Advertisement

- United States

- /

- Insurance

- /

- NasdaqGS:WTW

Should Willis Towers Watson's (WTW) Climate Insurance Pilot in the Philippines Prompt Investor Action?

Simply Wall St

Reviewed by Sasha Jovanovic

- The Philippine Bureau of Fisheries and Aquatic Resources, together with partners including Rare and Willis Towers Watson, recently announced the launch of the country's first parametric insurance pilot for 14,200 small-scale fishers, providing timely compensation for lost income during extreme weather.

- This initiative highlights WTW's expanding role in climate risk solutions and underscores the growing demand for insurance products that support social and environmental resilience in emerging markets.

- We'll examine how introducing climate-focused insurance in the Philippines may shape WTW's investment appeal through innovation-driven growth opportunities.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Willis Towers Watson Investment Narrative Recap

To be a shareholder in Willis Towers Watson, you must believe in the company's ability to adapt its consulting, broking, and risk management services to changing markets and technology. The recent launch of climate-focused parametric insurance in the Philippines shows WTW's commitment to innovation and resilience solutions, though this initiative is unlikely to move the needle on its most immediate growth catalyst: accelerating demand for advanced risk consulting. The main near-term risk remains margin compression from competition and digital automation, with the pilot not materially affecting this.

Relevant to the climate risk partnership is WTW's recent executive appointment in Asia, naming Anthony Wong as head of Casualty. Building experienced leadership in the region aligns with the company’s push for specialized, higher-margin business lines and may support momentum in areas like climate-linked risk products.

However, investors should be mindful that, despite these growth efforts, competitive pressures from peers and digital disruption could still threaten...

Read the full narrative on Willis Towers Watson (it's free!)

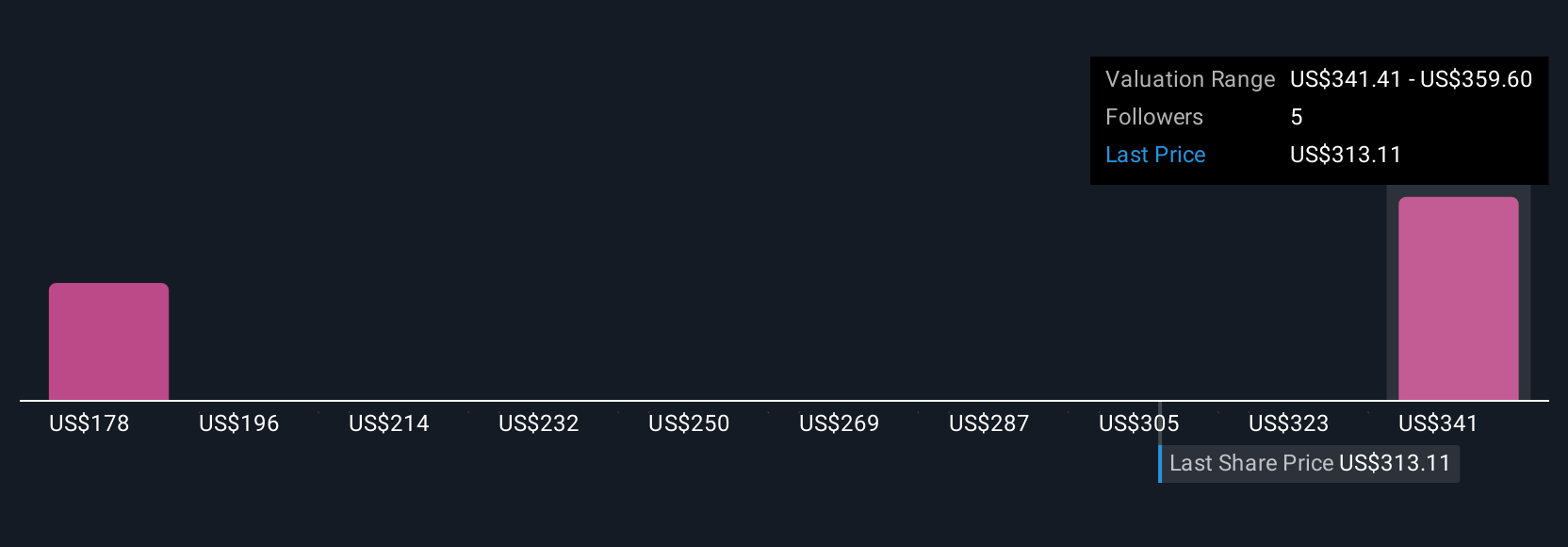

Willis Towers Watson's narrative projects $10.9 billion revenue and $2.5 billion earnings by 2028. This requires 3.7% yearly revenue growth and a $2.4 billion increase in earnings from $137.0 million today.

Uncover how Willis Towers Watson's forecasts yield a $371.61 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Fair value estimates from the Simply Wall St Community range from US$371.61 to US$392.29, based on two perspectives. While many see revenue growth in specialized segments as a driver, margin pressure from digital competitors also weighs on future performance, so it pays to review alternate forecasts.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth just $371.61!

Build Your Own Willis Towers Watson Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Willis Towers Watson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WTW

Willis Towers Watson

Operates as an advisory, broking, and solutions company worldwide.

Adequate balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|3.6% undervalued

TI

Community Contributor

Recently Updated Narratives

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8148.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.0% undervalued

22 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BI

BinocularMan on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.3% undervalued

128 followersusers have followed this narrative

5 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

79 followersusers have followed this narrative

10 commentsusers have commented on this narrative

16 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7921.6% undervalued

915 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative