Ares Management (ARES) has captured investor attention as its shares recently moved lower, slipping about 1% at the last close. Given the stock's longer-term growth and recent results, it is worth exploring what might be driving the current action.

This latest dip in Ares Management’s share price comes after a volatile stretch, with the stock down over 19% in the last three months. The company still boasts an impressive 94% total shareholder return over three years. Momentum has faded lately, but long-term performance remains strong and continues to signal the company’s enduring growth story.

If you’re curious where else rapid growth and insider conviction are shaping markets, now’s a great time to broaden your perspective and discover fast growing stocks with high insider ownership

With shares now trading below both recent highs and some analyst targets, investors are left to weigh whether Ares Management is undervalued at these levels or if the market has already accounted for future growth.

Advertisement

Most Popular Narrative: 16% Undervalued

Ares Management's widely followed narrative presents a fair value of $180 per share, notably above its last close of $151.26. This suggests that the narrative sees significant upside potential and sets the stage for ambitious performance expectations.

Expansion into multiple asset classes (infrastructure, real estate, sports/media, secondaries), with recent successes such as the GCP acquisition and the scaling of data center asset management, is expected to deliver higher management and development fees. This supports long-term revenue and FRE growth. Robust international fundraising, particularly in Europe and Asia-Pacific, along with ongoing success in deepening distribution partnerships, is broadening Ares' addressable markets, increasing global deal flow, and positioning the company for sustained earnings growth.

Curious which ambitious growth numbers are fueling this valuation? The narrative points to management’s bold expansion bets and high-multiple expectations. But the specific assumptions behind this upside — would you have guessed them? Tap in to see what really drives this fair value.

However, mounting competition and potential fee pressure could unsettle Ares Management's outlook, especially if rivals cut fees aggressively to gain market share.

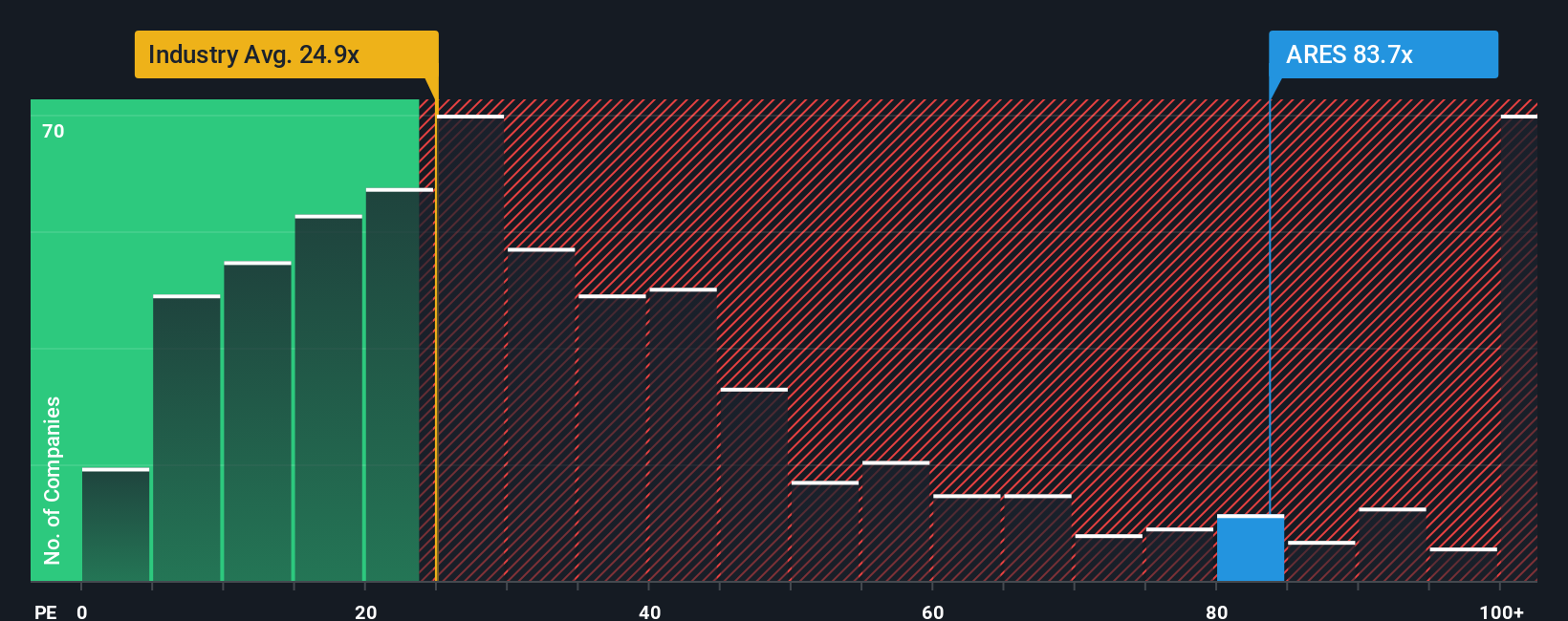

Looking through the lens of price-to-earnings, Ares Management appears expensive. Its 63.7x ratio is far above the US Capital Markets average of 23.8x, its peer average of 13.3x, and even the market's fair ratio of 26.1x. That kind of premium suggests higher valuation risk if growth stumbles or expectations shift. Could the story be too optimistic?

Not seeing your story reflected here, or want to dig into the numbers personally? Take a hands-on approach by creating your own take in just minutes. Do it your way

A great starting point for your Ares Management research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t stop at Ares Management. Seize the next big opportunity by reviewing high-potential companies handpicked with proven metrics on Simply Wall Street’s powerful Screener.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks