Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:BKV

A Fresh Look at BKV (BKV) Valuation After 20% Share Price Surge

Simply Wall St

Reviewed by Simply Wall St

BKV (BKV) shares have returned over 20% in the past month, standing out in a volatile energy market. Investors appear to be responding to the company's consistent growth and expansion across natural gas operations in Texas and Pennsylvania.

See our latest analysis for BKV.

Momentum has clearly been building for BKV, with a 30-day share price return of nearly 20% and a total shareholder return over the past year just above 30%. That rally reflects renewed optimism as the company benefits from favorable energy market trends and a string of operational milestones.

If recent energy gains have you thinking bigger, now is a perfect opportunity to discover fast growing stocks with high insider ownership.

But after such a strong rally, is BKV still overlooked by the market? Alternatively, are investors already factoring in all of its future growth potential? The key question is whether there is real value left for buyers to capture.

Price-to-Earnings of 56.9x: Is it justified?

At a last close price of $28.22, BKV trades at a price-to-earnings (PE) ratio of 56.9x, which is well above both its peer group and sector averages. This signals investor optimism or possibly high expectations for future profitability that the current earnings may not fully support.

The PE ratio measures how much investors are willing to pay per dollar of company earnings. For oil and gas companies, this multiple typically reflects anticipated future earnings growth, operational risk, and sector volatility. BKV’s elevated PE suggests the market sees either continuing earnings acceleration or a unique growth story that justifies the premium.

Looking closer, BKV's PE of 56.9x is notably higher than the US Oil and Gas industry average of 13.4x and also exceeds the peer group average of 33.7x. In comparison to an estimated fair price-to-earnings ratio of 27.5x, the market might be significantly overpricing the company based on near-term financials alone. This raises questions about whether such a steep multiple is sustainable or if future earnings and growth must deliver well beyond industry norms to be justified.

Explore the SWS fair ratio for BKV

Result: Price-to-Earnings of 56.9x (OVERVALUED)

However, a shift in energy prices or regulatory setbacks could quickly challenge expectations for continued outperformance.

Find out about the key risks to this BKV narrative.

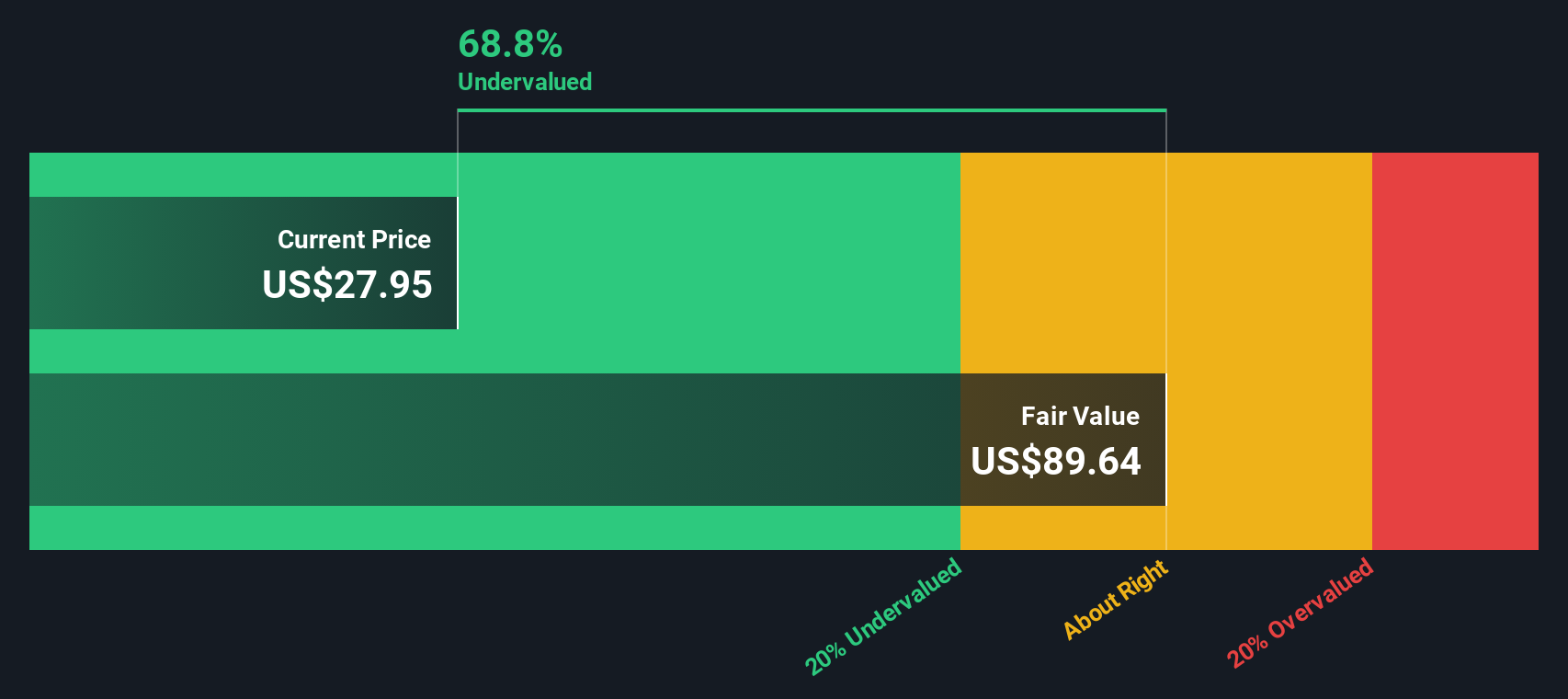

Another View: What Does Our DCF Model Say?

While the market’s price-to-earnings ratio places BKV in clearly overvalued territory, our SWS DCF model offers a different perspective. According to this method, BKV’s current share price is actually trading far below what the company’s long-term cash flows could justify. This suggests a potential undervaluation.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out BKV for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 927 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own BKV Narrative

If you’d rather chart your own course or come to different conclusions, it’s simple to analyze the figures and shape your own perspective in minutes, so why not Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding BKV.

Looking for more investment ideas?

Take control of your financial future by acting now. Do not watch the best opportunities pass by while others get ahead using smart tools.

- Capture the potential of fast-growing sectors by evaluating these 25 AI penny stocks for emerging leaders in artificial intelligence.

- Boost your income prospects by targeting these 14 dividend stocks with yields > 3% offering above-average yields backed by solid fundamentals.

- Seize opportunities at a discount by screening these 927 undervalued stocks based on cash flows and uncovering stocks trading well below their intrinsic value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BKV might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BKV

BKV

Produces and sells natural gas in the Barnett Shale in the Fort Worth Basin of Texas and in the Marcellus Shale in the Appalachian Basin of Northeast Pennsylvania.

High growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.5% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

28 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on NVIDIA ·

Not a Bubble, But the "Industrial Revolution 4.0" Engine

Fair Value:US$294.9239.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$416.4647.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

111 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

945 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

146 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative