Advertisement

- United States

- /

- Chemicals

- /

- NasdaqGS:SOLS

Solstice Advanced Materials (SOLS): Exploring Valuation After Cramer Highlights Nuclear Opportunity and Industry Role

Simply Wall St

Reviewed by Simply Wall St

Solstice Advanced Materials (SOLS) has caught fresh attention after Jim Cramer highlighted its unique position as the sole American provider of uranium hexafluoride conversion services. This renewed spotlight raises questions about the company’s evolving role in the energy space.

See our latest analysis for Solstice Advanced Materials.

With Solstice Advanced Materials back in the spotlight thanks to industry recognition and its return to nuclear-related services, investors have noticed a recent shift in sentiment. The year-to-date share price return sits at -8.2%, reflecting earlier headwinds, but the renewed attention may be building fresh momentum for the long term.

If you're keeping an eye on standout materials and energy stocks, it's a great opportunity to see what else is on the move. Check out the full list with See the full list for free.

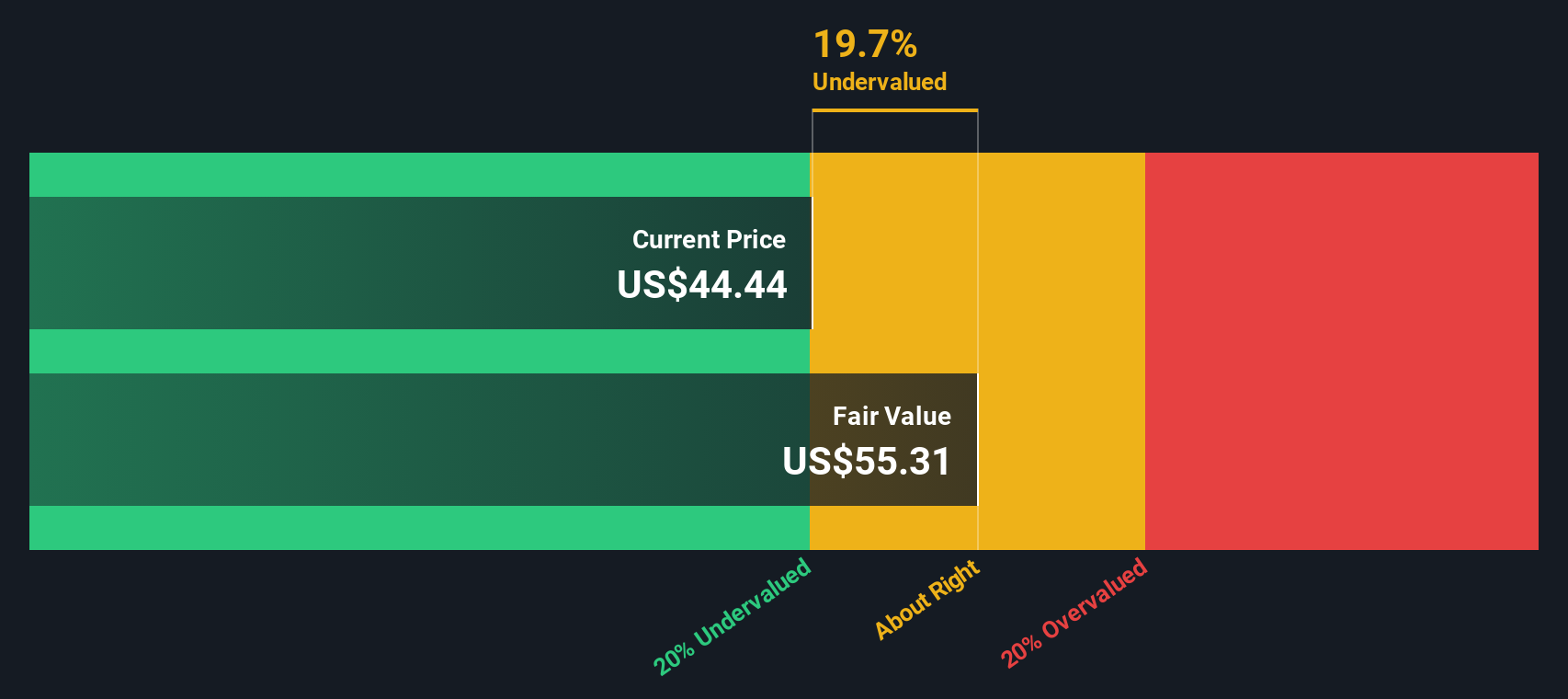

Yet with shares still trading at a nearly 20 percent discount to intrinsic value and well below analyst targets, the key question is whether this signals an undervalued entry point or if the market already anticipates future growth.

Price-to-Earnings of 21.4x: Is it justified?

Solstice Advanced Materials currently trades at a price-to-earnings (P/E) ratio of 21.4x, notably higher than the peer average of 16x. This suggests investors are pricing in a premium relative to similar companies within the sector.

The price-to-earnings ratio measures how much investors are willing to pay for each dollar of earnings. It is a widely watched valuation yardstick in the chemicals and materials space. A higher P/E ratio usually signals optimism about future profits, but it can also indicate that the stock is expensive relative to its earnings, unless future growth justifies the premium.

In the case of Solstice, its 21.4x P/E ratio stands out when compared to both its direct peers and the broader US Chemicals industry average, which is also 21.4x. While this could suggest the market expects substantial earnings growth or sees unique qualities in Solstice’s business, it puts pressure on the company to deliver improved financial performance in the quarters ahead.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 21.4x (OVERVALUED)

However, weaker-than-expected revenue growth or a delay in industry demand could quickly challenge bullish expectations for Solstice Advanced Materials in the short term.

Find out about the key risks to this Solstice Advanced Materials narrative.

Another View: The DCF Perspective

Looking through the lens of our DCF model offers a counterpoint. While the stock appears expensive based on its earnings multiple, the SWS DCF model suggests Solstice Advanced Materials is undervalued and trading about 19.8% below its estimated fair value. Does this model signal a hidden opportunity that the market is missing?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Solstice Advanced Materials for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 917 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Solstice Advanced Materials Narrative

If you see the story differently or want to dive deeper into the numbers yourself, it only takes a few minutes to craft your own outlook. Do it your way

A great starting point for your Solstice Advanced Materials research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

The smartest investors never settle for just one opportunity. Stay ahead of the curve by using these hand-picked screens from Simply Wall Street and put yourself in front of tomorrow’s winners.

- Capture steady returns when you target high-yield opportunities through these 17 dividend stocks with yields > 3%, offering reliable income in all market cycles.

- Outsmart the competition by spotting overlooked bargains using these 917 undervalued stocks based on cash flows, packed with potential growth stories trading below their real worth.

- Unlock the next wave of digital disruption by tapping into these 25 AI penny stocks, featuring companies applying artificial intelligence to transform entire industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SOLS

Solstice Advanced Materials

Operates as a specialty chemicals and advanced materials company in the United States and internationally.

Excellent balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor