Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:OMCL

How Investors May Respond To Omnicell (OMCL) Eyes on Return to Revenue Growth and Margin Prospects

Simply Wall St

Reviewed by Sasha Jovanovic

- Omnicell recently announced it will report earnings, with analysts expecting revenue to return to growth after last year's decline.

- An interesting detail is that Omnicell has exceeded revenue expectations for eight consecutive quarters, often surpassing analyst estimates.

- We'll explore how anticipation of renewed revenue growth influences Omnicell's investment case and margin outlook.

Find companies with promising cash flow potential yet trading below their fair value.

Omnicell Investment Narrative Recap

To own Omnicell shares, an investor needs to believe that healthcare automation will drive sustained demand for Omnicell’s medication management solutions, enabling a return to consistent revenue growth and stronger margins, even in the face of sector volatility. The recent news confirming analyst expectations for renewed revenue growth is a positive for the stock’s short-term outlook, with revenue performance remaining the most important near-term catalyst. Margin pressures from tariffs and supply chain costs are still key risks, and the news does not materially change these factors.

Among Omnicell’s latest initiatives, the launch of the Central Med Automation Service stands out, expanding the company’s subscription-based value proposition for health systems. This is closely tied to the catalyst of driving higher-margin recurring revenue, and aligns with the market’s focus on predictability as automation adoption increases.

However, while progress is visible, investors should be aware that, in contrast to expectations for revenue recovery, ongoing tariff impacts could still weigh on margins and long-term earnings...

Read the full narrative on Omnicell (it's free!)

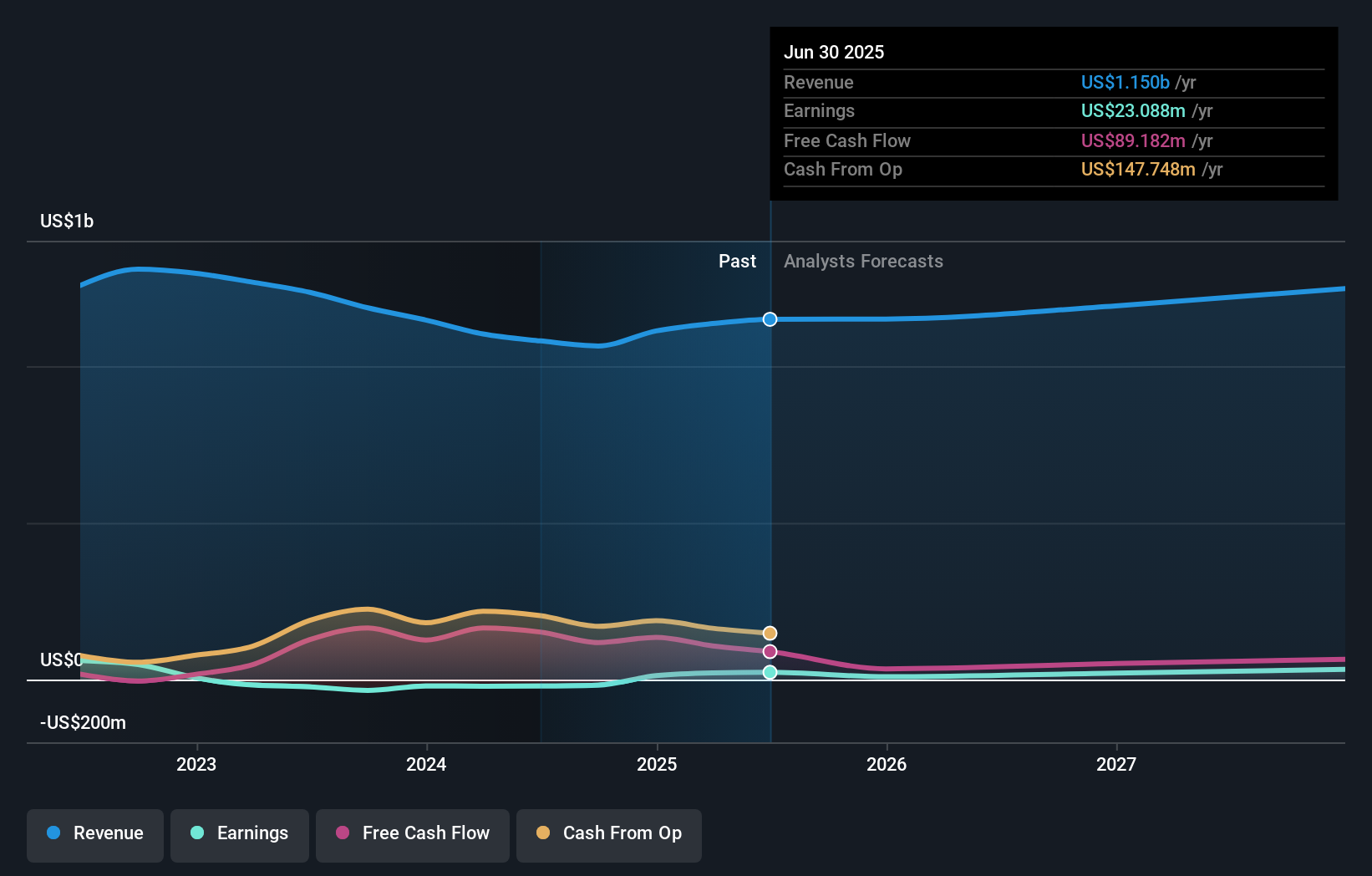

Omnicell's outlook anticipates $1.3 billion in revenue and $30.4 million in earnings by 2028. This scenario is based on a 3.0% annual revenue growth rate and a $7.3 million increase in earnings from the current $23.1 million.

Uncover how Omnicell's forecasts yield a $44.00 fair value, a 47% upside to its current price.

Exploring Other Perspectives

Only one member of the Simply Wall St Community gave a fair value estimate for Omnicell, setting it at US$44. Recent attention to recurring revenue growth has focused the market, but margin risk from tariffs remains in view. See how your view compares to others in the Community.

Explore another fair value estimate on Omnicell - why the stock might be worth just $44.00!

Build Your Own Omnicell Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Omnicell research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Omnicell research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Omnicell's overall financial health at a glance.

Curious About Other Options?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:OMCL

Omnicell

Provides medication management solutions and adherence tools for healthcare systems and pharmacies the United States and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor