- United States

- /

- Marine and Shipping

- /

- NYSE:GSL

Discover 3 Undiscovered Gems in the United States Market

Reviewed by Simply Wall St

Over the last 7 days, the United States market has experienced a slight decline of 1.6%, yet it remains up by an impressive 31% over the past year, with earnings projected to grow by 15% annually in the coming years. In this dynamic environment, identifying stocks that are undervalued or overlooked can offer unique opportunities for investors seeking to capitalize on potential growth and resilience.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Eagle Financial Services | 169.49% | 12.30% | 1.92% | ★★★★★★ |

| Morris State Bancshares | 17.84% | 4.83% | 6.58% | ★★★★★★ |

| Franklin Financial Services | 222.36% | 5.55% | -1.86% | ★★★★★★ |

| Omega Flex | NA | 0.39% | 2.57% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.65% | 11.17% | ★★★★★★ |

| Teekay | NA | -3.71% | 60.91% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 7.11% | -35.88% | ★★★★★☆ |

| Valhi | 38.71% | 2.57% | -19.76% | ★★★★★☆ |

| Nanophase Technologies | 40.87% | 24.19% | -9.71% | ★★★★★☆ |

| FRMO | 0.13% | 19.43% | 29.70% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

Northwest Pipe (NasdaqGS:NWPX)

Simply Wall St Value Rating: ★★★★★☆

Overview: Northwest Pipe Company, with a market cap of $478.28 million, manufactures and supplies water-related infrastructure products in North America.

Operations: Northwest Pipe generates revenue from two main segments: Engineered Steel Pressure Pipe, contributing $330.54 million, and Precast Infrastructure and Engineered Systems, adding $152.54 million.

Northwest Pipe, a small-cap player in the construction sector, is leveraging its strong position in the Steel Pressure Pipe market and expanding Precast segment to drive growth. Over the past five years, earnings have grown at 4% annually, with a current net debt to equity ratio of 18.2%, deemed satisfactory. The company reported Q3 2024 revenues of US$130.2 million and net income of US$10.25 million, up from US$118.72 million and US$5.82 million respectively last year, reflecting robust performance amidst challenges like fluctuating steel prices and competition. Trading slightly below fair value enhances its appeal for potential investors seeking growth opportunities in infrastructure projects.

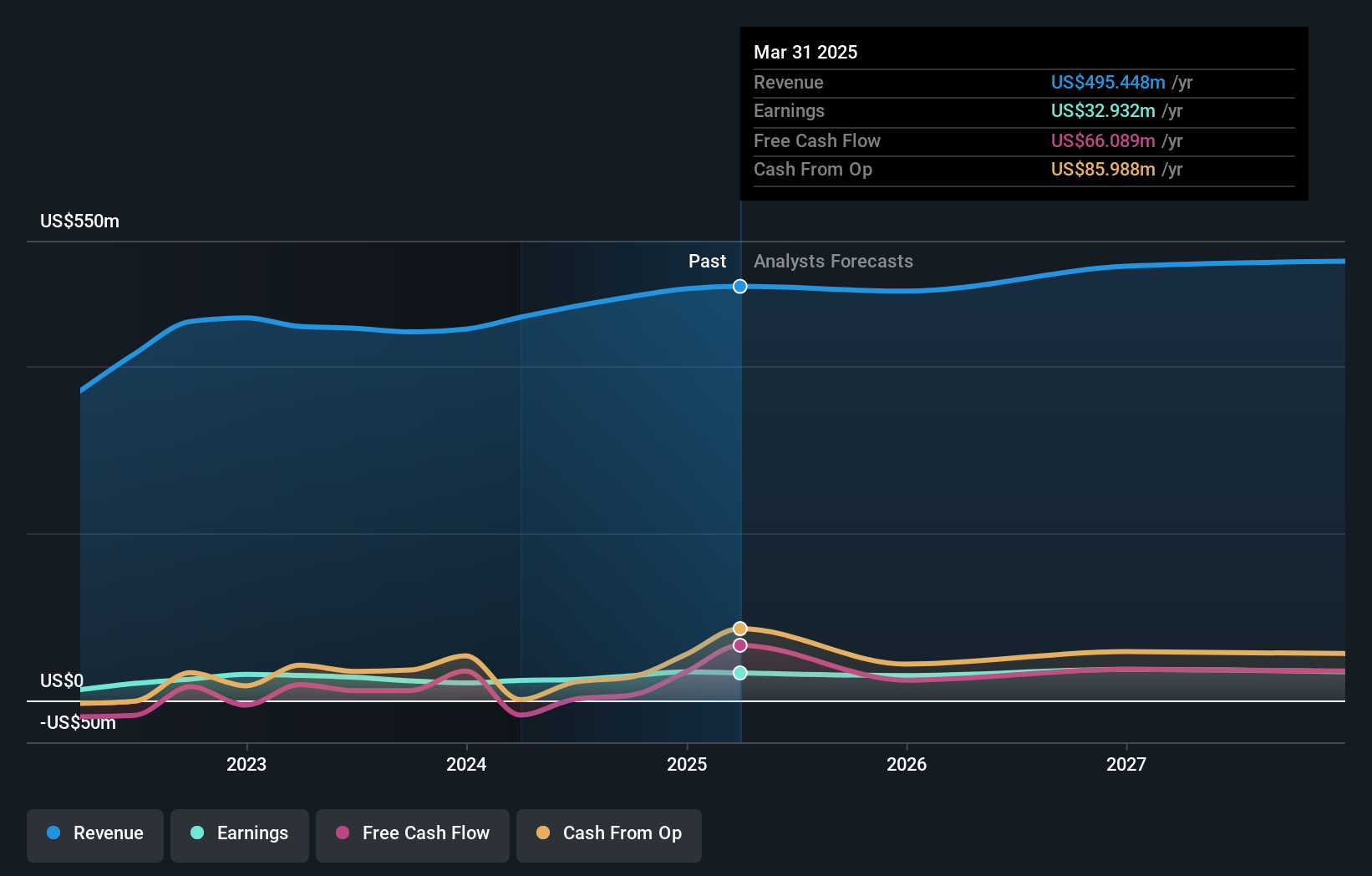

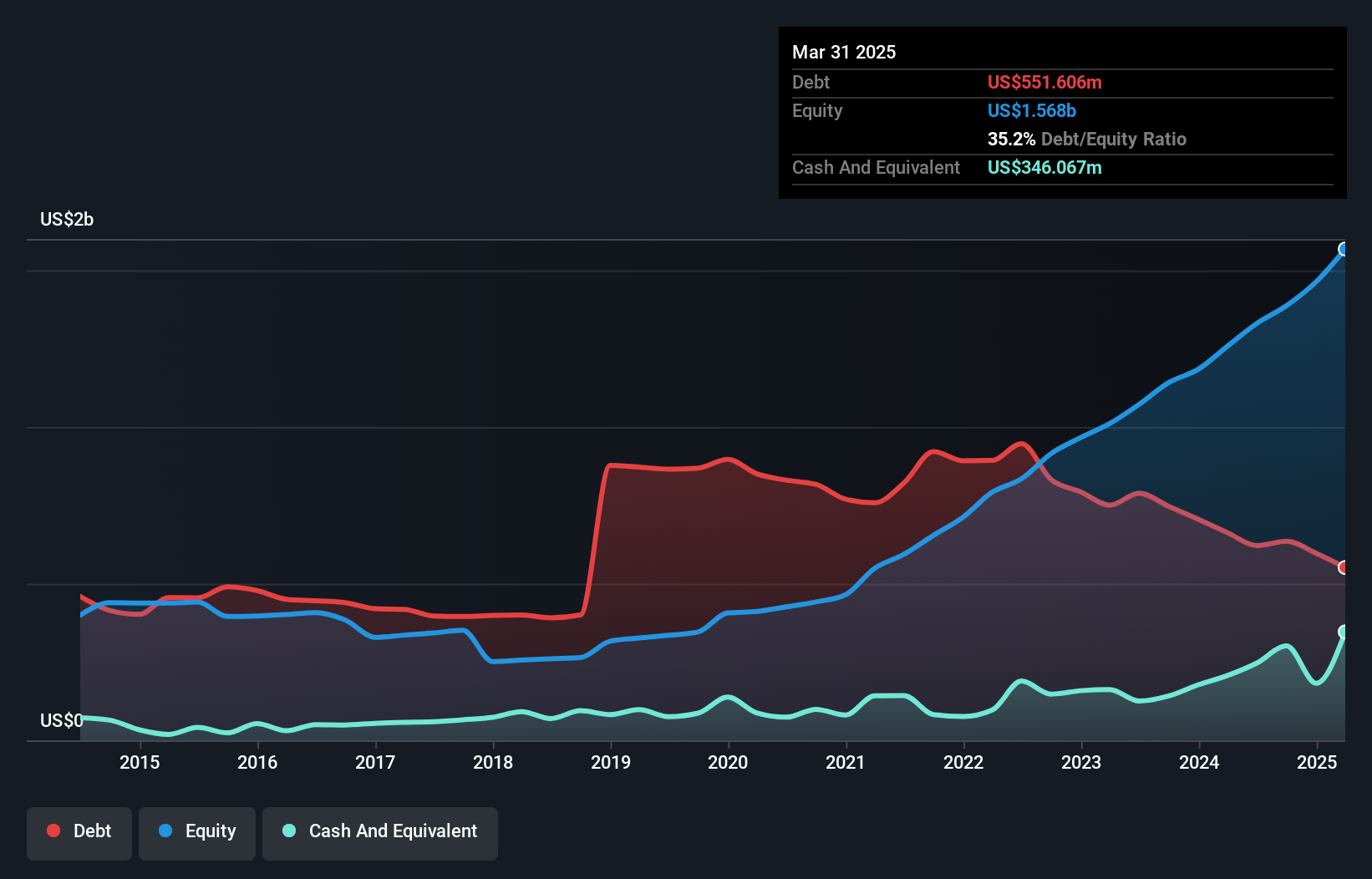

Global Ship Lease (NYSE:GSL)

Simply Wall St Value Rating: ★★★★★☆

Overview: Global Ship Lease, Inc. operates by owning and chartering containerships under fixed-rate charters to container shipping companies globally, with a market capitalization of approximately $848.36 million.

Operations: GSL generates revenue primarily through its transportation and shipping segment, amounting to $701.94 million. The company operates under fixed-rate charters, providing a stable revenue stream from its containerships.

Global Ship Lease, a player in the containership chartering sector, has seen its earnings grow by 4.1% over the past year, outpacing the shipping industry's 3.4%. Trading at a significant discount of 74.4% below its estimated fair value, it offers an attractive entry point for investors. The company's debt to equity ratio has impressively decreased from 258.1% to 46.7% over five years, highlighting effective debt management strategies. With interest payments well covered by EBIT at a remarkable 149x coverage and high-quality earnings reported, Global Ship Lease demonstrates financial stability despite potential market volatility risks ahead.

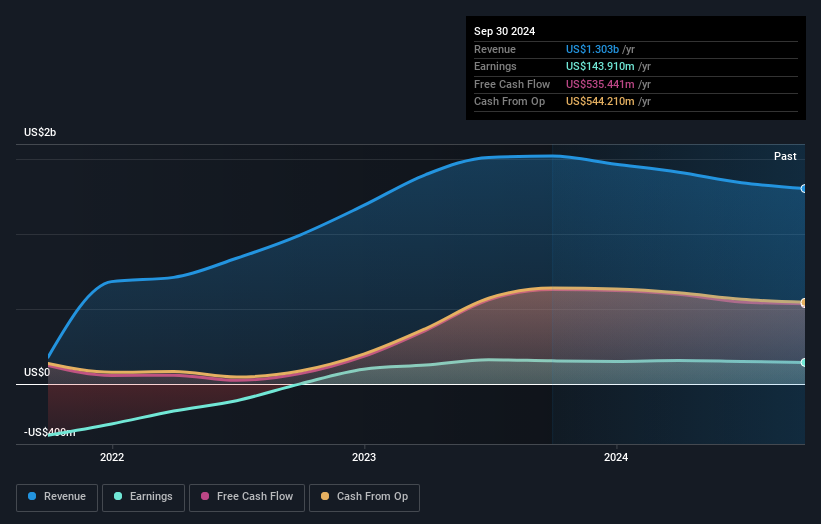

Teekay (NYSE:TK)

Simply Wall St Value Rating: ★★★★★★

Overview: Teekay Corporation Ltd. is a company that provides crude oil and other marine transportation services globally, with a market capitalization of approximately $715.57 million.

Operations: Teekay generates revenue primarily from its Teekay Tankers segment, which contributed $1.19 billion, while the Teekay Parent segment added $111.50 million.

Teekay Corporation, a notable player in the maritime industry, showcases financial resilience with its debt-free status and high-quality earnings. Despite a -6.8% earnings growth over the past year, which is better than the oil and gas sector's average of -30.2%, Teekay remains undervalued at 91.5% below its estimated fair value. The company reported Q3 sales of US$272 million and net income of US$20 million, reflecting a decrease from last year's figures but still maintaining profitability with free cash flow reaching US$629 million recently. A special dividend of US$1 per share highlights shareholder returns amidst these dynamics.

- Unlock comprehensive insights into our analysis of Teekay stock in this health report.

Explore historical data to track Teekay's performance over time in our Past section.

Make It Happen

- Delve into our full catalog of 223 US Undiscovered Gems With Strong Fundamentals here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GSL

Global Ship Lease

Engages in owning and chartering of containerships under fixed-rate charters to container shipping companies worldwide.

Very undervalued with excellent balance sheet and pays a dividend.