Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:HASI

Assessing Hannon Armstrong (HASI) Valuation After Recent Share Price Gains

Simply Wall St

Reviewed by Simply Wall St

HA Sustainable Infrastructure Capital (HASI) has seen its share price deliver some interesting moves recently, with a 15% climb over the past month and a nearly 20% gain year-to-date. Curious investors may be taking notice of these shifts, especially given the company’s strong annual revenue growth.

See our latest analysis for HA Sustainable Infrastructure Capital.

Momentum appears to be building for HA Sustainable Infrastructure Capital, with a 15% share price return over the past month reflecting renewed market interest in its growth story. While the short-term move has turned heads, its 1-year total shareholder return of nearly 19% and a strong three-year total return suggest those gains are rooted in something more sustainable than just a fleeting rally.

If you’re watching stocks that have started to pick up steam, now is an ideal time to broaden your search and discover fast growing stocks with high insider ownership

But with such strong recent performance and analysts targeting even higher prices, investors are left to wonder whether this sustainable growth story is still trading at a discount or if the market has already priced in all the future upside.

Price-to-Earnings of 13.4x: Is it justified?

HA Sustainable Infrastructure Capital is trading at a price-to-earnings (P/E) ratio of 13.4x, just above the US Diversified Financial industry average of 13x. This reflects a slightly richer valuation in the context of its last close at $32.48.

The price-to-earnings ratio compares the company’s current share price to its per-share earnings, providing a snapshot of how much investors are willing to pay for each dollar of profit. For diversified financials, P/E can signal how the market views a company’s future earnings growth or stability relative to its peers.

While the market is paying a premium over the broader industry, this premium is quite narrow. Notably, the company trades well below its peer group average of 27.4x, which indicates that HASI could still offer relative value. When compared to the estimated “fair” P/E of 13.5x, determined by considering business fundamentals and sector trends, HASI’s current multiple suggests there is little room for mispricing. It is trading almost exactly where analysts’ models say it should be.

Explore the SWS fair ratio for HA Sustainable Infrastructure Capital

Result: Price-to-Earnings of 13.4x (ABOUT RIGHT)

However, unexpected shifts in industry trends or changes in growth rates could challenge the company’s current valuation and its potential for future gains.

Find out about the key risks to this HA Sustainable Infrastructure Capital narrative.

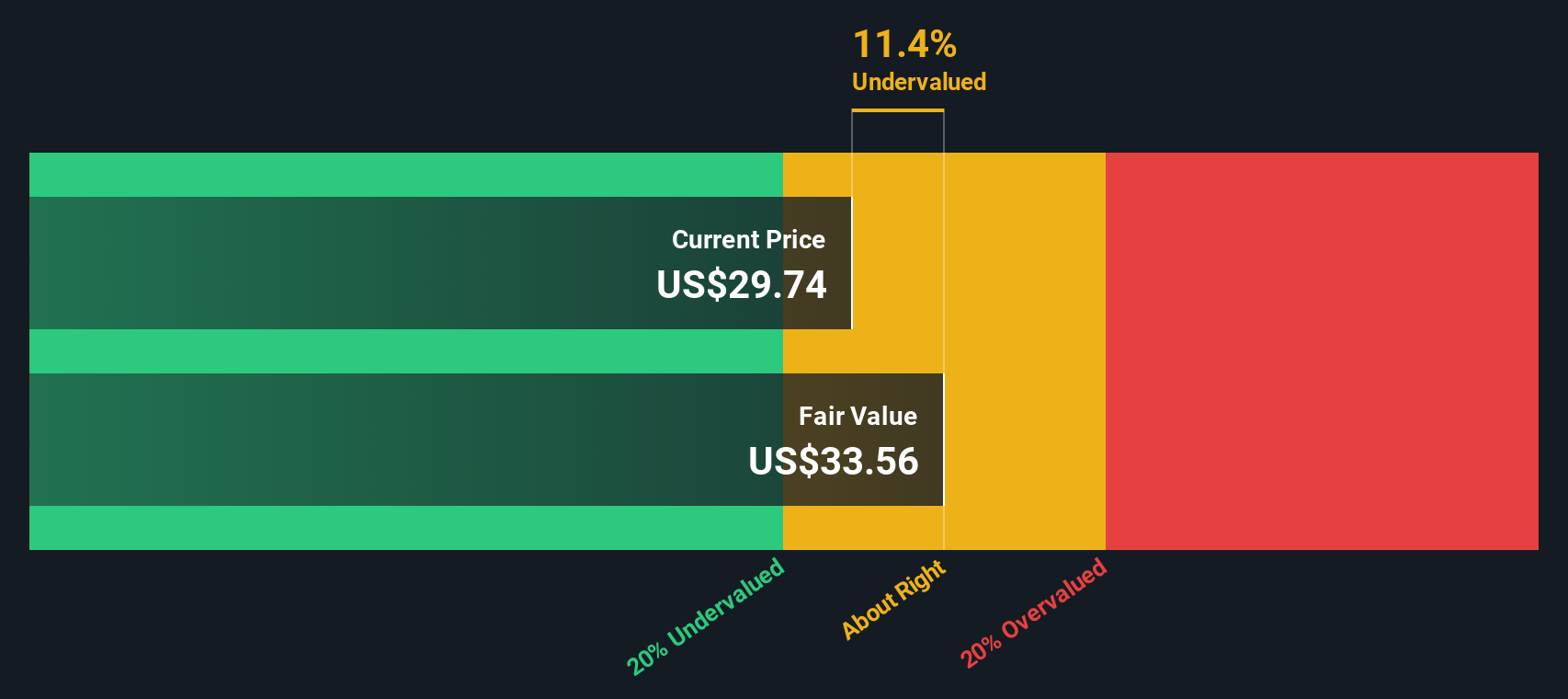

Another View: The SWS DCF Model

While the company's price-to-earnings ratio places it in line with fair value, our DCF model takes a different approach. It estimates that HA Sustainable Infrastructure Capital is undervalued by about 12% compared to its $36.99 fair value. Does this indicate hidden upside, or is the market seeing something the model isn't?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out HA Sustainable Infrastructure Capital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 918 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own HA Sustainable Infrastructure Capital Narrative

If you see things differently or want to analyze the numbers your own way, you can build and share your perspective in just a few minutes. Do it your way

A great starting point for your HA Sustainable Infrastructure Capital research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t settle for just one strong pick when you can open the door to a whole range of compelling stocks with big upside potential. Turn curiosity into action by checking out these powerful opportunities:

- Capture income with stable returns when you review these 17 dividend stocks with yields > 3%, offering yields above 3% and strong fundamentals behind every payout.

- Gain early access to industry breakthroughs as you survey these 26 quantum computing stocks, featuring companies making bold advances in quantum computing.

- Tap into tomorrow’s leaders by seeking out these 25 AI penny stocks, riding the cutting edge of artificial intelligence innovation and growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HA Sustainable Infrastructure Capital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HASI

HA Sustainable Infrastructure Capital

Through its subsidiaries, engages in the investment in energy efficiency, renewable energy, and sustainable infrastructure markets in the United States.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor