Stock Analysis

- United States

- /

- Food

- /

- NasdaqGS:FARM

Farmer Bros (NASDAQ:FARM) Has Debt But No Earnings; Should You Worry?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Farmer Bros. Co. (NASDAQ:FARM) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Farmer Bros

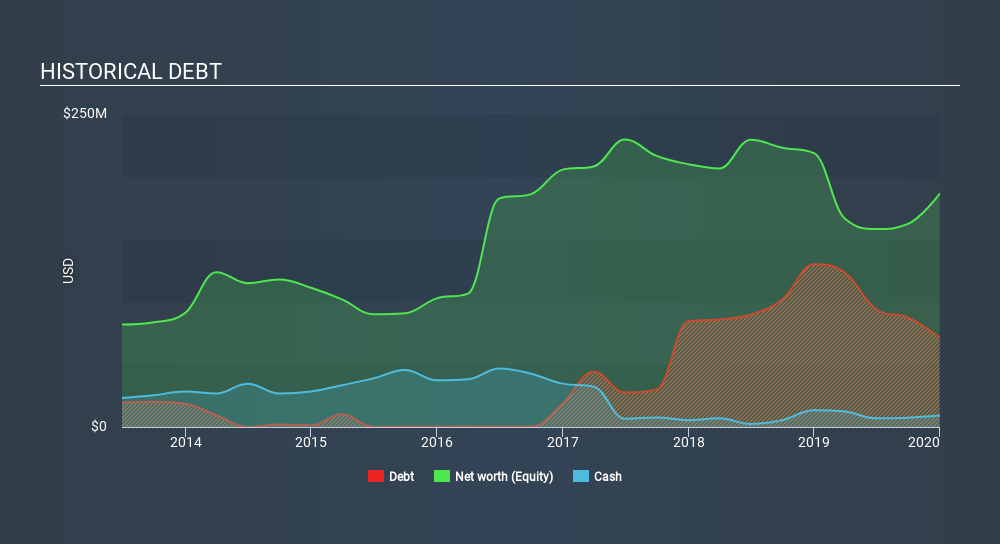

How Much Debt Does Farmer Bros Carry?

As you can see below, Farmer Bros had US$71.4m of debt at December 2019, down from US$130.0m a year prior. However, it also had US$9.13m in cash, and so its net debt is US$62.3m.

How Healthy Is Farmer Bros's Balance Sheet?

The latest balance sheet data shows that Farmer Bros had liabilities of US$89.8m due within a year, and liabilities of US$160.8m falling due after that. Offsetting this, it had US$9.13m in cash and US$62.0m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$179.4m.

This deficit casts a shadow over the US$117.0m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Farmer Bros would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Farmer Bros can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Farmer Bros had negative earnings before interest and tax, and actually shrunk its revenue by 5.7%, to US$580m. That's not what we would hope to see.

Caveat Emptor

Over the last twelve months Farmer Bros produced an earnings before interest and tax (EBIT) loss. Its EBIT loss was a whopping US$17m. When we look at that alongside the significant liabilities, we're not particularly confident about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. It's fair to say the loss of US$49m didn't encourage us either; we'd like to see a profit. In the meantime, we consider the stock to be risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Consider risks, for instance. Every company has them, and we've spotted 2 warning signs for Farmer Bros you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:FARM

Farmer Bros

Engages in the roasting, wholesale, equipment servicing, and distribution of coffee, tea, and other allied products in the United States.

Fair value with mediocre balance sheet.