- United States

- /

- Medical Equipment

- /

- NasdaqCM:RMTI

Some Rockwell Medical, Inc. (NASDAQ:RMTI) Analysts Just Made A Major Cut To Next Year's Estimates

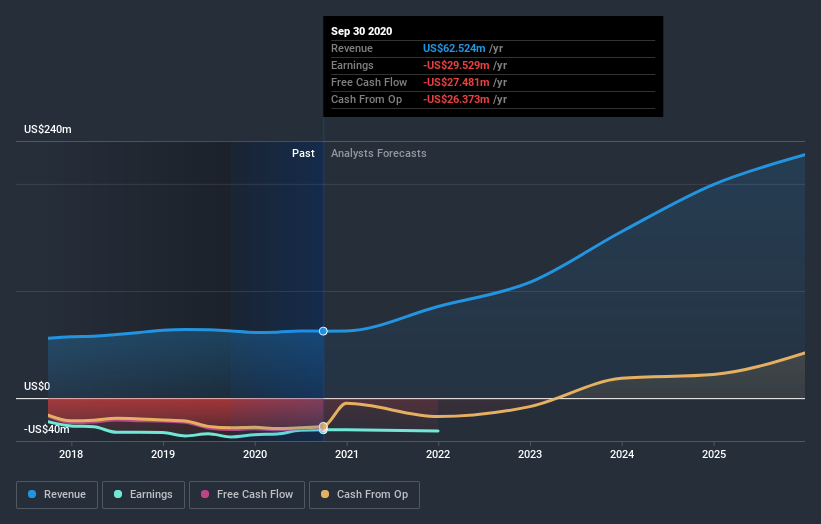

The analysts covering Rockwell Medical, Inc. (NASDAQ:RMTI) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for next year. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analysts have soured majorly on the business. Investors however, have been notably more optimistic about Rockwell Medical recently, with the stock price up a whopping 56% to US$1.93 in the past week. It will be interesting to see if the downgrade has an impact on buying demand for the company's shares.

Following the downgrade, the current consensus from Rockwell Medical's dual analysts is for revenues of US$86m in 2021 which - if met - would reflect a substantial 37% increase on its sales over the past 12 months. Losses are predicted to fall substantially, shrinking 32% to US$0.29. However, before this estimates update, the consensus had been expecting revenues of US$110m and US$0.19 per share in losses. Ergo, there's been a clear change in sentiment, with the analysts administering a notable cut to next year's revenue estimates, while at the same time increasing their loss per share forecasts.

See our latest analysis for Rockwell Medical

The consensus price target fell 25% to US$5.25, implicitly signalling that lower earnings per share are a leading indicator for Rockwell Medical's valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Rockwell Medical at US$5.50 per share, while the most bearish prices it at US$5.00. This is a very narrow spread of estimates, implying either that Rockwell Medical is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The analysts are definitely expecting Rockwell Medical's growth to accelerate, with the forecast 37% growth ranking favourably alongside historical growth of 3.6% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 9.0% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that Rockwell Medical is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that analysts increased their loss per share estimates for next year. While analysts did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

That said, the analysts might have good reason to be negative on Rockwell Medical, given recent substantial insider selling. For more information, you can click here to discover this and the 4 other risks we've identified.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

When trading Rockwell Medical or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:RMTI

Rockwell Medical

Operates as a healthcare company that engages in the development, manufacture, commercialization, and distribution of various hemodialysis products for dialysis providers worldwide.

Excellent balance sheet with reasonable growth potential.