Advertisement

- United States

- /

- Healthcare Services

- /

- NasdaqGS:ENSG

The Bull Case For Ensign Group (ENSG) Could Change Following Raised Outlook and New Facility Acquisitions

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 3, 2025, The Ensign Group announced raised earnings and revenue guidance for 2025, posted solid third quarter results with year-over-year growth in revenue and net income, and revealed several new skilled nursing facility acquisitions.

- The simultaneous increase in guidance and expansion through multiple facility acquisitions highlights the company's focus on scaling operations and integrating recent growth.

- We'll examine how Ensign Group's updated profit outlook and expanding facility portfolio shape its broader investment narrative.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

What Is Ensign Group's Investment Narrative?

For anyone looking at Ensign Group, the core investment case centers on its ability to scale while maintaining quality and improving profitability in a competitive healthcare market. The company’s just-released results and raised 2025 guidance signal intent: management is pushing for growth through fresh acquisitions and higher top-line expectations. Not only did Ensign deliver solid quarterly figures, but the latest acquisitions in Utah and Alabama add fresh facilities and revenue streams, potentially strengthening its near-term catalysts. This expansion provides some support to growth forecasts, reducing concerns about organic growth plateauing in the short term. Still, the biggest risks, such as its relatively high valuation, modest return on equity, and the challenges of integrating new facilities, remain relevant. The news may help reduce uncertainty on execution risk, but it also puts pressure on the company to prove these moves will boost margins and justify Ensign’s premium multiples. On the other hand, Ensign’s high price-to-earnings ratio is higher than much of the sector, something investors should keep in mind.

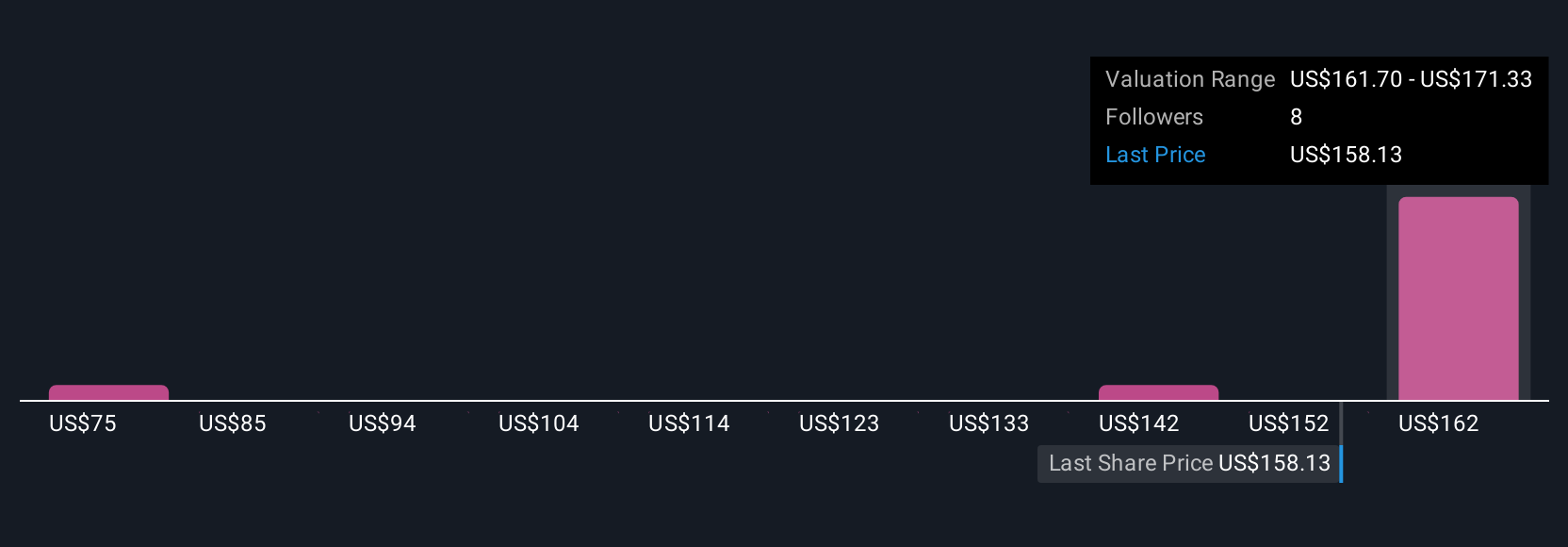

Ensign Group's share price has been on the slide but might be up to 11% below fair value. Find out if it's a bargain.Exploring Other Perspectives

Explore 4 other fair value estimates on Ensign Group - why the stock might be worth less than half the current price!

Build Your Own Ensign Group Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Ensign Group research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Ensign Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ensign Group's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Outshine the giants: these 27 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Ensign Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ENSG

Ensign Group

Provides skilled nursing, senior living, and rehabilitative services.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor