Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:EMBC

Embecta Corp. Just Beat EPS By 79%: Here's What Analysts Think Will Happen Next

Investors in Embecta Corp. (NASDAQ:EMBC) had a good week, as its shares rose 3.1% to close at US$14.82 following the release of its quarterly results. It looks like a credible result overall - although revenues of US$273m were what the analysts expected, Embecta surprised by delivering a (statutory) profit of US$0.25 per share, an impressive 79% above what was forecast. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for Embecta

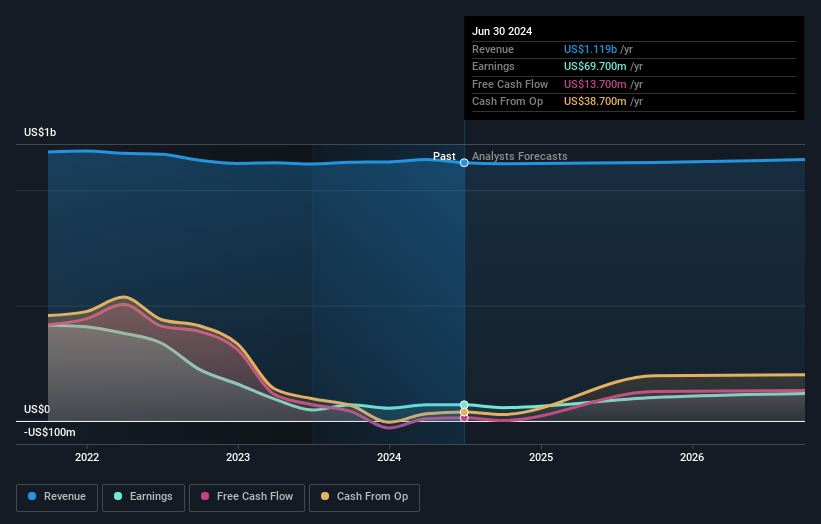

Following last week's earnings report, Embecta's six analysts are forecasting 2025 revenues to be US$1.12b, approximately in line with the last 12 months. Per-share earnings are expected to soar 42% to US$1.71. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$1.12b and earnings per share (EPS) of US$1.69 in 2025. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

The consensus price target rose 7.1% to US$16.07despite there being no meaningful change to earnings estimates. It could be that the analystsare reflecting the predictability of Embecta's earnings by assigning a price premium. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Embecta, with the most bullish analyst valuing it at US$18.20 and the most bearish at US$13.00 per share. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The period to the end of 2025 brings more of the same, according to the analysts, with revenue forecast to display 0.04% growth on an annualised basis. That is in line with its 0.04% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 8.1% per year. So it's pretty clear that Embecta is expected to grow slower than similar companies in the same industry.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have forecasts for Embecta going out to 2026, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 4 warning signs for Embecta (2 shouldn't be ignored) you should be aware of.

Valuation is complex, but we're here to simplify it.

Discover if Embecta might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:EMBC

Embecta

A medical device company, focuses on the provision of various solutions to enhance the health and wellbeing of people living with diabetes in the United States and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor