Advertisement

- United States

- /

- Energy Services

- /

- NasdaqGS:BKR

Baker Hughes (BKR): A Closer Look at Its Current Valuation After Recent Share Price Momentum

Simply Wall St

Reviewed by Simply Wall St

Baker Hughes (BKR) shares have been steadily climbing, closing recently at $48.95 after gaining over 8% for the month. Investors are taking note of its consistent performance and are prompting a closer look at what is driving the momentum.

See our latest analysis for Baker Hughes.

Zooming out, Baker Hughes has been steadily building momentum, with its 30-day share price return of almost 9% and a strong total shareholder return of nearly 15% over the past year. The recent climb reflects growing optimism around the company’s outlook and reinforces its longer-term track record of delivering for shareholders.

If the energy sector’s upswing has you looking for the next opportunity, consider broadening your search and discover fast growing stocks with high insider ownership

But with shares up nearly 15% over the past year and trading just below analyst price targets, the question now is whether Baker Hughes remains undervalued or if the market has already factored in all future growth potential.

Most Popular Narrative: 6.6% Undervalued

With Baker Hughes closing at $48.95, the narrative-backed fair value estimate sits higher at $52.43. This gap hints at more upside if key assumptions play out as projected. Now let's see what supports this view.

The company's strong momentum in securing large-scale service contracts, framework agreements, and technology-driven orders (such as for data centers, LNG, CCS, and recurring gas tech services) is driving an all-time high IET backlog. This builds strong visibility into future revenue and supports sustained earnings durability.

Want to know which unstoppable business trends and bold numbers are baked into this fair value? The analysts behind this narrative are counting on a powerful mix of high-margin growth, recurring revenue, and ambitious financial targets, all underpinned by a valuation multiple rarely seen in the sector. Uncover the full strategy that could keep Baker Hughes ahead of the curve.

Result: Fair Value of $52.43 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent cost pressures or a sharper than expected drop in oil demand could quickly challenge Baker Hughes’s upbeat outlook and valuation momentum.

Find out about the key risks to this Baker Hughes narrative.

Another View: Comparing to Peers and Industry

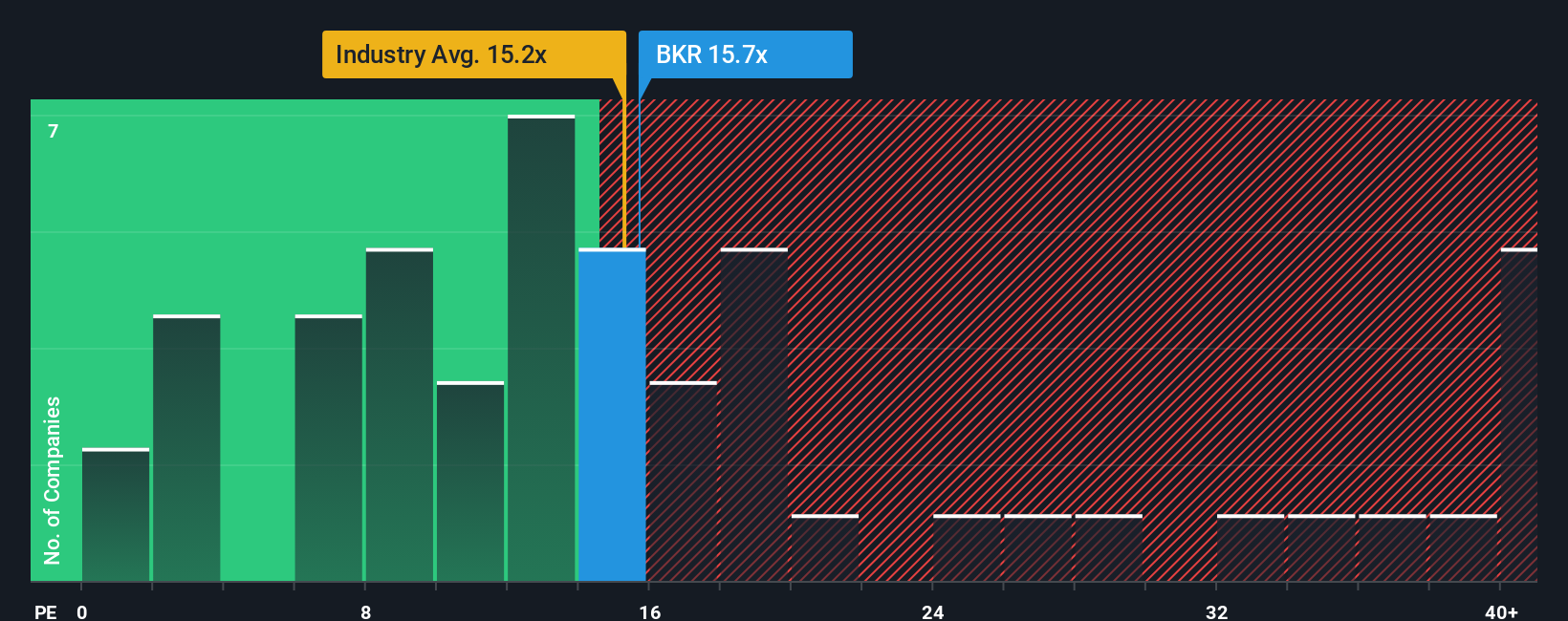

While narrative-driven fair value suggests Baker Hughes is undervalued, the company’s current price-to-earnings ratio of 16.7x nearly matches the US Energy Services industry average of 16.7x and is slightly above the peer average of 16.6x. At the same time, it sits just below the estimated fair ratio of 17.6x, indicating only a narrow margin between opportunity and risk. Could a small change in market sentiment tip the balance?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Baker Hughes Narrative

Your perspective might differ or you may want to run your own analysis. You can easily craft a personalized Baker Hughes narrative in just minutes Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Baker Hughes.

Looking for More Smart Investment Moves?

Don’t let opportunity pass you by. Today’s winners often start as early ideas, so take charge and uncover tomorrow’s top stocks using Simply Wall St tools.

- Target high income potential and start building a stream of passive returns with these 15 dividend stocks with yields > 3% offering yields greater than 3%.

- Spot tomorrow’s tech leaders before the crowd by reviewing these 25 AI penny stocks shaping the future of artificial intelligence.

- Position yourself for outsized gains by checking out these 855 undervalued stocks based on cash flows, which could be trading below their real worth right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Baker Hughes might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:BKR

Baker Hughes

Provides a portfolio of technologies and services to energy and industrial value chain worldwide.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor