Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:BTU

Are Acquisition Costs Reshaping Peabody Energy’s (BTU) Long-Term Value Proposition?

Simply Wall St

Reviewed by Sasha Jovanovic

- Peabody Energy Corporation reported a third-quarter 2025 net loss of US$70.1 million, with sales falling to US$1,012.1 million from US$1,088 million a year earlier, and declared a quarterly dividend of US$0.075 per share payable in December.

- The company attributed its operating loss mainly to costs from a terminated acquisition, while offering progress updates on its Centurion Mine project in Australia and improved labor relations at the Metropolitan Mine.

- We’ll examine how Peabody’s acquisition-related costs and operational developments could shift its previously positive long-term investment narrative.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Peabody Energy Investment Narrative Recap

To own Peabody Energy stock, investors must believe in the staying power of coal demand, especially as policy supports and operational efficiencies counter global energy transition risks. The recent operating loss tied to the terminated acquisition adds a temporary setback, but the most important short-term catalyst remains the Centurion Mine ramp-up and this update signals no material disruption; the key risk continues to be long-term coal demand erosion from net-zero ambitions and regulatory tightening.

The ongoing progress at the Centurion Mine in Australia stands out from recent announcements as particularly relevant. This project’s timeline to reach full-scale production by February 2026 is central to Peabody’s catalyst of shifting its portfolio more toward high-margin metallurgical coal, a move that could help offset declining thermal coal demand and support future earnings, assuming execution stays on track.

However, investors should be alert that, despite these operational updates, exposure to regulatory or policy changes remains a ...

Read the full narrative on Peabody Energy (it's free!)

Peabody Energy's outlook projects $4.9 billion in revenue and $468.2 million in earnings by 2028. This scenario assumes a 6.4% annual revenue growth and a $327.3 million increase in earnings from the current $140.9 million.

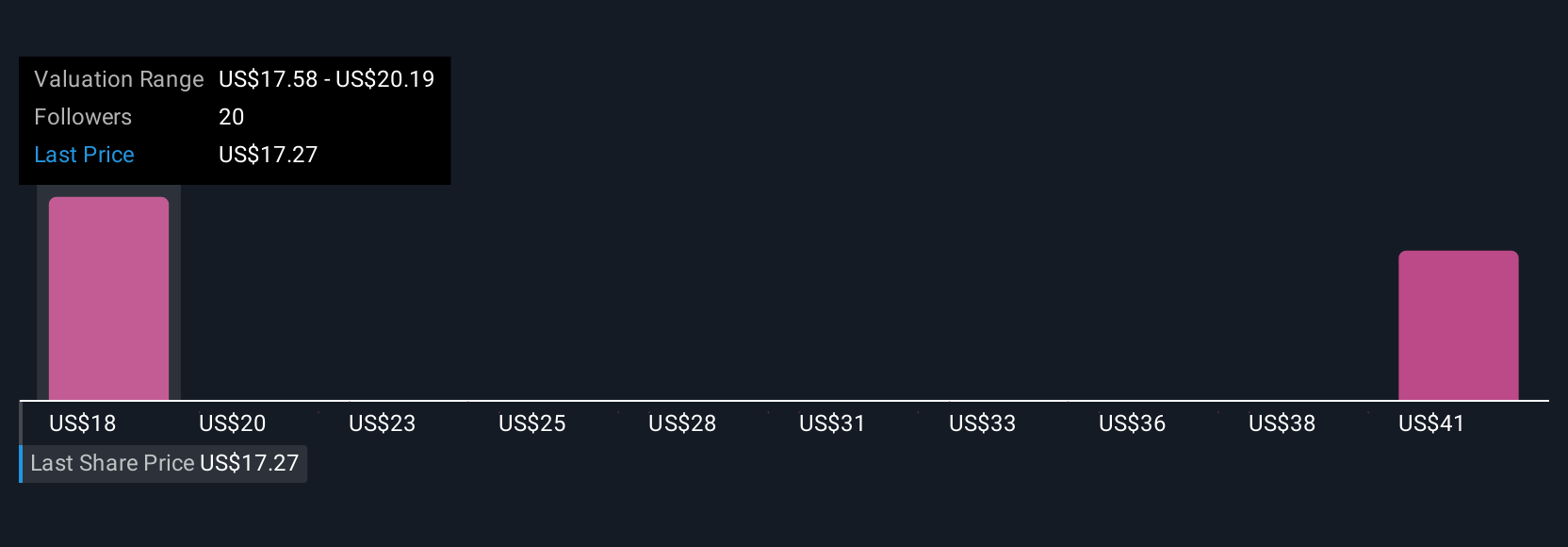

Uncover how Peabody Energy's forecasts yield a $33.95 fair value, a 12% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community’s fair value estimates for Peabody Energy span from US$24 to US$86.10, across five analyses. In contrast, ongoing global policy shifts toward renewables could significantly impact the company’s addressable market, so it is essential to consider these diverse views before making decisions.

Explore 5 other fair value estimates on Peabody Energy - why the stock might be worth over 2x more than the current price!

Build Your Own Peabody Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Peabody Energy research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Peabody Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Peabody Energy's overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Rare earth metals are the new gold rush. Find out which 35 stocks are leading the charge.

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BTU

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor