Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:BRK.A

Berkshire Hathaway (BRK.A): Assessing Valuation After Buffett Retirement News and Strong Q3 Results

Simply Wall St

Reviewed by Simply Wall St

Berkshire Hathaway’s (BRK.A) recent stock action comes after two major developments: CEO Warren Buffett’s retirement announcement and the release of strong third-quarter results, featuring higher operating profits and a record cash pile.

See our latest analysis for Berkshire Hathaway.

Berkshire Hathaway’s share price is showing renewed strength, up over 7% in the past three months as investors digest Warren Buffett’s pending retirement and the company’s robust third-quarter results. While market momentum has picked up lately, the one-year total shareholder return of 7.5% reflects a steadier, long-term pace rather than a sharp rally or retreat.

If Berkshire’s staying power has you considering what else is worth a look, now is a smart time to broaden your scope and discover fast growing stocks with high insider ownership

With the stock sitting near all-time highs and a historic cash position, investors must ask if Berkshire Hathaway remains undervalued after its latest results or if the market is already factoring in all foreseeable growth.

Price-to-Earnings of 16x: Is it justified?

Berkshire Hathaway’s stock is trading at a price-to-earnings (P/E) ratio of 16x, signaling a value that sits well below the peer average of 27x and the estimated fair P/E ratio of 16.9x. With a recent closing price of $748,320, the market appears to reflect cautious optimism about future earnings.

The price-to-earnings ratio measures how much investors are willing to pay for a dollar of the company's earnings. For a diversified financial giant like Berkshire Hathaway, the P/E is a crucial indicator because it encapsulates both the company’s steady performance and investor sentiment on its long-term profitability. A moderate ratio like 16x usually signals reasonable expectations rather than exuberance or pessimism.

Despite reporting negative earnings growth over the past year, Berkshire’s current P/E stands out as good value compared not only to direct peers in the diversified financial sector but also relative to what regression analysis suggests the fair value should be. This means the market could still move closer to the 16.9x level if there is positive momentum or improved earnings.

Explore the SWS fair ratio for Berkshire Hathaway

Result: Price-to-Earnings of 16x (UNDERVALUED)

However, slower annual revenue growth and declining net income signal potential challenges ahead. These factors could temper Berkshire Hathaway’s current valuation optimism.

Find out about the key risks to this Berkshire Hathaway narrative.

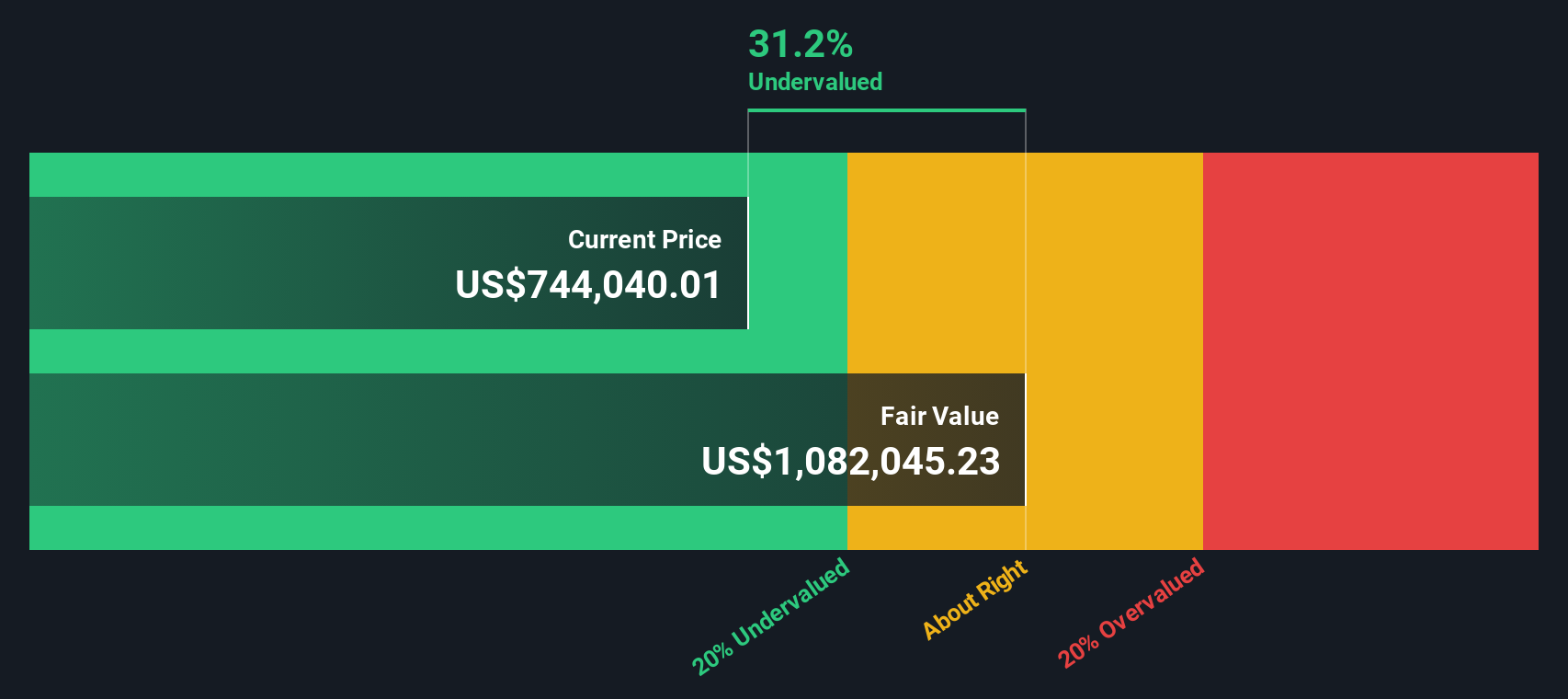

Another View: Discounted Cash Flow Suggests Deeper Discount

While the current valuation appears reasonable using the price-to-earnings metric, our DCF model paints a different picture. Berkshire Hathaway is trading roughly 34.5% below its estimated fair value by this method. Could the market be underestimating future cash generation potential, or is there a risk the forecast is too optimistic?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Berkshire Hathaway for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 870 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Berkshire Hathaway Narrative

If you see the numbers differently or want to dive into your own analysis, you can quickly craft a personal take on Berkshire Hathaway in just a few minutes, and Do it your way

A great starting point for your Berkshire Hathaway research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let fresh opportunities pass you by. Get ahead of the market with the Simply Wall Street Screener and uncover smart stock picks tailored to your strategy.

- Unlock the growth potential of emerging tech disruptors by taking a closer look at these 24 AI penny stocks that are driving innovation across multiple industries.

- Boost your portfolio’s income stream when you tap into these 16 dividend stocks with yields > 3% providing solid yields above 3% year after year.

- Catch the next big trend in digital assets and see how these 82 cryptocurrency and blockchain stocks are transforming finance and technology on a global scale.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Berkshire Hathaway might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BRK.A

Berkshire Hathaway

Through its subsidiaries, engages in the insurance, freight rail transportation, and utility businesses.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor