Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGM:ATRC

Health Check: How Prudently Does AtriCure (NASDAQ:ATRC) Use Debt?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, AtriCure, Inc. (NASDAQ:ATRC) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for AtriCure

What Is AtriCure's Debt?

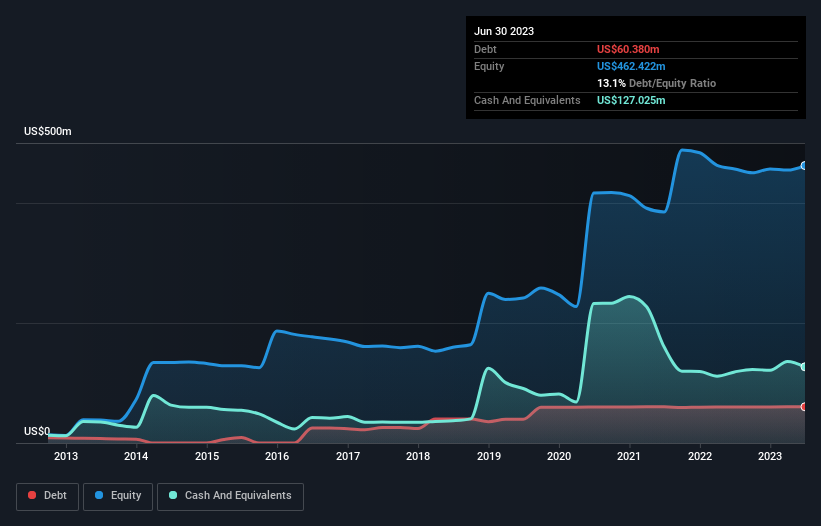

As you can see below, AtriCure had US$60.4m of debt, at June 2023, which is about the same as the year before. You can click the chart for greater detail. But it also has US$127.0m in cash to offset that, meaning it has US$66.6m net cash.

A Look At AtriCure's Liabilities

Zooming in on the latest balance sheet data, we can see that AtriCure had liabilities of US$71.4m due within 12 months and liabilities of US$60.3m due beyond that. Offsetting these obligations, it had cash of US$127.0m as well as receivables valued at US$48.4m due within 12 months. So it actually has US$43.6m more liquid assets than total liabilities.

Having regard to AtriCure's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the US$2.66b company is struggling for cash, we still think it's worth monitoring its balance sheet. Simply put, the fact that AtriCure has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine AtriCure's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, AtriCure reported revenue of US$366m, which is a gain of 21%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

So How Risky Is AtriCure?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year AtriCure had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of US$48m and booked a US$28m accounting loss. However, it has net cash of US$66.6m, so it has a bit of time before it will need more capital. AtriCure's revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. By investing before those profits, shareholders take on more risk in the hope of bigger rewards. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that AtriCure is showing 4 warning signs in our investment analysis , and 1 of those shouldn't be ignored...

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:ATRC

AtriCure

Develops, manufactures, and sells devices for surgical ablation of cardiac tissue, exclusion of the left atrial appendage, and temporarily blocking pain by ablating peripheral nerves to medical centers in the United States, the Asia-Pacific, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor