Advertisement

- United States

- /

- Media

- /

- NasdaqGS:SCHL

Here's Why Scholastic (NASDAQ:SCHL) Can Manage Its Debt Responsibly

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Scholastic Corporation (NASDAQ:SCHL) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Scholastic

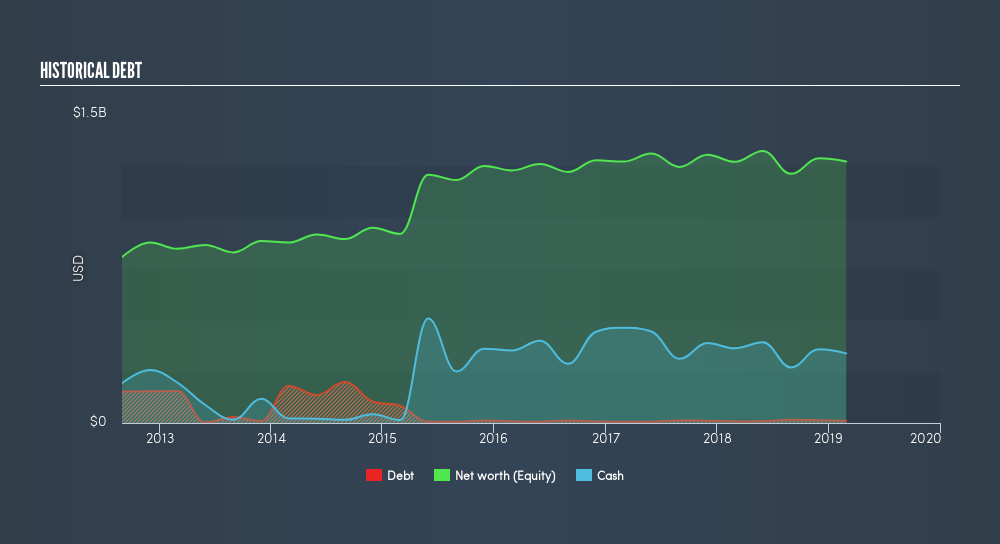

How Much Debt Does Scholastic Carry?

You can click the graphic below for the historical numbers, but it shows that as of February 2019 Scholastic had US$11.0m of debt, an increase on US$7.70m, over one year. But on the other hand it also has US$338.1m in cash, leading to a US$327.1m net cash position.

How Healthy Is Scholastic's Balance Sheet?

According to the last reported balance sheet, Scholastic had liabilities of US$696.1m due within 12 months, and liabilities of US$57.9m due beyond 12 months. Offsetting this, it had US$338.1m in cash and US$317.3m in receivables that were due within 12 months. So its liabilities total US$98.6m more than the combination of its cash and short-term receivables.

Since publicly traded Scholastic shares are worth a total of US$1.16b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Scholastic boasts net cash, so it's fair to say it does not have a heavy debt load!

Fortunately, Scholastic grew its EBIT by 8.0% in the last year, making that debt load look even more manageable. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Scholastic can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Scholastic has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Scholastic produced sturdy free cash flow equating to 56% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Scholastic has US$327m in net cash. So we don't think Scholastic's use of debt is risky. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Scholastic insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:SCHL

Scholastic

Scholastic Corporation, together with its subsidiaries, publishes and distributes children’s books in the United States and internationally.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor