Stock Analysis

- United States

- /

- Hospitality

- /

- NasdaqGS:CHDN

Is Now The Time To Put Churchill Downs (NASDAQ:CHDN) On Your Watchlist?

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

In contrast to all that, many investors prefer to focus on companies like Churchill Downs (NASDAQ:CHDN), which has not only revenues, but also profits. While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

Check out our latest analysis for Churchill Downs

Churchill Downs' Earnings Per Share Are Growing

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. Impressively, Churchill Downs has grown EPS by 29% per year, compound, in the last three years. As a general rule, we'd say that if a company can keep up that sort of growth, shareholders will be beaming.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. The music to the ears of Churchill Downs shareholders is that EBIT margins have grown from 23% to 26% in the last 12 months and revenues are on an upwards trend as well. Both of which are great metrics to check off for potential growth.

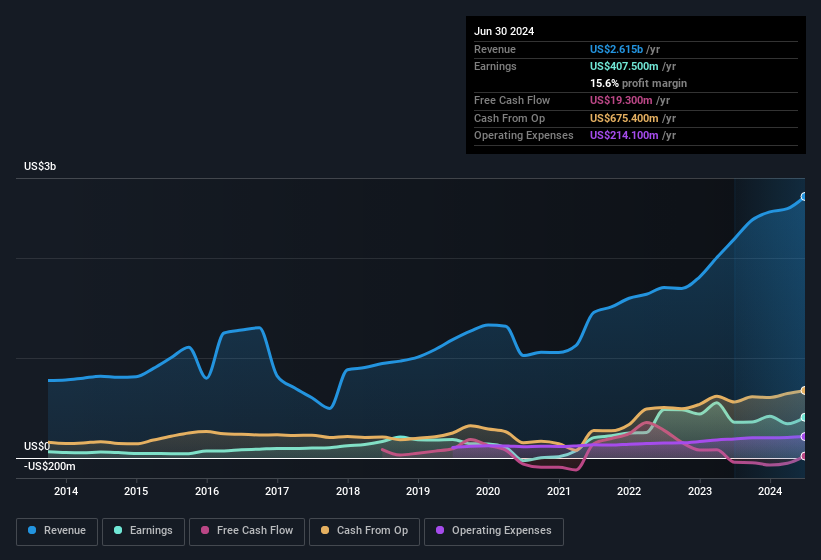

In the chart below, you can see how the company has grown earnings and revenue, over time. For finer detail, click on the image.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Churchill Downs' forecast profits?

Are Churchill Downs Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

First and foremost; there we saw no insiders sell Churchill Downs shares in the last year. But the really good news is that Independent Director Paul Varga spent US$495k buying stock, at an average price of around US$130. Big buys like that may signal an opportunity; actions speak louder than words.

On top of the insider buying, it's good to see that Churchill Downs insiders have a valuable investment in the business. Indeed, they have a considerable amount of wealth invested in it, currently valued at US$347m. This suggests that leadership will be very mindful of shareholders' interests when making decisions!

Does Churchill Downs Deserve A Spot On Your Watchlist?

If you believe that share price follows earnings per share you should definitely be delving further into Churchill Downs' strong EPS growth. On top of that, insiders own a significant piece of the pie when it comes to the company's stock, and one has been buying more. Astute investors will want to keep this stock on watch. Still, you should learn about the 1 warning sign we've spotted with Churchill Downs.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Churchill Downs, you'll probably love this curated collection of companies in the US that have an attractive valuation alongside insider buying in the last three months.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:CHDN

Churchill Downs

Operates as a racing, online wagering, and gaming entertainment company in the United States.