Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:CARG

CarGurus (CARG) Surges on Strong Q3 Results and Dealer Expansion but What Fuels Its Growth Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

- CarGurus, Inc. recently reported its third-quarter 2025 earnings, revealing US$238.7 million in revenue and net income of US$44.72 million, both higher than the same period last year, along with optimistic guidance for the next quarter and full year.

- Strong international performance, increased dealer upgrades, and the launch of new AI-powered tools supported marketplace revenue growth and accelerated the company's addition of nearly 2,000 new paying dealers during the quarter.

- We'll examine how CarGurus' better-than-expected earnings and dealer growth impact its investment narrative and future prospects.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

CarGurus Investment Narrative Recap

To be a CarGurus shareholder, you need confidence in its ability to scale its core digital marketplace while maintaining strong dealer relationships, expanding internationally, and leveraging new technology. The Q3 2025 earnings beat and robust paying dealer growth directly support the most important near-term catalyst, wider dealer adoption of AI-powered tools and analytics, but do not materially reduce key competitive threats from large retailers and OEMs moving into the online car market.

Among recent announcements, the rollout of PriceVantage, CarGurus' AI-powered pricing tool, stands out as relevant. Its early success in improving inventory turnover showcases how product innovation is central to the company's growth story and to capturing more value from existing and new dealers, a vital factor given the increasingly competitive digital auto market.

In contrast, heightened competitive pressure from established auto retailers and new digital entrants could limit CarGurus’ ability to sustain margin expansion and...

Read the full narrative on CarGurus (it's free!)

CarGurus' narrative projects $1.1 billion revenue and $316.9 million earnings by 2028. This requires 5.7% yearly revenue growth and an earnings increase of $187.1 million from the current earnings of $129.8 million.

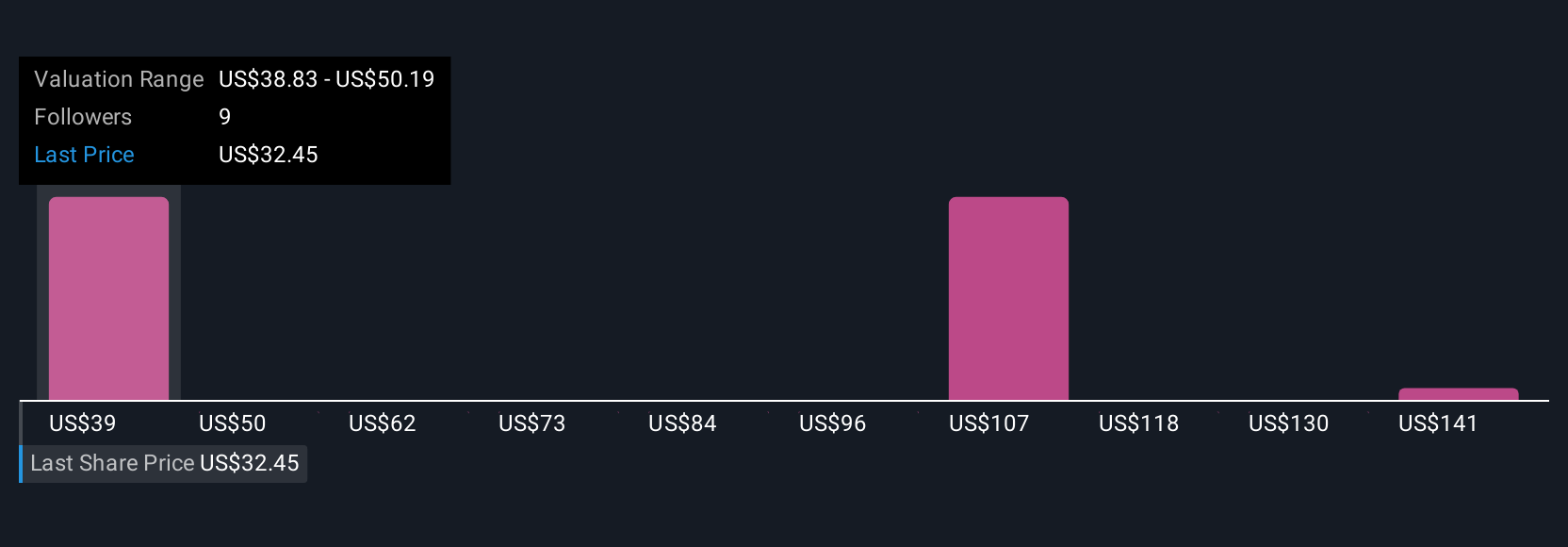

Uncover how CarGurus' forecasts yield a $39.75 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community range from US$39.75 up to US$152.39 per share. With marketplace revenue rising and competition intensifying, your outlook may shift as these diverse views reveal alternate expectations for CarGurus’ future performance.

Explore 6 other fair value estimates on CarGurus - why the stock might be worth over 4x more than the current price!

Build Your Own CarGurus Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CarGurus research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free CarGurus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CarGurus' overall financial health at a glance.

No Opportunity In CarGurus?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CARG

CarGurus

Operates an online automotive platform for buying and selling vehicles in the United States and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor