Advertisement

- United States

- /

- Energy Services

- /

- NYSE:KGS

Kodiak Gas Services (KGS) Completes Major Buyback Despite Wider Losses—What Does This Signal for Capital Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- Kodiak Gas Services reported its third quarter 2025 earnings, recording sales of US$296.97 million and a net loss of US$14.01 million, while also announcing the completion of a major share buyback program totaling over 2.49 million shares for US$84.96 million.

- Although year-over-year sales increased, both net loss and loss per share widened, highlighting cost pressures even as the company returned significant capital to shareholders through its repurchase activity.

- We'll assess how the widened quarterly net loss and substantial share buyback completion influence Kodiak Gas Services' current investment outlook.

This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

Kodiak Gas Services Investment Narrative Recap

Shareholders in Kodiak Gas Services need to believe in sustained growth for the Permian Basin and continued robust demand for large horsepower compression, as these are central to Kodiak's revenue outlook. The latest quarterly update, highlighting a widened net loss despite rising sales and a completed share buyback, does not materially shift the biggest short-term catalyst of increasing natural gas demand or the primary risk of margin pressure from elevated labor costs and operational expansion challenges in the Permian region.

Among recent announcements, the completion of a US$84.96 million share repurchase program stands out, reinforcing Kodiak's efforts to return capital to shareholders even in the face of profitability headwinds. This action sits alongside recent dividend increases and emphasizes ongoing shareholder returns, but does not directly address the underlying operational cost pressures described in the latest earnings results.

In contrast, investors should be aware that persistent labor tightness in Kodiak’s key operating region could...

Read the full narrative on Kodiak Gas Services (it's free!)

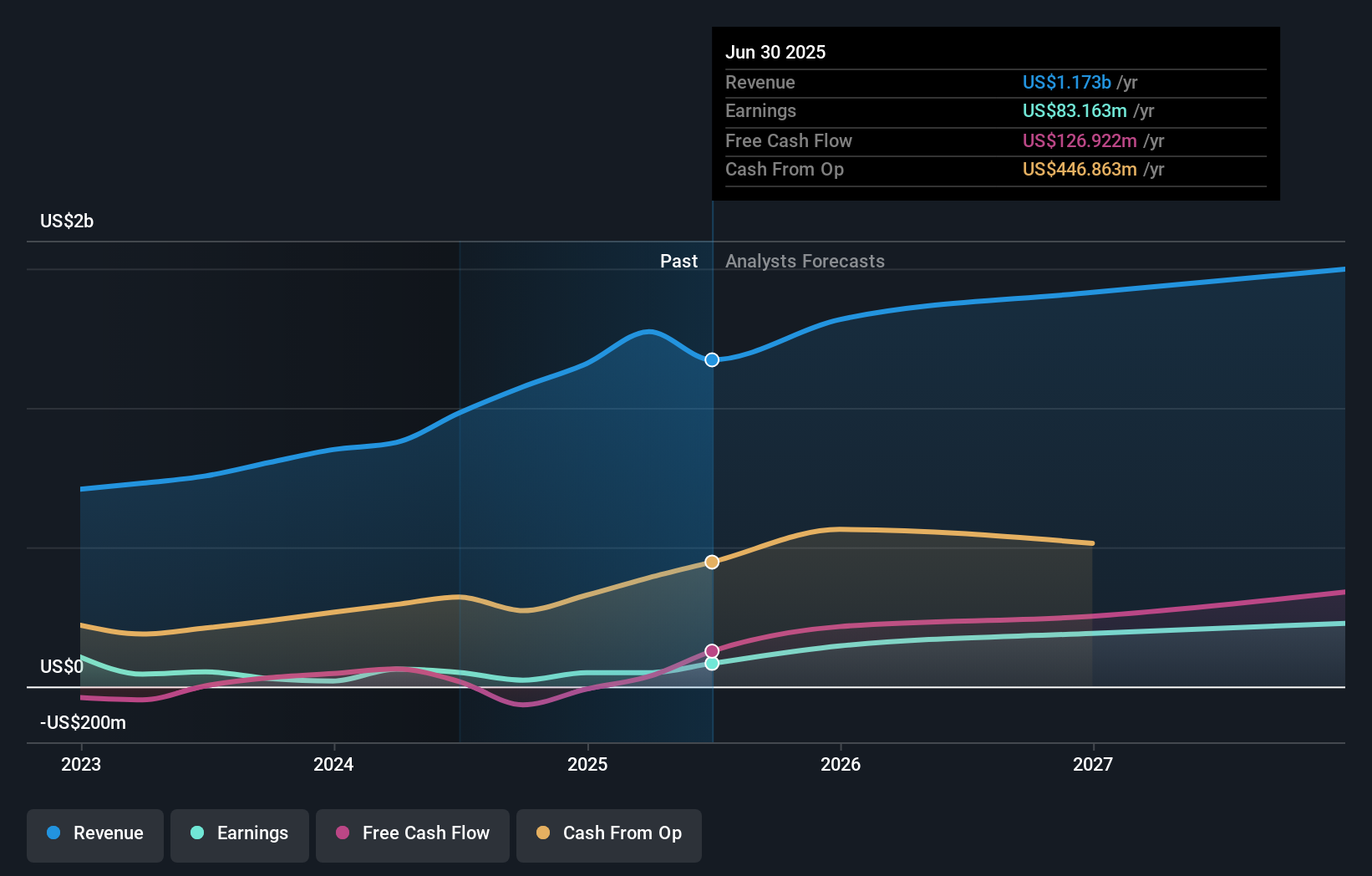

Kodiak Gas Services' outlook anticipates $1.5 billion in revenue and $293.4 million in earnings by 2028. This is based on a projected 5.8% annual revenue growth rate and an increase in earnings of about $210 million from current earnings of $83.2 million.

Uncover how Kodiak Gas Services' forecasts yield a $44.20 fair value, a 30% upside to its current price.

Exploring Other Perspectives

Three perspectives from the Simply Wall St Community place Kodiak’s fair value between US$44.20 and US$72.32 per share. However, with margin pressure highlighted in the latest results, you may want to compare these views for a fuller picture.

Explore 3 other fair value estimates on Kodiak Gas Services - why the stock might be worth over 2x more than the current price!

Build Your Own Kodiak Gas Services Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kodiak Gas Services research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Kodiak Gas Services research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kodiak Gas Services' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kodiak Gas Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KGS

Kodiak Gas Services

Operates contract compression infrastructure for customers in the oil and gas industry in the United States.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor