Advertisement

- United States

- /

- Food

- /

- NYSE:GIS

Does General Mills’ Product Line Expansion Signal an Attractive Entry as Shares Drop 23.9% in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if General Mills is a bargain right now? Let's dig into whether the stock's current price is as attractive as it seems.

- The stock climbed 1.9% over the past week, but is still down 23.9% year-to-date. This hints at shifting sentiment and possible opportunities ahead.

- Recent headlines have focused on General Mills' evolving product line and steady consumer demand as the company expands its health-conscious offerings and invests in key brands. These moves are shaping broader investor conversations around its long-term resilience.

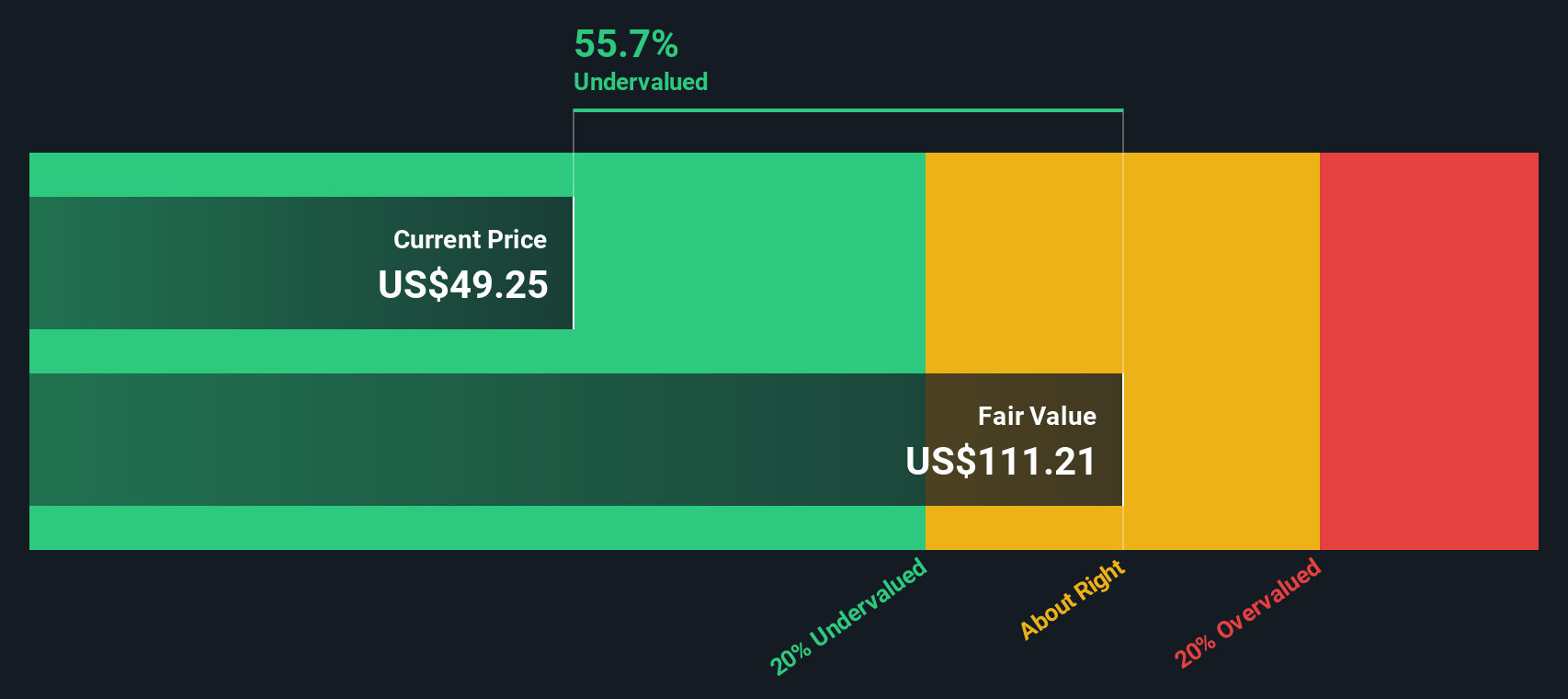

- Based on our valuation checks, General Mills scores 5 out of 6 for being undervalued, a strong showing for this market backdrop. We'll break down the standard valuation methods in a moment, and there will be an even more insightful approach to understanding the real value of General Mills at the end of this article.

Find out why General Mills's -22.2% return over the last year is lagging behind its peers.

Approach 1: General Mills Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates the value of a company by forecasting its future cash flows and discounting them back to today's dollars. This approach captures both the company's near-term financial performance and its long-term growth prospects.

