Brown & Brown (BRO) has caught attention from investors following its recent stock performance. While the past month saw the share price drop around 8%, its longer-term record remains solid. The stock has gained 79% over five years.

Brown & Brown’s share price has cooled off so far this year, with momentum fading after a stretch of robust gains and a 12-month total shareholder return of -26%. However, its underlying long-term performance and earnings growth still set it apart from many competitors.

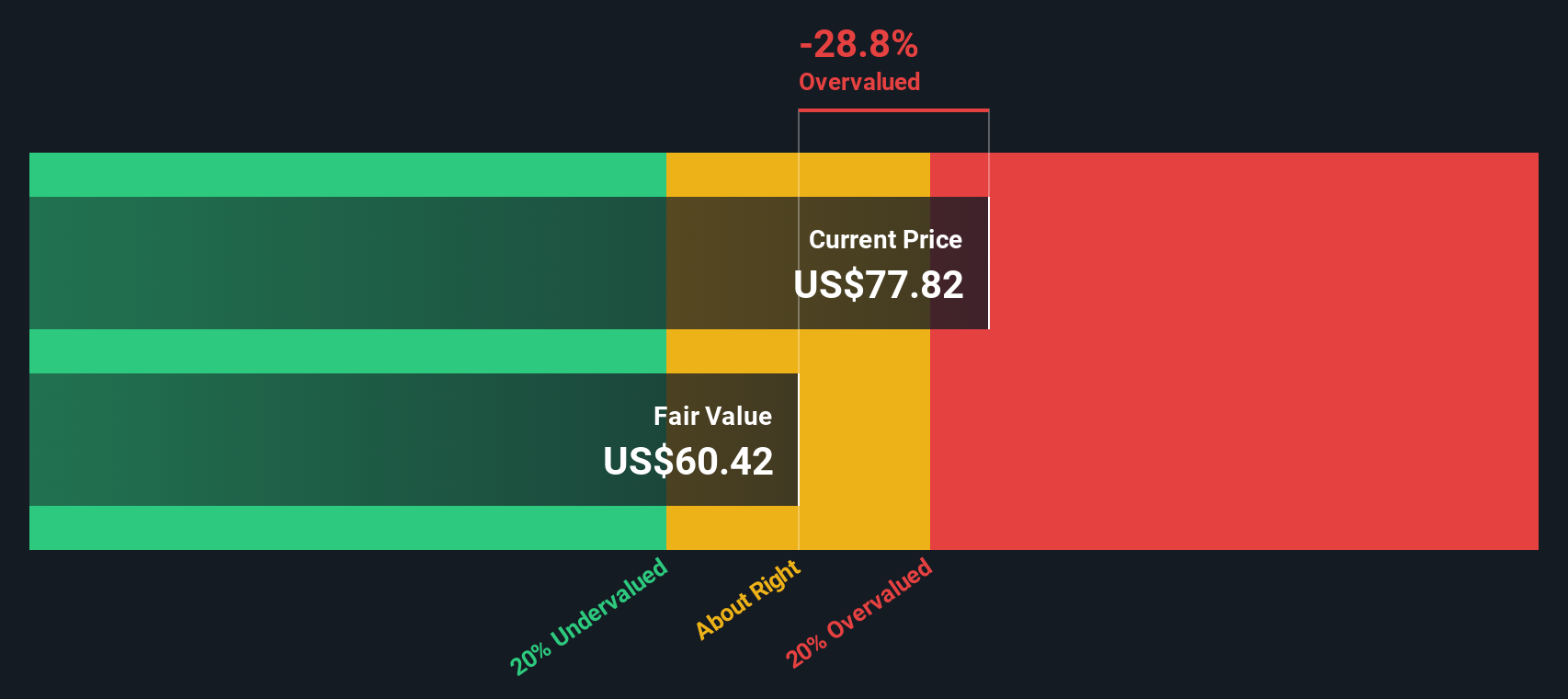

With the price now well below recent highs but long-term metrics still looking strong, should investors consider Brown & Brown undervalued at this stage, or has the market already accounted for its future growth potential?

Advertisement

Most Popular Narrative: 16.9% Undervalued

Brown & Brown’s fair value, as estimated in the widely followed narrative, sits well above the latest close. This comparison raises the stakes for what might drive future upside.

Brown & Brown's strategic focus on acquisitions, having completed 13 acquisitions with projected annual revenues of $36 million, could significantly enhance future revenue streams and market presence. This aligns with their goal of sustained revenue growth through expansion.

What is behind the math? The narrative’s price target is fueled by aggressive expansion bets, evolving margin forecasts, and some bold growth assumptions. Ready to dig into which levers analysts are pulling to justify this premium? The underlying model might surprise even the most seasoned investors.

However, unexpected shifts in insurance regulations or continued pressure on profit margins could quickly alter the outlook for Brown & Brown’s valuation.

While the narrative and consensus suggest Brown & Brown is undervalued, our SWS DCF model tells a different story. According to this method, Brown & Brown’s shares actually trade well above the current estimate of fair value. This could indicate that the market is already factoring in more future growth than is realistic.

If you would rather form your own conclusions or take a hands-on approach with the numbers, you can build a narrative from scratch in just a few minutes using our tools. Do it your way

A great starting point for your Brown & Brown research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Want More Ways to Grow Your Portfolio?

Think bigger with fresh opportunities. There is a world of top picks beyond Brown & Brown waiting to be found using the Simply Wall Street Screener. Don’t let the next market mover pass you by.

Tap into the next innovation wave by checking out these 27 AI penny stocks powering artificial intelligence, automation, and the future of tech sectors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Brown & Brown might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.