Advertisement

- United States

- /

- Food

- /

- NYSE:POST

How JPMorgan's Focus on Foodservice Potential Could Shift Post Holdings (POST) Investment Narrative

Simply Wall St

Reviewed by Sasha Jovanovic

- Post Holdings recently reached its 52-week low following JPMorgan's initiation of coverage with an Overweight rating, where the firm highlighted strong performance in the Foodservice division despite soft expectations for most other segments.

- Management's continued share buybacks and the company's strong liquidity position appear to be reassuring factors for investors amid ongoing operational challenges.

- We'll explore how the focus on Foodservice potential by a major financial institution could impact Post Holdings' overall investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Post Holdings Investment Narrative Recap

To have confidence as a Post Holdings shareholder, I believe you need to accept near-term volatility in exchange for the company's ability to defend market share and drive margin expansion, particularly through its Foodservice segment. The recent Overweight rating from JPMorgan, highlighting Foodservice growth despite segment softness, may provide a short-term sentiment boost, but does not materially change the biggest catalyst, operational execution in Foodservice, or the largest risk, which remains shrinking volumes in core cereal and pet food categories. Among the company’s recent moves, the ongoing $500 million share buyback stands out as most relevant to current events. Management’s active repurchases reinforce liquidity and signal confidence during periods of uncertainty, offering some buffer to investor sentiment while the business contends with mixed segment performance and market headwinds. Yet, despite these constructive signals, it’s important to recognize that volume declines in key brands could pressure...

Read the full narrative on Post Holdings (it's free!)

Post Holdings' narrative projects $9.2 billion revenue and $537.3 million earnings by 2028. This requires 5.2% yearly revenue growth and a $171 million earnings increase from $366.3 million today.

Uncover how Post Holdings' forecasts yield a $127.44 fair value, a 21% upside to its current price.

Exploring Other Perspectives

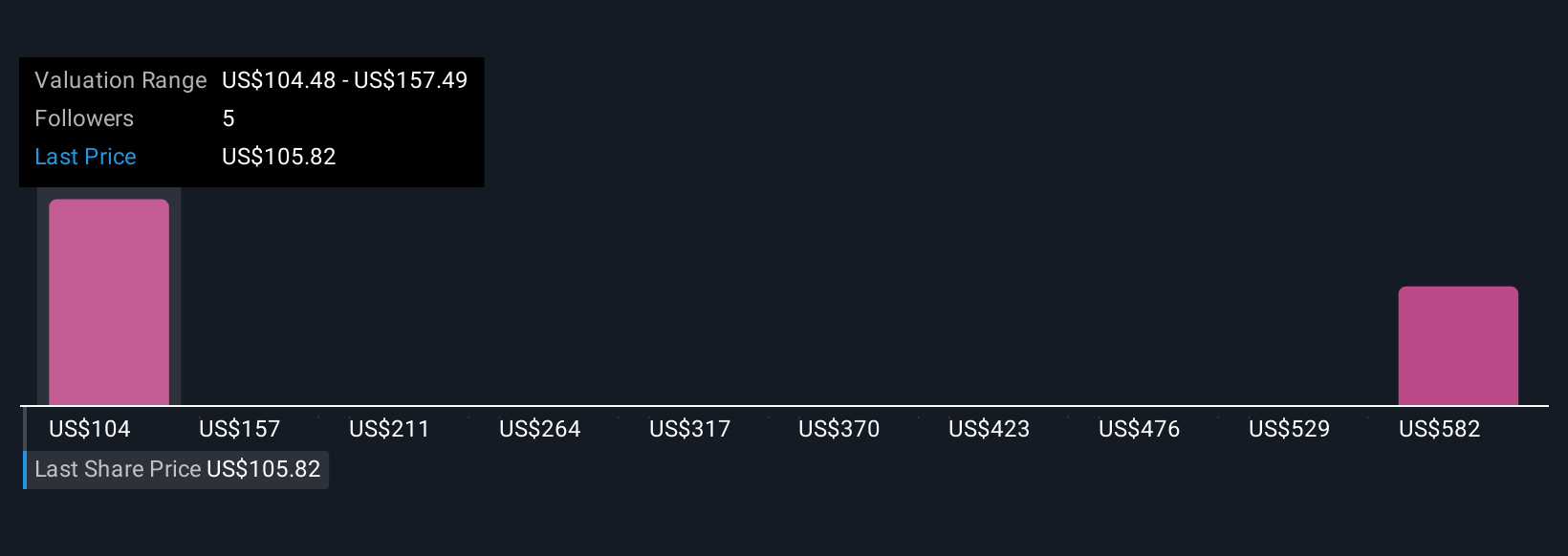

Four perspectives from the Simply Wall St Community put Post Holdings’ fair value anywhere from US$104.48 to US$549.94. While you weigh this broad spread, remember that continued category volume declines could challenge long-term earnings strength, take a look at how others interpret the risks and opportunities surrounding Post Holdings.

Explore 4 other fair value estimates on Post Holdings - why the stock might be worth over 5x more than the current price!

Build Your Own Post Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Post Holdings research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Post Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Post Holdings' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:POST

Post Holdings

Operates as a consumer packaged goods holding company in the United States and internationally.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.6% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.0% undervalued

DA

Community Contributor