Advertisement

- United States

- /

- Oil and Gas

- /

- NasdaqCM:USEG

Need To Know: Analysts Just Made A Substantial Cut To Their U.S. Energy Corp. (NASDAQ:USEG) Estimates

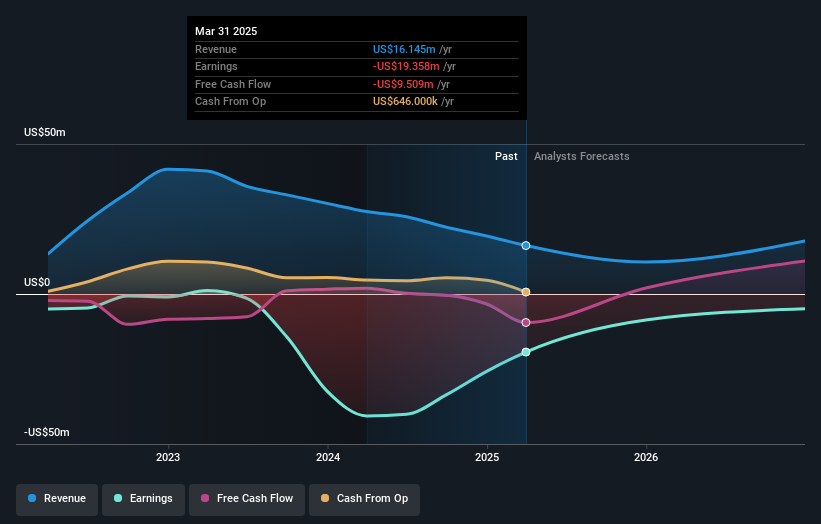

The latest analyst coverage could presage a bad day for U.S. Energy Corp. (NASDAQ:USEG), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon. Bidders are definitely seeing a different story, with the stock price of US$1.22 reflecting a 11% rise in the past week. With such a sharp increase, it seems brokers may have seen something that is not yet being priced in by the wider market.

After the downgrade, the consensus from U.S. Energy's dual analysts is for revenues of US$11m in 2025, which would reflect a concerning 34% decline in sales compared to the last year of performance. Losses are predicted to fall substantially, shrinking 55% to US$0.26 per share. Yet before this consensus update, the analysts had been forecasting revenues of US$14m and losses of US$0.23 per share in 2025. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a serious cut to their revenue forecasts while also expecting losses per share to increase.

Check out our latest analysis for U.S. Energy

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 43% by the end of 2025. This indicates a significant reduction from annual growth of 31% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 3.6% per year. It's pretty clear that U.S. Energy's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to note from this downgrade is that the consensus increased its forecast losses this year, suggesting all may not be well at U.S. Energy. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that U.S. Energy's revenues are expected to grow slower than the wider market. Given the serious cut to this year's outlook, it's clear that analysts have turned more bearish on U.S. Energy, and we wouldn't blame shareholders for feeling a little more cautious themselves.

After a downgrade like this, it's pretty clear that previous forecasts were too optimistic. What's more, we've spotted several possible issues with U.S. Energy's business, like major dilution from new stock issuance in the past year. Learn more, and discover the 2 other warning signs we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies backed by insiders.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:USEG

U.S. Energy

An independent energy company, focuses on the acquisition, exploration, and development of industrial gas, and oil and natural gas properties in the continental United States.

Slight risk and fair value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor