.26% by the end of the latest period reported.

PE: 12.8x

Recently, Semen Indonesia demonstrated insider confidence with purchases signaling belief in the company's potential despite a dip in first quarter sales to IDR 8,375 million from IDR 8,935 million year-over-year and a decrease in net income. At the Macquarie Asia Conference, they highlighted strategies poised to reverse these trends. With earnings expected to grow by 13.5% annually and reliance solely on external borrowing—devoid of customer deposits—the firm presents a compelling narrative for growth amidst its industry peers.

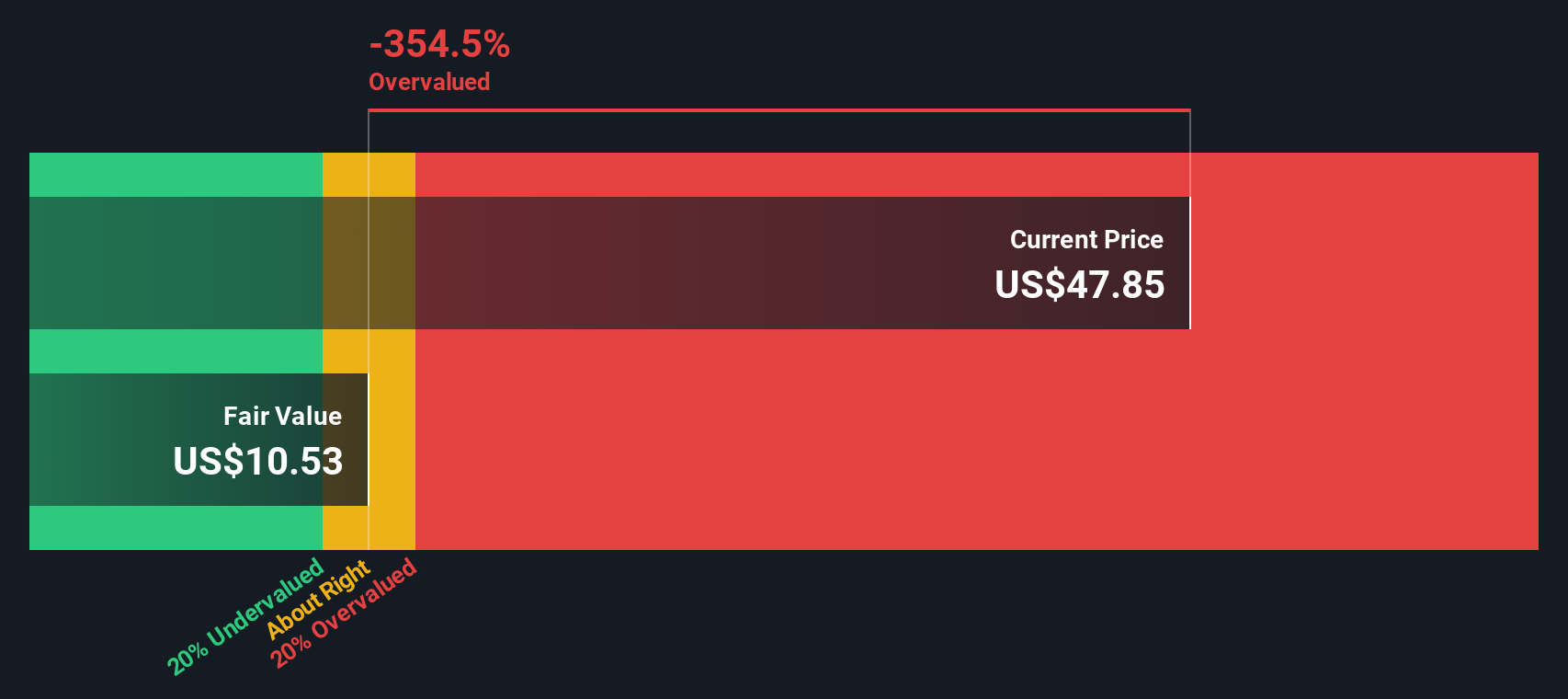

Ramaco Resources (NasdaqGS:METC)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Ramaco Resources is a company engaged in the coal mining sector, with a market capitalization of approximately $699.84 million.

Operations: In recent financial data, the company reported a revenue of $699.84 million with a net income of $56.32 million. The gross profit margin stood at 25.27%, reflecting the cost of goods sold at $522.96 million and gross profit at $176.88 million, indicating operational efficiency in managing production costs relative to sales revenue.

PE: 13.3x

Recently, Ramaco Resources has seen significant insider confidence, with key figures purchasing shares, signaling strong belief in the company's prospects despite a challenging financial landscape marked by a profit margin decrease from 17.3% to 8%. This move coincides with their inclusion in several growth-oriented indexes like the Russell 2000 and Russell 3000 Growth Indexes as of July 1, 2024. These developments suggest a strategic pivot towards growth sectors, supported by leadership's tangible commitment through equity investment.

- Click to explore a detailed breakdown of our findings in Ramaco Resources' valuation report.

Examine Ramaco Resources' past performance report to understand how it has performed in the past.

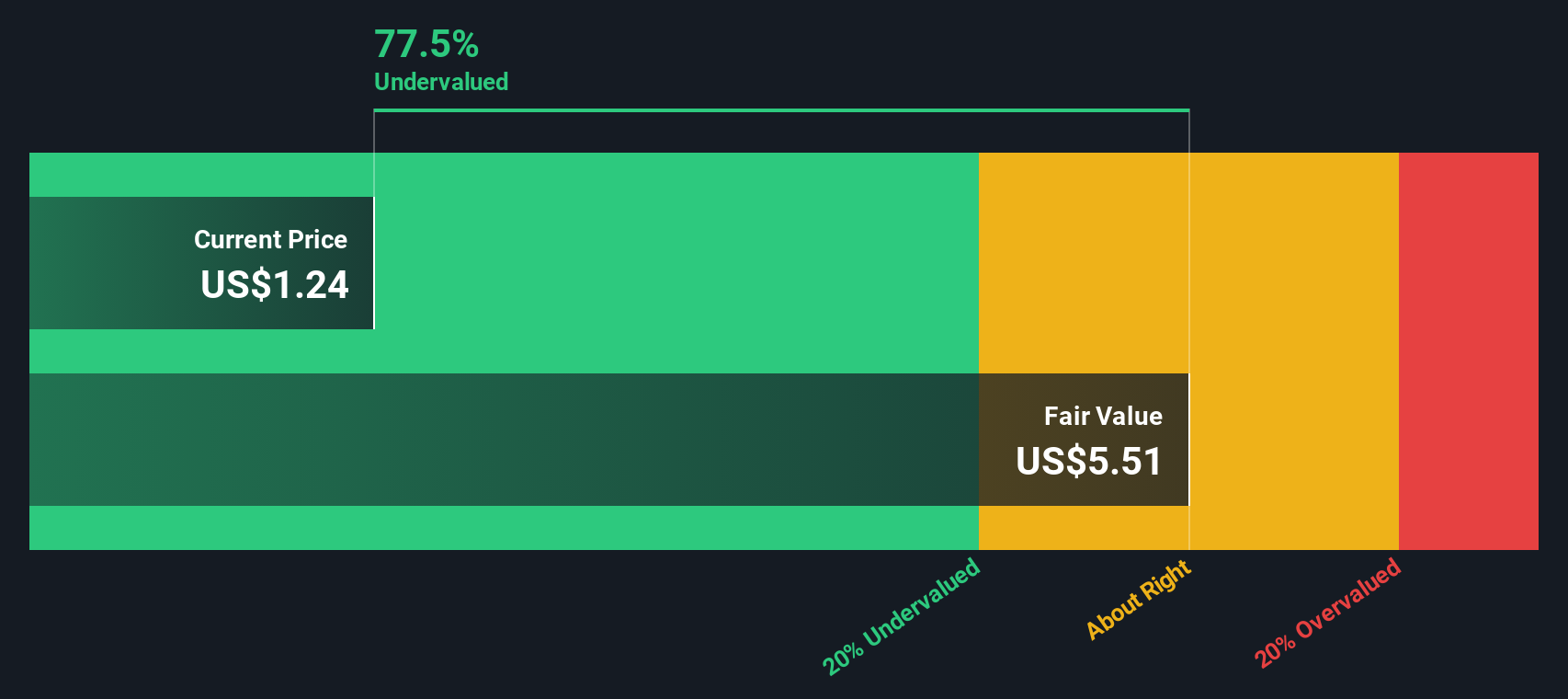

Clear Channel Outdoor Holdings (NYSE:CCO)

Simply Wall St Value Rating: ★★★★★☆

Overview: Clear Channel Outdoor Holdings is a global outdoor advertising company with operations spanning America and Europe, including airports, and has a market capitalization of approximately $0.65 billion.

Operations: The company generates its revenue from diverse geographical segments including America (excluding airports), Europe-north, and Airports, with respective revenues of $1.11 billion, $630.45 million, and $334.74 million. It has experienced a gross profit margin fluctuation over recent periods, recording 0.48% in the latest quarter compared to 0.45% three months prior, reflecting variability in cost management relative to sales generated.

PE: -4.9x

Recently, Clear Channel Outdoor Holdings demonstrated insider confidence with significant share purchases, signaling a strong belief in the company's future despite its current challenges. This optimism coincides with their inclusion in several Russell indexes and a substantial shelf registration, suggesting readiness for strategic moves. Despite reporting a larger net loss this quarter compared to last year, they project an increase in revenue up to US$2.26 billion for the year. These developments could hint at potential underappreciated value within this market player.

Key Takeaways

- Reveal the 225 hidden gems among our Undervalued Small Caps With Insider Buying screener with a single click here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Clear Channel Outdoor Holdings is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CCO

Clear Channel Outdoor Holdings

Operates as an out-of-home advertising company in the United States, Europe, and internationally.

Undervalued with worrying balance sheet.