For General Mills, the most recent Free Cash Flow stands at $2.01 billion. Analysts provide cash flow projections for up to five years, with Simply Wall St's model extrapolating further estimates through 2035. Over the next ten years, forecasts suggest that General Mills' cash flows will grow to approximately $2.29 billion by 2029. Each year's future cash flows are discounted back to present value, reflecting both the time value of money and uncertainties in distant forecasts.

Based on these calculations, the DCF model arrives at an estimated intrinsic value of $103.97 per share. This figure is notably higher than the current market price, indicating that General Mills stock is trading at a 53.5% discount to its intrinsic value.

In summary, the DCF approach suggests General Mills is significantly undervalued compared to its projected long-term cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests General Mills is undervalued by 53.5%. Track this in your watchlist or portfolio, or discover 917 more undervalued stocks based on cash flows.

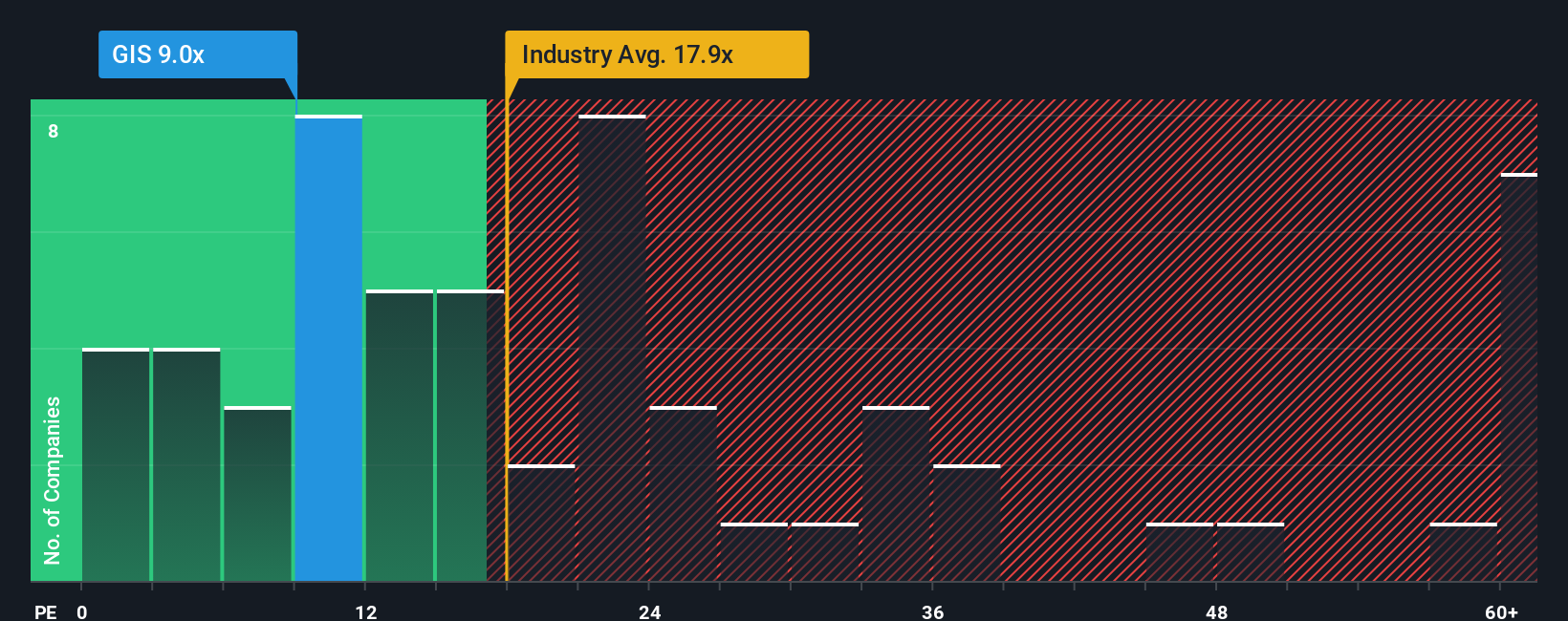

Approach 2: General Mills Price vs Earnings

For companies with steady profits like General Mills, the Price-to-Earnings (PE) ratio is a practical tool for valuation. The PE ratio helps investors assess what they are paying for each dollar of a company's earnings, making it especially useful for mature, profitable businesses.

A company's "normal" or "fair" PE ratio reflects both its growth outlook and risk levels. Higher growth expectations often justify a higher PE, while more uncertainty or sector-specific risks may warrant a discount compared to the market.

Currently, General Mills is trading at a PE of 8.86x. This is considerably lower than the Food industry average of 19.45x and also lags behind the peer group, which averages 28.49x. These comparisons suggest the market is taking a conservative view on General Mills relative to its sector.

However, rather than relying solely on these broad benchmarks, Simply Wall St’s “Fair Ratio” offers a more tailored perspective. This proprietary metric blends factors like earnings growth, profitability, risk, industry characteristics and market capitalization to estimate the PE ratio that truly reflects General Mills’ unique position and prospects. By factoring in these company-specific drivers, the Fair Ratio provides a more meaningful yardstick than a blanket industry or peer average.

In General Mills’ case, the Fair Ratio is set at 11.48x. Since this is just moderately above the current PE of 8.86x, it indicates the stock is meaningfully undervalued, even when considering the risks and growth profile captured by the custom Fair Ratio.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1422 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your General Mills Narrative

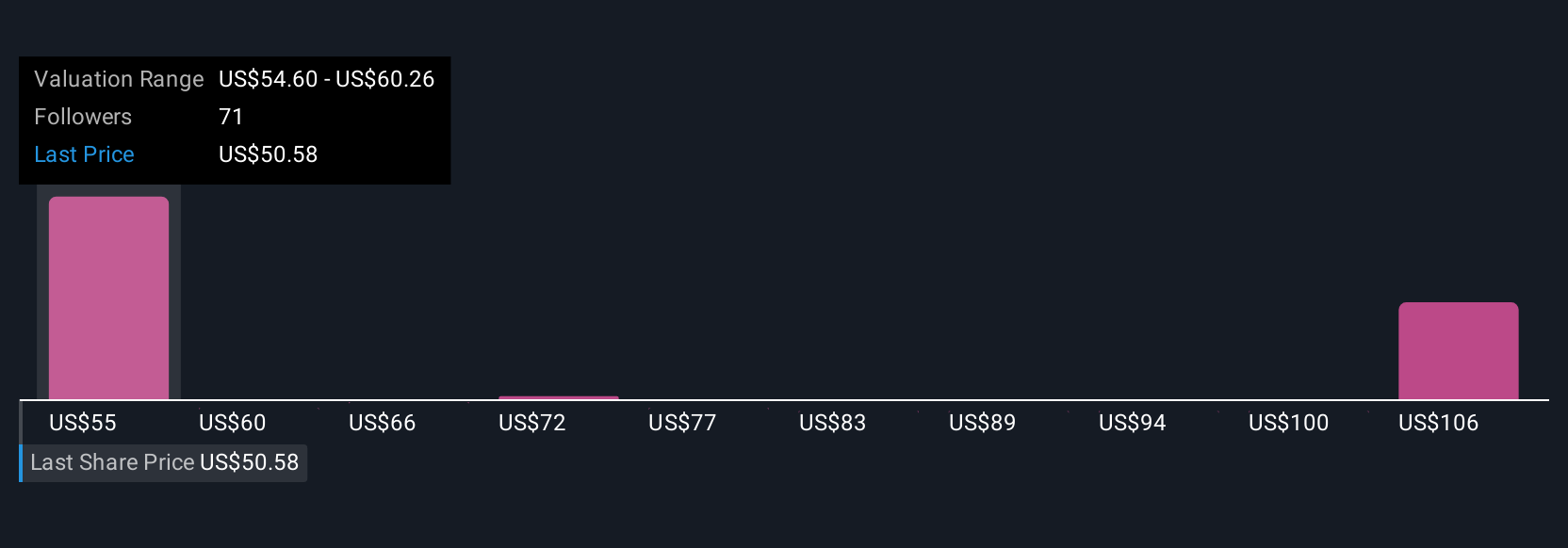

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal story or perspective about a company, connecting what you believe about its future with financial forecasts and estimated fair value. Instead of just focusing on ratios or analyst price targets, Narratives allow you to tie together the company’s strategy, expected growth, risks and industry dynamics in one place, creating a financial outcome that truly reflects your outlook.

On Simply Wall St's Community page, millions of investors use Narratives to share exactly how news, products, management moves or market trends shape their own forecasts for revenue, earnings and margins. Narratives help you decide when to buy or sell by directly comparing your fair value to the current market price, and they automatically update as new information or earnings are announced. This way, your views remain fresh and actionable.

For instance, one investor might believe General Mills’ aggressive reinvestment and innovation will drive profit recovery and set a fair value of $63.00 per share. Another, more cautious Narrative might focus on margin headwinds or potential business closures, resulting in a bearish valuation of $45.00 per share.

Do you think there's more to the story for General Mills? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GIS

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor