Stock Analysis

- United States

- /

- Energy Services

- /

- NYSE:DRQ

Dril-Quip (NYSE:DRQ) Is In A Strong Position To Grow Its Business

We can readily understand why investors are attracted to unprofitable companies. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So, the natural question for Dril-Quip (NYSE:DRQ) shareholders is whether they should be concerned by its rate of cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for Dril-Quip

When Might Dril-Quip Run Out Of Money?

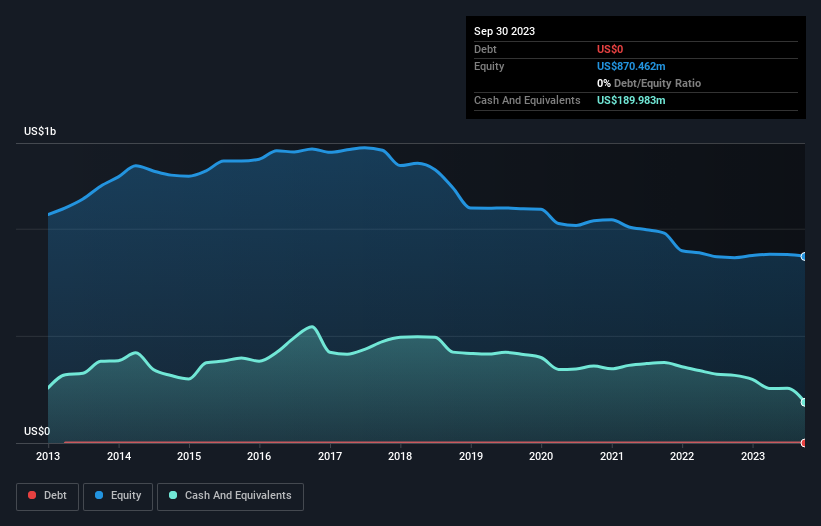

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. In September 2023, Dril-Quip had US$190m in cash, and was debt-free. In the last year, its cash burn was US$89m. That means it had a cash runway of about 2.1 years as of September 2023. Notably, however, analysts think that Dril-Quip will break even (at a free cash flow level) before then. If that happens, then the length of its cash runway, today, would become a moot point. You can see how its cash balance has changed over time in the image below.

How Well Is Dril-Quip Growing?

Notably, Dril-Quip actually ramped up its cash burn very hard and fast in the last year, by 195%, signifying heavy investment in the business. While operating revenue was up over the same period, the 15% gain gives us scant comfort. Taken together, we think these growth metrics are a little worrying. Clearly, however, the crucial factor is whether the company will grow its business going forward. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

Can Dril-Quip Raise More Cash Easily?

Even though it seems like Dril-Quip is developing its business nicely, we still like to consider how easily it could raise more money to accelerate growth. Companies can raise capital through either debt or equity. Many companies end up issuing new shares to fund future growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Since it has a market capitalisation of US$779m, Dril-Quip's US$89m in cash burn equates to about 11% of its market value. As a result, we'd venture that the company could raise more cash for growth without much trouble, albeit at the cost of some dilution.

Is Dril-Quip's Cash Burn A Worry?

It may already be apparent to you that we're relatively comfortable with the way Dril-Quip is burning through its cash. For example, we think its cash runway suggests that the company is on a good path. While we must concede that its increasing cash burn is a bit worrying, the other factors mentioned in this article provide great comfort when it comes to the cash burn. It's clearly very positive to see that analysts are forecasting the company will break even fairly soon. Looking at all the measures in this article, together, we're not worried about its rate of cash burn; the company seems well on top of its medium-term spending needs. When you don't have traditional metrics like earnings per share and free cash flow to value a company, many are extra motivated to consider qualitative factors such as whether insiders are buying or selling shares. Please Note: Dril-Quip insiders have been trading shares, according to our data. Click here to check whether insiders have been buying or selling.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

Valuation is complex, but we're helping make it simple.

Find out whether Dril-Quip is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:DRQ

Dril-Quip

Dril-Quip, Inc., together with its subsidiaries, designs, manufactures, sells, and services engineered drilling and production equipment for offshore and onshore applications worldwide.

Flawless balance sheet with reasonable growth potential.