P10 (PX) shares have been on a slow slide over the past month, dipping about 5%. While there is no single event driving recent price action, investors are watching to see if value emerges at current levels.

Even with the recent 5% slip, P10’s share price has been trending lower for most of 2024, and the 19.7% year-to-date decline reflects fading momentum. Over the past year, the total shareholder return was a milder -6.3%. This hints that long-term holders have fared better than recent entrants as sentiment continues to shift.

With shares well below analyst price targets and a 20% year-to-date loss, P10 trades at a steep discount by some metrics. However, does this represent a genuine bargain, or is the market simply factoring in modest growth ahead?

Advertisement

Price-to-Earnings of 77.6x: Is it justified?

P10 shares currently trade at a price-to-earnings ratio of 77.6x, while the stock last closed at $10.31. This places the company at a significant premium compared to comparable firms.

The price-to-earnings ratio (P/E) is a simple but telling yardstick. It shows how much investors are willing to pay today for a dollar of earnings. In the capital markets space, it can reflect confidence in future growth or suggest the market is betting on an earnings rebound.

With P10’s P/E at 77.6x, the premium stands well above the US Capital Markets industry average of 24.3x and the peer average of just 7.6x. Such a wide gap signals the stock is currently judged expensive based on trailing earnings, despite big profit growth recently. This could be factoring in expectations for a strong turnaround, or possibly overstating future growth given the company’s recent earnings swing and forecasts for moderate revenue expansion. No fair ratio estimate is available to help frame how much this multiple might revert, but the existing premium is hard to dismiss.

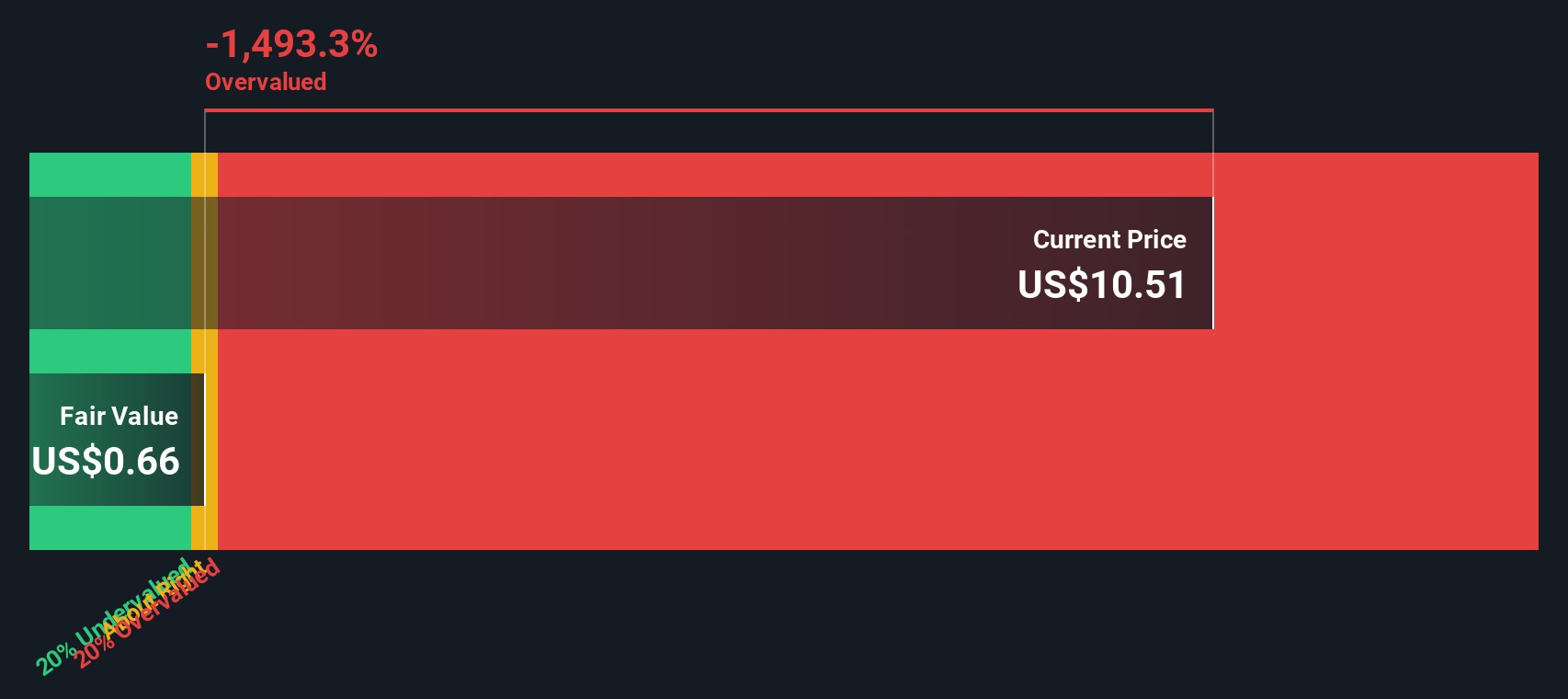

Looking from a different angle, our DCF model delivers a starkly different signal. It estimates P10's fair value at just $0.66, which suggests the stock is trading well above what the company’s future cash flows might justify. This raises the question of whether the risk of overpaying is too high, or if there are hidden strengths the market observes.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out P10 for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 840 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own P10 Narrative

If you’re looking for your own perspective or enjoy doing your own homework, you can build a narrative using the same data in just minutes, Do it your way.

Smart investors stay ahead by seeking fresh opportunities. Don’t limit yourself when the market rewards those who act. Expand your search and level up your strategy today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks