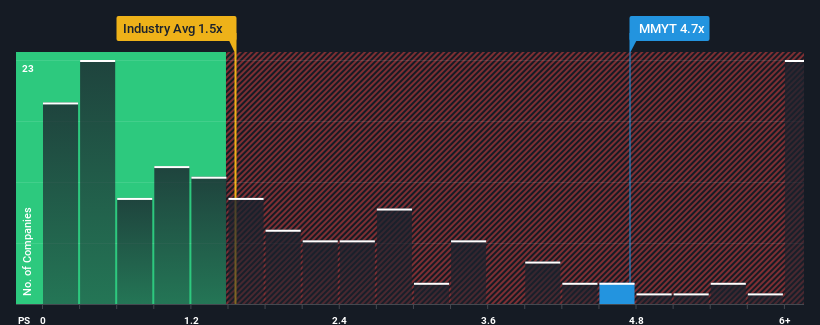

MakeMyTrip Limited's (NASDAQ:MMYT) price-to-sales (or "P/S") ratio of 4.7x may look like a poor investment opportunity when you consider close to half the companies in the Hospitality industry in the United States have P/S ratios below 1.5x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for MakeMyTrip

How MakeMyTrip Has Been Performing

With revenue growth that's superior to most other companies of late, MakeMyTrip has been doing relatively well. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on analyst estimates for the company? Then our free report on MakeMyTrip will help you uncover what's on the horizon.How Is MakeMyTrip's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as steep as MakeMyTrip's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an exceptional 95% gain to the company's top line. Revenue has also lifted 16% in aggregate from three years ago, mostly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Shifting to the future, estimates from the eight analysts covering the company suggest revenue should grow by 24% per annum over the next three years. That's shaping up to be materially higher than the 17% per annum growth forecast for the broader industry.

With this in mind, it's not hard to understand why MakeMyTrip's P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From MakeMyTrip's P/S?

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of MakeMyTrip's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for MakeMyTrip with six simple checks will allow you to discover any risks that could be an issue.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:MMYT

MakeMyTrip

MakeMyTrip (India) Private Limited , an online travel company, sells travel products and services.

Outstanding track record with excellent balance sheet.