Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Enzo Biochem, Inc. (NYSE:ENZ) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Enzo Biochem

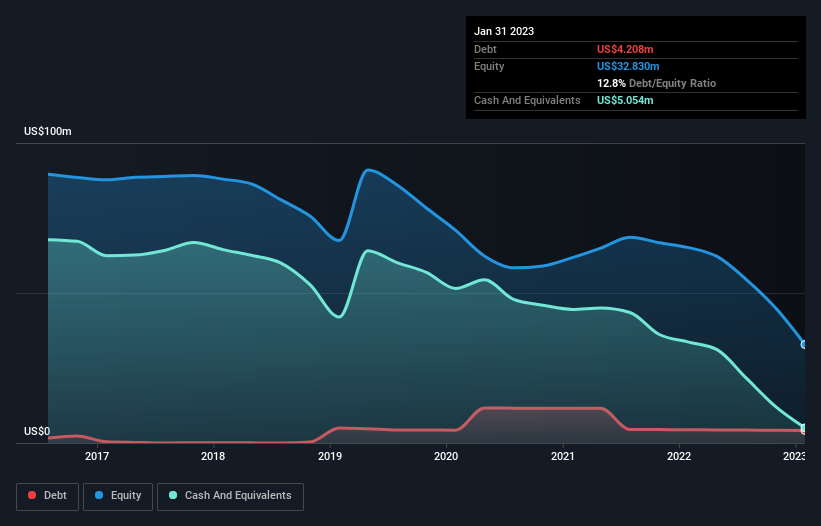

What Is Enzo Biochem's Debt?

You can click the graphic below for the historical numbers, but it shows that Enzo Biochem had US$4.21m of debt in January 2023, down from US$4.43m, one year before. However, it does have US$5.05m in cash offsetting this, leading to net cash of US$846.0k.

How Healthy Is Enzo Biochem's Balance Sheet?

The latest balance sheet data shows that Enzo Biochem had liabilities of US$32.2m due within a year, and liabilities of US$11.4m falling due after that. Offsetting these obligations, it had cash of US$5.05m as well as receivables valued at US$10.9m due within 12 months. So its liabilities total US$27.7m more than the combination of its cash and short-term receivables.

Enzo Biochem has a market capitalization of US$114.7m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. While it does have liabilities worth noting, Enzo Biochem also has more cash than debt, so we're pretty confident it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Enzo Biochem will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Enzo Biochem had a loss before interest and tax, and actually shrunk its revenue by 31%, to US$81m. To be frank that doesn't bode well.

So How Risky Is Enzo Biochem?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that Enzo Biochem had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$28m and booked a US$35m accounting loss. While this does make the company a bit risky, it's important to remember it has net cash of US$846.0k. That means it could keep spending at its current rate for more than two years. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 3 warning signs for Enzo Biochem you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Enzo Biochem might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:ENZB

Enzo Biochem

A life sciences company, engages in the labeling and detection technologies from DNA to whole cell analysis in the United States and internationally.

Flawless balance sheet unattractive dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor