Advertisement

- United States

- /

- Hospitality

- /

- NYSE:GBTG

Need To Know: Analysts Are Much More Bullish On Global Business Travel Group, Inc. (NYSE:GBTG) Revenues

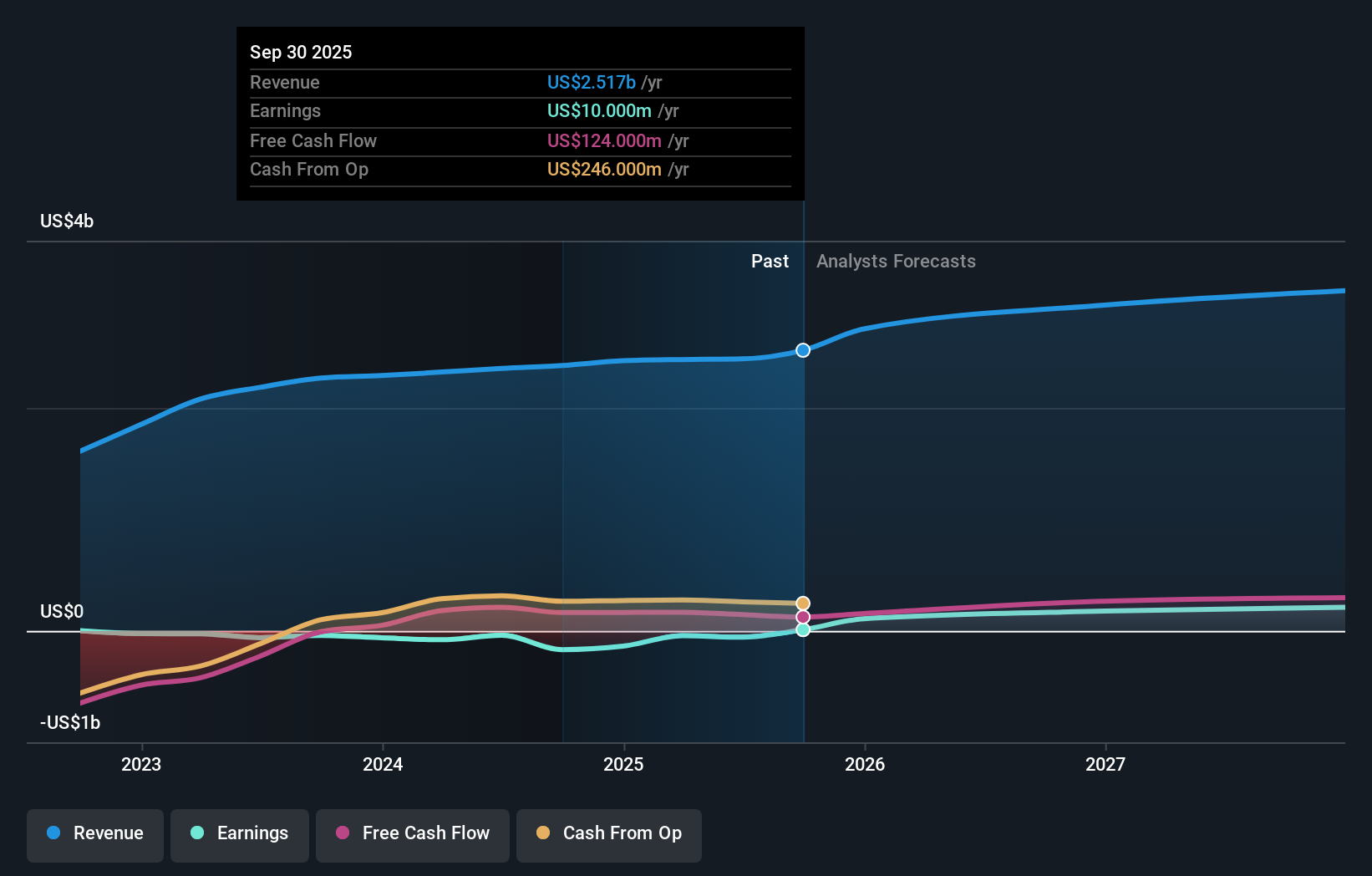

Celebrations may be in order for Global Business Travel Group, Inc. (NYSE:GBTG) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

Following the upgrade, the current consensus from Global Business Travel Group's six analysts is for revenues of US$3.0b in 2026 which - if met - would reflect a meaningful 19% increase on its sales over the past 12 months. Per-share earnings are expected to shoot up 1,685% to US$0.34. Before this latest update, the analysts had been forecasting revenues of US$2.6b and earnings per share (EPS) of US$0.34 in 2026. It seems analyst sentiment has certainly become more bullish on revenues, even though they haven't changed their view on earnings per share.

Check out our latest analysis for Global Business Travel Group

It may not be a surprise to see that the analysts have reconfirmed their price target of US$10.06, implying that the uplift in sales is not expected to greatly contribute to Global Business Travel Group's valuation in the near term.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that Global Business Travel Group's revenue growth is expected to slow, with the forecast 15% annualised growth rate until the end of 2026 being well below the historical 24% p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 10% annually. So it's pretty clear that, while Global Business Travel Group's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with analysts reconfirming that earnings per share are expected to continue performing in line with their prior expectations. They also upgraded their revenue estimates for next year, and sales are expected to grow faster than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Global Business Travel Group.

Using these estimates as a starting point, we've run a discounted cash flow calculation (DCF) on Global Business Travel Group that suggests the company could be somewhat undervalued. For more information, you can click through to our platform to learn more about our valuation approach.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:GBTG

Global Business Travel Group

Provides business-to-business (B2B) travel platform in the United States, the United Kingdom, and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor