Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:INSW

Will International Seaways’ (INSW) Capital Returns and Fleet Renewal Reshape Its Long-Term Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 6, 2025, International Seaways reported its third quarter results, including revenue of US$196.39 million and net income of US$70.55 million, alongside the declaration of a regular US$0.12 and supplemental US$0.74 per share dividend to be paid in December.

- Despite year-over-year declines in revenue and earnings, the company extended its share repurchase program to 2026 and continued its fleet renewal strategy, reflecting management’s focus on shareholder returns and operational modernization.

- We'll explore how International Seaways' ongoing capital return program and fleet renewal effort impact its investment narrative and future prospects.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

International Seaways Investment Narrative Recap

To see International Seaways as an attractive investment, you’d need confidence in sustained demand for seaborne oil transport and the company’s ability to modernize its fleet within a volatile market. The latest results showed lower revenue and earnings but did not alter the most important short-term catalyst, longer trade routes from shifting refinery patterns, nor did they substantially reduce the biggest risk around regulatory costs for fleet upgrades. The impact of this quarter’s performance appears limited for now.

Among the recent announcements, the extension of the share repurchase program through 2026 stands out. This reflects management’s ongoing commitment to returning capital to shareholders, which complements the fleet renewal strategy and adds support to the potential for near-term shareholder value, even as operating performance fluctuates.

By contrast, investors should be aware that the tightening environmental regulations facing the tanker industry could mean that...

Read the full narrative on International Seaways (it's free!)

International Seaways' narrative projects $848.0 million revenue and $288.7 million earnings by 2028. This requires 2.0% yearly revenue growth and a $50.1 million earnings increase from $238.6 million currently.

Uncover how International Seaways' forecasts yield a $57.50 fair value, a 8% upside to its current price.

Exploring Other Perspectives

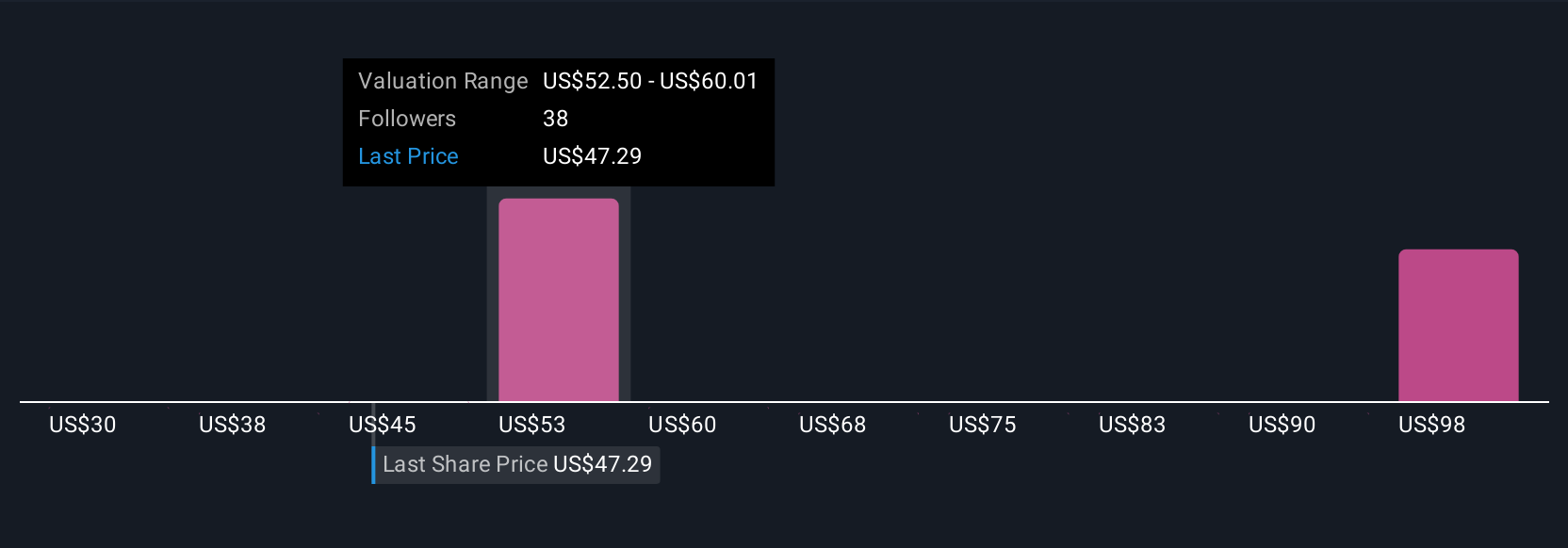

Six retail investors in the Simply Wall St Community pegged International Seaways’ fair value from as low as US$30 to as high as US$120. With regulations likely to increase costs industry-wide, it’s clear opinions on future performance and value can differ widely, consider reviewing several viewpoints before making a decision.

Explore 6 other fair value estimates on International Seaways - why the stock might be worth over 2x more than the current price!

Build Your Own International Seaways Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your International Seaways research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

- Our free International Seaways research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate International Seaways' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:INSW

International Seaways

Owns and operates a fleet of oceangoing vessels for the transportation of crude oil and petroleum products in the international flag trade.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor