Advertisement

- United States

- /

- Healthcare Services

- /

- NasdaqGS:PRVA

A Fresh Look at Privia Health Group (PRVA) Valuation Following Raised 2025 Revenue Guidance and Strong Q3 Results

Simply Wall St

Reviewed by Simply Wall St

Privia Health Group (PRVA) just released its third-quarter earnings, showing strong year-over-year growth in both revenue and profits. The company also raised its revenue outlook for the full year, signaling confidence in ongoing performance.

See our latest analysis for Privia Health Group.

Following the upbeat earnings report and raised revenue guidance, Privia Health Group’s 16.5% share price return over the last 90 days stands out, even as the 1-year total shareholder return sits at 6.4%. While momentum is building in the short term, the longer view still reflects some recovery from earlier challenges.

Interested in healthcare stocks benefiting from renewed growth trends? Discover fresh opportunities in the sector with our curated picks. See the full list here: See the full list for free.

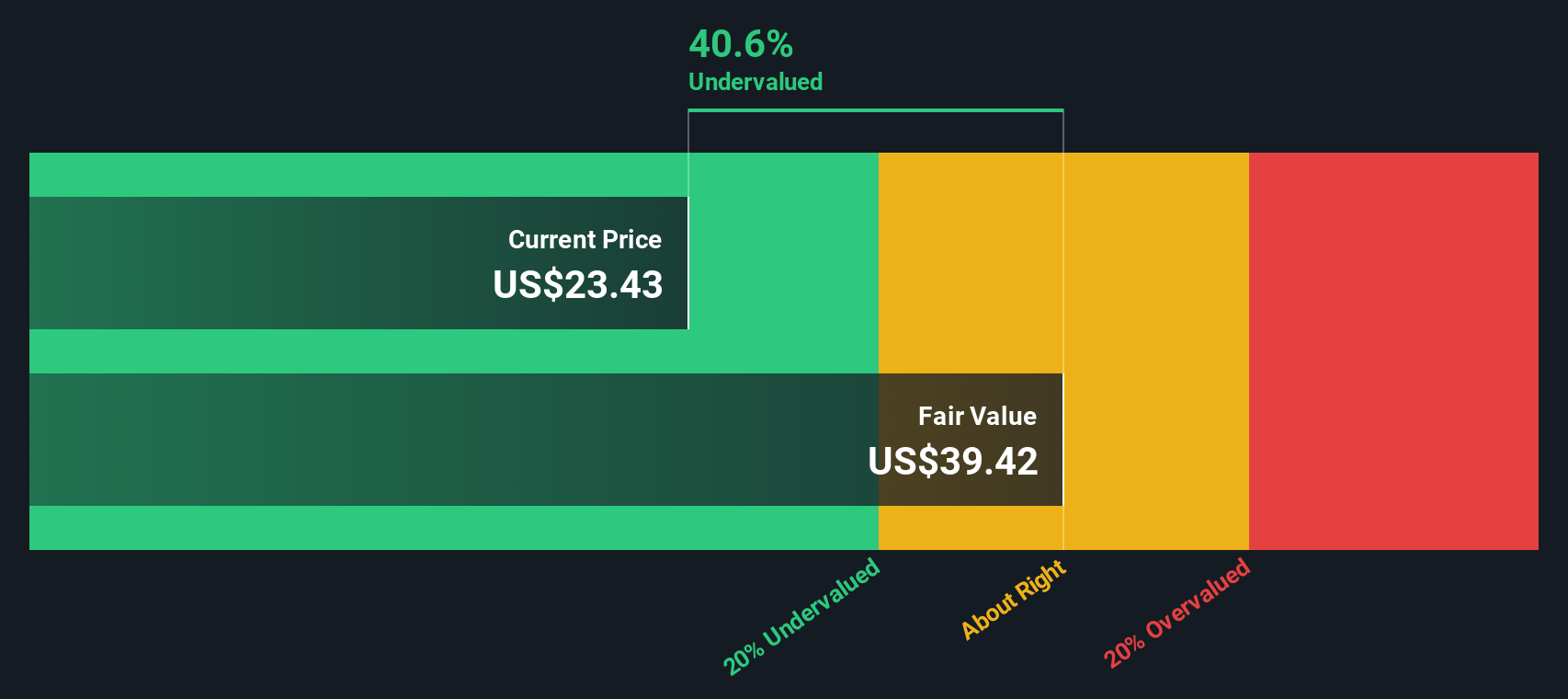

With the stock now trading well below most analyst price targets and showing impressive growth rates, investors must ask themselves if Privia Health Group is still undervalued or if the market has already priced in these strong results.

Most Popular Narrative: 20.5% Undervalued

At $23.98, Privia Health Group’s last close sits well below the narrative consensus fair value of $30.15. The narrative points to meaningful upside if the company delivers on its projected earnings and margin growth.

Demographic tailwinds from the growing and aging U.S. population are driving sustained increases in patient volumes across Privia's network. This supports strong top-line revenue growth and predictable, recurring fee streams for the company's technology and services platform. The industry trend toward value-based care, along with related shared savings and care management fees, is enabling Privia to grow its value-based attributed lives at a double-digit rate and to expand margins as risk-sharing agreements mature. This, in turn, positively impacts earnings and long-term EBITDA growth.

Want to see what’s behind this bullish narrative? The fair value hinges on aggressive profit margin expansion and bigger recurring revenue, but there’s even more factored into those projections. Curious if these assumptions truly stack up? Find out what the narrative says is fueling that premium price target.

Result: Fair Value of $30.15 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, growing consolidation among insurers and rising healthcare labor costs could put pressure on Privia Health Group’s margins and challenge its long-term profitability narrative.

Find out about the key risks to this Privia Health Group narrative.

Another View: DCF Model Signals Even Greater Upside

While consensus analyst targets suggest Privia Health Group has room to run, our DCF model paints an even brighter picture, estimating fair value at $39.51. This is nearly 39% above the current share price. Could this deeper discount in the DCF hint at even more untapped opportunity, or does it overstate long-term growth?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Privia Health Group Narrative

If you want to challenge these assumptions or build your own case around the numbers, you can create a custom narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Privia Health Group.

Looking for more investment ideas?

Smart investors never settle for just one opportunity. Unlock your next great move by using Simply Wall Street’s powerful screener, which spots hidden gems and untapped growth stories you don’t want to miss out on.

- Access the latest market disruptors and cutting-edge artificial intelligence by checking out these 25 AI penny stocks poised for explosive growth.

- Secure consistent returns with these 17 dividend stocks with yields > 3% that offer yields above 3 percent and stand out for their strong income potential.

- Capitalize on value plays with these 849 undervalued stocks based on cash flows designed to spotlight stocks trading below their fair value based on future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PRVA

Privia Health Group

Operates as a national physician-enablement company in the United States.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor