Natural Resource Partners (NRP) shares saw modest movement over the past week, with recent trading reflecting a wait-and-see sentiment from investors. The stock’s small gain comes as the market considers the partnership’s long-term value and recent performance.

While Natural Resource Partners’ share price drifted only slightly upward over the past week, the real story sits in its solid long-term run. The partnership has delivered a steady 1.85% total shareholder return over the past year, with momentum fueled by an impressive 186% total return across three years. This signals persistent interest despite recent swings.

The big question for investors now is whether Natural Resource Partners is trading below its true worth, or if the recent gains reflect a market that is already pricing in all of the partnership's future growth potential.

Advertisement

Price-to-Earnings of 9.5x: Is it justified?

Natural Resource Partners is currently trading at a price-to-earnings ratio of 9.5x, placing its market value well below the US Oil and Gas industry average of 13.5x. With a last close price of $105.5, this signals a notable discount compared to sector peers and may suggest the market is cautious about future growth or is underpricing profitability.

The price-to-earnings (PE) ratio is a widely used metric that compares a company’s current share price to its per-share earnings. For a resource partnership like NRP, this figure helps investors gauge how the market values current and anticipated profits, especially given the company’s strong profitability and robust profit margins.

Valued at a 9.5x multiple versus the industry’s 13.5x, NRP appears attractively valued on this measure. This suggests that, relative to the sector, investors are not paying a premium for NRP’s strong returns and high-quality earnings. If the market reassesses what it is willing to pay for these factors, there could be further upside ahead.

However, based on comparisons to the peer average, NRP is considered expensive, given the peer average is negative (-8.5x) due to sector-specific circumstances. The discount to the broader industry average remains a key point of focus for valuation observers.

However, challenging commodity prices or regulatory changes could dampen returns. It is crucial for investors to monitor industry developments closely.

Another View: Discounted Cash Flow Model Weighs In

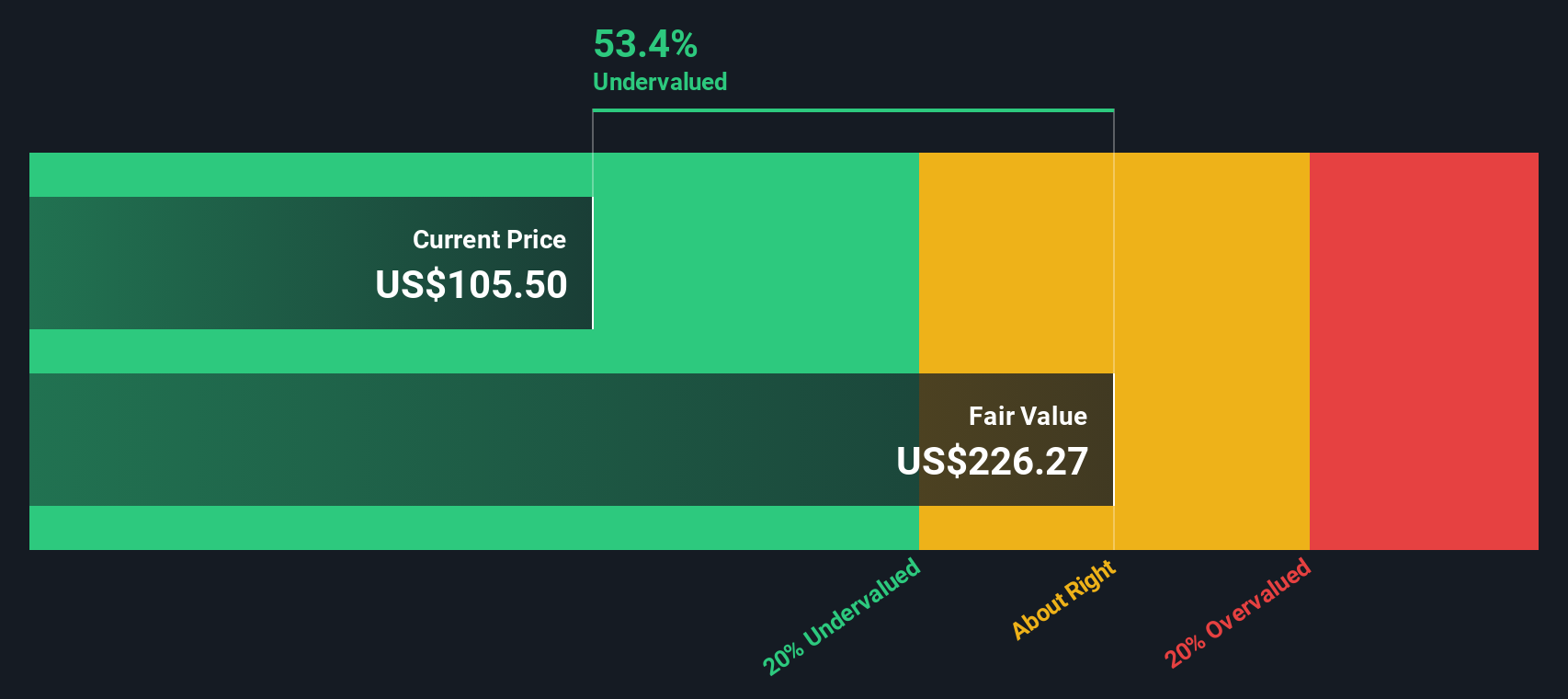

While the price-to-earnings ratio points to attractive value, our DCF model takes a more granular look at NRP’s future cash flows. It estimates the partnership’s fair value at $226.27. This suggests the current $105.5 share price is significantly undervalued. What could the market be missing?

Build Your Own Natural Resource Partners Narrative

If you’d rather dive into the numbers yourself or challenge the story we’ve outlined here, it takes just a few minutes to shape your own perspective. So why not Do it your way?

A great starting point for your Natural Resource Partners research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let opportunity pass you by. Take a proactive step toward smarter investing and uncover hidden gems, growth leaders, and steady performers that fit your goals.

Capitalize on technological breakthroughs in the medical field by spotting future innovators through these 32 healthcare AI stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Natural Resource Partners might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.